Gold looks attractive in 2026 as a long‑term diversifier and potential inflation hedge, but it is volatile, richly priced, and should be used as a supporting asset, not a core growth engine.

For Agemy Financial Strategies clients, many of whom are pre‑retirees or retirees, the key question is not “Is gold good?” but “How much, in what form, and for what purpose?” within an overall financial plan.

Where Gold Stands in Early 2026

Gold has just come through one of its strongest multi‑year runs on record, dramatically outpacing many traditional assets. Gold has surged past $5,000 — and forecasts from major banks are calling for $6,000 or more by year’s end.

A few big forces are behind this surge:

- Strong central bank buying, especially from emerging markets that are diversifying away from the U.S. dollar.

- Rising allocations by retail investors and ETFs seeking a safe haven amid market volatility and policy uncertainty.

- Expectations of lower real interest rates as central banks, including the Federal Reserve, continue or contemplate rate cuts.

At the same time, analysts stress two important realities: gold rallies can be sharp and emotional, and the same is true of corrections. That means investors considering gold in 2026 need a clear, plan‑driven rationale, not fear or greed.

Why Many Experts Still Like Gold

Professionals often describe gold as “portfolio insurance” rather than a speculative trade. Here are the main reasons 2026 still looks constructive for gold.

1. Hedge against inflation and currency risk: Gold has historically tended to hold its purchasing power over long periods, even as paper currencies lose value. With years of aggressive monetary policy behind us and ongoing concern about fiscal deficits, many investors see a continued role for hard assets like gold.

2. Diversification and crisis protection: Gold often behaves differently than stocks and, to a lesser degree, bonds, especially during periods of stress. When equities experience sharp drawdowns, gold has frequently held value or risen, which can help cushion portfolio losses for retirees drawing income.

- Supportive macro backdrop

-

- Central banks are expected to continue buying hundreds of tonnes of gold annually, representing a meaningful share of yearly mine output.

- Retail and ETF demand jumped in 2025 and is projected to remain robust as investors seek safe‑haven exposure.

- Forecasts from major banks cluster around the idea that gold can remain elevated, with many calling for prices at or above $5,000 per ounce by late 2026 if current trends persist.

3. Favorable real‑rate and dollar dynamics: Gold often has a negative relationship with real interest rates and the U.S. dollar. Analysts expect further rate cuts and a softer real‑rate environment, which historically has supported gold prices, especially if the dollar weakens.

For long‑term, risk‑aware investors, these factors make gold a reasonable candidate for a modest allocation in 2026.

The Major Risks and Drawbacks in 2026

Our advisors would emphasize what gold is not: it is not a guaranteed winner, a substitute for income‑producing assets, or a one‑way bet.

- Elevated prices and the risk of buying “after the run”: Gold’s huge gains in 2025 and early 2026 mean new buyers are entering at historically high levels. Some analysts warn that if sentiment shifts, a sharp pullback is possible, especially for investors focused on short‑term gains.

- High volatility: Recent years have shown that gold can swing sharply in both directions within short periods. Those fluctuations can be unsettling for retirees who need stability around withdrawals, particularly if gold is over‑weighted.

- No income, no dividends: Unlike bonds or dividend‑paying stocks, gold does not produce interest or cash flow. For income‑oriented investors, this means gold must be funded by other assets that do produce income, or it risks undermining a retirement paycheck strategy.

- Opportunity cost if rates rise again: If inflation cools or central banks turn more hawkish, real yields could rise, making cash and bonds relatively more attractive than gold. In that scenario, gold prices could stagnate or decline while interest‑bearing assets provide positive income.

- Behavioral risk: Because headlines about “record highs” are so attention‑grabbing, investors may be tempted to chase gold late in the cycle, then panic‑sell at the first pullback. That pattern, buying high, selling low, is generally the opposite of what our planning‑driven approach aims to achieve.

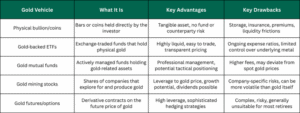

Ways to Invest in Gold in 2026

If gold fits into your plan, the next decision is how to gain exposure. Different vehicles carry different risks, costs, and logistical considerations.

For many retirement‑focused investors, a simple combination of a low‑cost, gold‑backed ETF or fund and possibly a modest amount of physical bullion is often the most practical approach. More speculative vehicles, such as futures or highly leveraged mining stocks, are usually better left to experienced, risk‑tolerant traders, not those relying on their nest egg.

How Agemy Might Position Gold in a 2026 Plan

From the perspective of a holistic retirement planning firm like Agemy Financial Strategies, the decision is less about timing the perfect entry point and more about integrating gold thoughtfully into an overall strategy.

- Clarify your purpose for owning gold

-

- Hedge against inflation and currency risk.

- Diversify equity and bond exposure.

- Provide psychological comfort (“sleep‑at‑night” insurance).

Each goal may justify a different target allocation and vehicle.

- Right‑size your allocation: Many experts view gold as a “satellite” holding rather than a core position, with allocations often in the mid‑single‑digit to low‑double‑digit percentage range depending on risk tolerance and objectives. Too little may not move the needle; too much can crowd out productive assets and add volatility.

- Integrate with income and withdrawal planning: For retirees, a key question is how gold interacts with income‑producing holdings. One approach is to let gold sit as a long‑term store of value while using dividends, interest, and systematic withdrawals from other assets to fund lifestyle needs.

- Set expectations and time horizon: Experts frequently stress that gold works best as a long‑term holding, not a short‑term trade. That means being prepared for periods when gold underperforms stocks or even declines in price, while keeping the focus on its role as insurance rather than as a primary growth engine.

- Stay diversified and disciplined: Even with bullish forecasts pointing toward the possibility of gold moving higher into and beyond 2026, concentration in any single asset is dangerous. A disciplined rebalancing plan, trimming gold after large run‑ups and adding modestly after pullbacks, can help manage risk and keep the allocation aligned with your plan.

So, Is Gold a Good Investment in 2026?

For many, the answer is: gold can be a good investment in 2026 as part of a diversified, plan‑driven portfolio, not as a stand‑alone bet. The macro backdrop of strong central bank demand, elevated geopolitical and economic uncertainty, and a potentially favorable interest‑rate environment all support a constructive long‑term outlook for gold.

At the same time, today’s high prices and the possibility of sharp corrections mean investors should approach gold thoughtfully, with realistic expectations and a long‑term mindset. The most appropriate allocation, vehicle, and timing will depend on your age, risk tolerance, income needs, and broader retirement goal, factors that a personalized plan can help you balance.

If you’re wondering whether gold belongs in your 2026 portfolio, the next step is to review your current holdings, risk profile, and retirement timeline with an advisor who understands how to use tools like gold as part of a comprehensive income and wealth‑protection strategy.

Contact us at agemy.com.