June 01, 2022

There is no one-size-fits-all when it comes to saving and investment strategies. However, there are best practices that can help you achieve your financial goals while minimizing risk. Here’s some tips on how to make the best financial decisions for your retirement nest egg.

Saving for retirement is one of the best financial strategies you can take part in. Everyone will hopefully retire at some point in their lifetime. Saving early on in life for your golden years will help prevent you from running out of money. Whether you’re on track for retirement or need to catch up, a Fiduciary financial advisor can help prepare you for your later years.

Here’s a look at 5 saving and investing tips that will help you maximize your savings for retirement.

What is a Retirement Savings Plan?

Having a retirement savings plan is essential to securing your financial security later in life. By utilizing various retirement savings accounts, you can maximize your tax savings, invest in the index funds, and take advantage of compound interest — leaving you with more money when the time comes to retire.

Take Advantage of Your 401(k) or 403(b) Company Match

401(k) and 403(b) plans are qualified tax-advantaged retirement plans offered by employers to their employees. If your workplace offers a retirement plan and a company match, it’s always best practice to contribute up to the maximum your company offers. It is financially beneficial to take advantage of your 401(k) or 403(b) early on in your career.

401(k) plans are offered by for-profit companies to eligible employees who contribute pre or post-tax money through payroll deduction. 403(b) plans are offered to employees of non-profit organizations and the government. You should always see what kind of retirement packages are offered with the company you work for to see where you can better invest and save your money.

Apply for Retirement Savings Credits

If you are a lower- or middle-income taxpayer, you may claim a saver’s tax credit for up to 50% of your retirement plan contribution. If you are married and filing jointly with an adjusted gross income (AGI) of below $68,000 for 2022 ($66,000 for 2021), and you contribute to a qualified retirement plan, you may be eligible for a tax credit.

The income limit for heads of household is $51,000 for 2022 and for single filers and married persons filing separately is $34,000.The maximum credit for 2021 and 2022 is $2,000 for married couples filing jointly and $1,000 for single filers (applied against the maximum contribution amounts: $4,000 for married couples filing jointly and $2,000 for single filers.

Contribute to a Health Savings Account

Healthcare costs are one of the highest growing expenses in the country. High-deductible health plans and health savings accounts are a golden retirement planning opportunity. This tool can not only be used to pay for healthcare expenses but can also be used to squirrel away additional funds for retirement.

Contributions are 100% tax-deductible, and funds unused for medical expenses may continue to be invested and grow over time. One of the best things about an HSA plan is that the distributions made on qualified medical expenses are tax-exempt. People over the age of 55 can keep and save an additional $1,000 per year. It’s important to remember that a traditional IRA is funded with pre-tax dollars whereas a Roth IRA is funded with after-tax dollars. Choose the one that works best for your tax situation.

Use the Backdoor Roth IRA to Increase Savings

For 2022, the AGI phase-out contribution range for Roth IRAs for married couples filing jointly is $204,000 to $214,000 and for single taxpayers and heads of households is $129,000 to $144,000. If your current income is too high and makes you ineligible to contribute to a Roth IRA, there’s another way in. First, contribute to a traditional IRA. There is no income ceiling for contributions to a non-deductible traditional IRA, although there is a limit to what can be contributed.

The IRS caps the contribution limit to $6,000 or $7,000 if you are 50 or over.After the funds clear, convert the traditional IRA to a Roth IRA. That way the funds can compound for the future and be withdrawn tax-free, as long as you meet the withdrawal guidelines.

Retire in the Right State

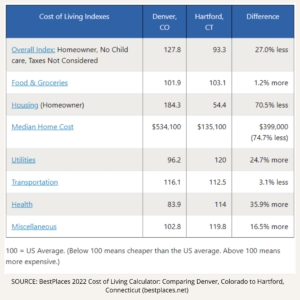

When it comes time to retire, you should look and see what states don’t have state income taxes. Alaska, Florida, South Dakota, New Hampshire, Tennessee, Wyoming, Texas, and Nevada are just some of the states that don’t have state income taxes. Colorado routinely ranks among the top tax-friendly states for retirees. The state income tax range is a low, flat rate of 4.63%, and you get a fair deduction on retirement income.

A good thing to note is that a majority of states don’t tax social security. Before packing up and moving, evaluate all of the taxes in your proposed new home state.

Fund Your Retirement Accounts with Side Hustles

Side jobs can be an excellent way to make money. Instead of using this cash to purchase a new car or upgrade your appliances, consider using it to fund your retirement accounts. If you haven’t maxed out your IRA contribution, this would be a great option.

Whether you are flipping furniture, tutoring students, or completing freelance work, using side hustles to save money for retirement can be a great way to save money and jump start your retirement investments.

Last Thoughts

It’s important to look at your retirement plan and see if any of our tips could maximize your savings. If you’re like most people, qualified-retirement plans, Social Security, personal savings and investments are expected to play a role. Once you have estimated the amount of money you may need for relocating in retirement, a sound approach involves taking a close look at your potential retirement-income sources.

At Agemy Financial Strategies, we want you to know we’re here to help you navigate retirement and any questions that come up during your retirement process. As Fiduciary advisors, it’s our duty to act on your behalf in finding the right solutions for your individual wants and needs.

For more information on our retirement and financial planning services, contact us here today.