Retirement is no longer a distant dream—it’s a financial milestone that requires careful planning, especially in a changing economic climate like 2025.

One of the most common questions we hear at Agemy Financial Strategies is: “How much do I really need to retire comfortably?”

The answer? It depends on your lifestyle, health, location, tax exposure, and goals. In this guide, we’ll help you explore what “comfortable” really means and how much it might take to get there in today’s economic environment.

Defining “Comfortable” Retirement for the Wealthy

Only 27% of Americans feel very confident in their ability to maintain a comfortable retirement lifestyle, according to this EBRI Study.

So why are so few assured they’re on the right track?

The average American might target $1 million to $1.5 million for retirement. But for high-net-worth individuals, the equation is far more nuanced.

Comfort, in your case, often includes:

-

Multiple properties or vacation homes

-

Extended travel (domestic and international)

-

Financial support for adult children or grandchildren

-

Gifting and philanthropic goals

-

Concierge healthcare or long-term care services

-

Ongoing investment and business interests

-

Legacy planning and wealth transfer strategies

These ambitions require far more than average savings. They demand proactive planning, liquidity, and insulation from market, tax, and longevity risks.

What the Numbers Say in 2025

In 2025, the retirement landscape for HNWIs is more complex than ever. Here’s what you’re up against:

-

Inflation: Core inflation remains elevated, eroding purchasing power over time. A luxury lifestyle that costs $300,000 annually today may exceed $500,000 in two decades.

-

Longevity: High-net-worth retirees tend to live longer, with many planning for a 30-year retirement or more.

-

Healthcare Costs: According to a recent report, a 65-year-old couple can expect to spend over $330,000 on healthcare in retirement—and that doesn’t include long-term care or private medical services.

-

Tax Law Sunset: The 2026 tax law sunset could dramatically alter planning needs for HNWIs. Provisions of the 2017 Tax Cuts and Jobs Act are set to expire in 2026, meaning today’s favorable estate and income tax rules could soon disappear.

-

RMD Planning: For those with large retirement accounts, Required Minimum Distributions (RMDs) can create substantial tax burdens if not managed strategically.

3 Key Questions to Ask Yourself

Before determining your “magic number,” ask:

1. What lifestyle do I want to maintain?

Estimate annual expenses for travel, real estate upkeep, insurance, taxes, and discretionary spending.

2. What risks must I hedge against?

Consider market volatility, rising healthcare costs, longevity risk, and tax uncertainty.

3. What legacy do I want to leave?

Wealth transfer, charitable foundations, and multigenerational support can significantly affect how much you need.

A Closer Look at Retirement Spending for HNWIs

Many affluent retirees underestimate just how much their lifestyle costs, especially when it involves more than one home, frequent travel, or private schooling for grandchildren.

|

Expense Category |

Estimated Annual Range (HNWIs) |

|

Core Living Expenses |

$150,000 – $300,000+ |

|

Travel & Leisure |

$50,000 – $150,000+ |

|

Property Maintenance |

$25,000 – $100,000+ |

|

Philanthropy/Gifting |

$20,000 – $250,000+ |

|

Healthcare & Insurance |

$30,000 – $100,000+ |

|

Wealth Advisory Fees |

Varies (0.5% – 1% of AUM) |

Note: The estimated spending ranges provided are illustrative and based on aggregated insights from financial industry sources, based on aggregated data from Fidelity, Schwab, UBS, the Spectrem Group, and high-net-worth lifestyle spending reports featured in publications such as Barron’s, Forbes, and CNBC Wealth. Actual expenses will vary based on individual circumstances, lifestyle choices, geographic location, and health status. These figures are intended for educational purposes and do not constitute personalized financial advice.*

How Much Capital Do You Need? The 4% Rule Isn’t Enough

The traditional “4% rule” suggests withdrawing 4% annually from your retirement savings to avoid running out of money. For a $10 million portfolio, that would provide $400,000 per year.

But the 4% rule was built on historical data that may not hold in today’s economy. Instead, consider:

-

Tax drag: Withdrawals from pre-tax accounts may be reduced by 30%+ in taxes.

-

Lifestyle inflation: Expenses tend to rise in the early and late stages of retirement.

-

Market conditions: Sequence of returns risk could derail early retirement years.

-

Long-term care needs: Costs that can exceed $100,000/year if private or specialized.

Many HNWIs aim for a 3% or lower withdrawal rate, which means you’ll need $12–15 million in investable assets to support a $350,000+ annual lifestyle with added flexibility.

Asset Allocation for a Comfortable Retirement

Preserving and growing wealth during retirement requires balance:

-

Income-generating assets: Dividend-paying stocks, municipal bonds, and real estate.

-

Tax-efficient vehicles: Roth IRAs and charitable trusts.

-

Growth potential: Carefully selected equities, private equity, and alternatives.

-

Protection: Insurance products, structured notes, and guaranteed income strategies.

Consider reflecting both your lifestyle ambitions and your desire for capital preservation.

Planning for Longevity and Legacy

For high-net-worth retirees, the goal is often twofold:

-

Help ensure income for life.

-

Transfer wealth tax-efficiently.

Considerations for Long-Term Planning:

-

Trusts to shield assets from probate and help minimize estate taxes.

-

Gifting strategies to help reduce taxable estate while supporting heirs during your lifetime.

-

Charitable giving through donor-advised funds or private foundations.

-

Life insurance for liquidity and legacy leverage.

Without strategic planning, taxes could significantly reduce what your heirs receive, especially with estate tax exemptions set to drop in 2026.

Taxes: The Hidden Retirement Threat

It’s also important for high-net-worth retirees to be vigilant about taxes. RMDs, capital gains, and income from investments can push you into the highest tax brackets—even in retirement.

Strategies to Consider in 2025:

-

Roth conversions before 2026

-

Tax-loss harvesting in volatile markets

-

Asset location:placing tax-inefficient investments in IRAs and tax-efficient ones in brokerage accounts

-

Qualified charitable distributions (QCDs) from IRAs after age 70½

Your retirement plan should include a tax strategy that anticipates law changes and helps minimize lifetime tax liability.

How Agemy Financial Strategies Can Help Retirees Thrive

At Agemy Financial Strategies,we’re experienced in helping affluent individuals and families design a retirement strategy as unique as their lives. We understand the complexities of preserving multi-million-dollar portfolios, managing tax liability, and helping protect wealth for future generations.

Here’s what we offer:

-

Advanced estate and legacy strategies

-

Custom tax mitigation solutions

-

Investment management tailored for your risk profile and income needs

-

Fiduciary guidance every step of the way

We don’t believe in one-size-fits-all planning. We believe in personalized, proactive wealth strategy built on trust, transparency, and long-term vision.

Final Thoughts: What’s Your Number?

There’s no single dollar amount that defines a “comfortable retirement” for high-net-worth individuals. For some, $5 million in assets is enough. For others, it’s $20 million or more. The real question isn’t just how much, but how well your wealth is positioned to support your future.

The earlier you begin planning—or adjusting—the more control you’ll have.

Ready to Define Your Retirement Number?

Frequently Asked Questions

1. How much does a high-net-worth individual really need to retire comfortably in 2025?

It depends on your lifestyle, spending goals, and family legacy plans. Many HNWIs aim for $10–20 million in investable assets to generate $300,000+ in annual income, help preserve purchasing power, and leave a meaningful legacy.

2. Should I still be concerned about taxes in retirement if I’ve already accumulated wealth?

Yes. Large RMDs, capital gains, and income distributions can push you into top tax brackets. Without proactive planning—like Roth conversions, QCDs, or charitable trusts—your tax exposure could erode long-term wealth.

3. What role does longevity play in my retirement number?

Affluent individuals often have access to better healthcare and longer life expectancy. Planning for a 30- to 35-year retirement helps ensure you won’t outlive your savings or compromise your lifestyle in later years.

4. How should I adjust my asset allocation once I retire?

Your portfolio should shift toward income-generating, tax-efficient, and lower-volatility assets, while maintaining enough growth potential to keep pace with inflation and evolving spending needs.

5. How can Agemy Financial Strategies help high-net-worth individuals plan for retirement?

We’re experienced in advanced retirement income strategies, tax mitigation, legacy planning, and personalized wealth management. Our fiduciary approach helps ensure your plan is built to preserve, protect, and grow your wealth for decades to come.

Disclaimer: This content is for educational purposes only and should not be considered financial or investment advice. Please consult with the fiduciary advisors at Agemy Financial Strategies before making any investment decisions.

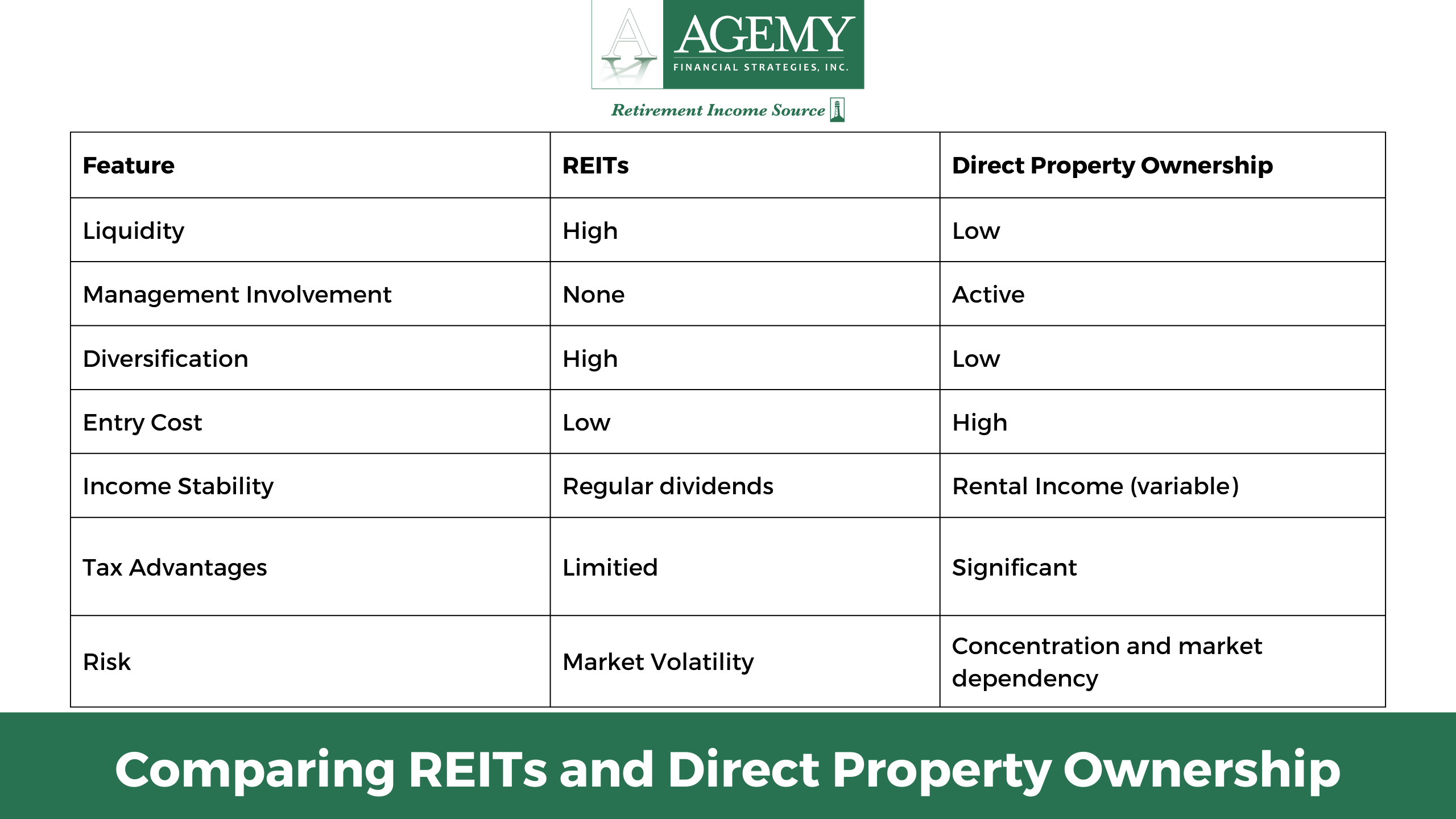

Cons of REITs

Cons of REITs

Cons of Direct Property Ownership

Cons of Direct Property Ownership