For individuals with substantial retirement savings — especially those navigating multi-million-dollar portfolios — Required Minimum Distributions (RMDs) can be one of the most complex and impactful aspects of retirement planning.

RMDs are mandated by the IRS to help ensure that tax-deferred retirement assets eventually generate taxable income. While the rules can be straightforward for smaller portfolios, when you’re managing significant wealth, RMDs intersect with broader tax planning, estate strategies, income management, investment allocation, and legacy goals.

At Agemy Financial Strategies, we believe that RMDs should not be treated as a compliance exercise; they must be integrated into a thoughtful long-term financial plan. This blog unpacks what RMDs are, how they function in large portfolios, key strategies for management, and how proactive planning can minimize taxes, maximize flexibility, and support your broader financial goals.

1. Understanding RMD Fundamentals

What Are RMDs?

Required Minimum Distributions refer to the minimum amount that individuals must withdraw annually from certain tax-deferred retirement accounts once they reach a specific age. These include:

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- 401(k), 403(b), and 457(b) plans

- Other defined contribution plans

The purpose of RMDs is to ensure that retirement savings are eventually taxed. The IRS views these assets as tax-deferred, meaning contributions and earnings grow without annual tax until withdrawn.

When Do RMDs Start?

Following recent tax law changes, RMDs generally begin at age 73 for those who reach 72 after December 31, 2022; for those who reached 72 before this date, the prior RMD age still applies. The rules change over time, so periodic review with a financial advisor is critical.

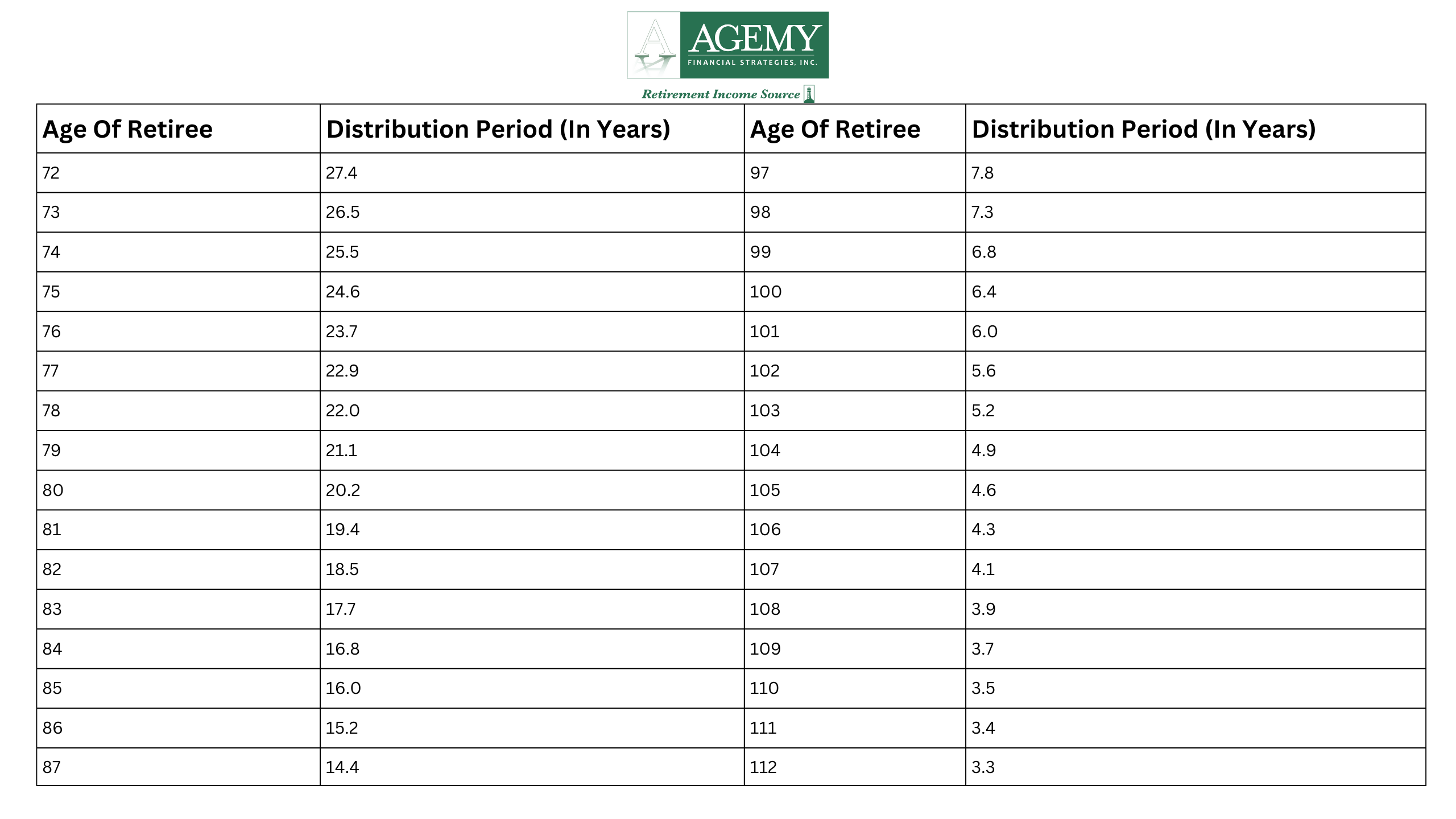

How Are RMDs Calculated?

RMD amounts are based on your account balance as of December 31 of the prior year and your life expectancy factor from IRS tables. For high-net-worth individuals with multi-million-dollar accounts, this calculation often results in substantial distributions that can significantly impact taxable income.

For example, if your IRA balance was $4 million on December 31 and your IRS life expectancy divisor is 25.6 (a hypothetical from IRS tables), your RMD would be approximately:

$4,000,000 ÷ 25.6 = $156,250

This distribution is taxable as ordinary income and must be taken before the RMD deadline (generally December 31).

2. RMD Challenges for Multi-Million-Dollar Portfolios

When account balances are significant, RMDs present unique challenges:

Tax Liability Can Increase Dramatically

Large distributions can push you into higher marginal tax brackets, increasing your overall tax burden. Even if you don’t “need” the money for living expenses, the IRS requires you to take these withdrawals and pay taxes on them.

Bracket Creep and the Impact on Cash Flow

“Bracket creep” occurs when RMDs increase your taxable income significantly enough to move you into a higher tax bracket. This shift can also affect how Social Security benefits are taxed, Medicare premiums, and eligibility for certain tax deductions or credits.

Compounding Effects Over Time

Because RMDs are recalculated annually based on the prior year’s balance, poor market performance or strategic rebalancing can increase or decrease future RMDs unpredictably.

3. Strategic Approaches to RMD Management

To stay ahead of RMD issues and optimize outcomes, high-net-worth investors should consider a suite of strategies:

A. Roth Conversions Before RMD Age

One of the most powerful tools in RMD planning is the Roth IRA conversion. Unlike traditional IRAs, Roth IRAs do not have RMDs during the owner’s lifetime.

How it helps:

- Reduces future RMD amounts because assets moved to a Roth no longer count toward RMD calculations.

- Grew absolutely tax-free — qualified withdrawals, including earnings, are not taxable.

- Converts when tax rates are relatively low, potentially saving more in the long run.

Considerations:

- Roth conversions are taxable events. You’ll owe income tax the year of conversion.

- Timing matters: converting too much in a single year can spike your tax bracket.

- A well-timed conversion plan can balance tax liability while reducing future RMDs.

B. Qualified Charitable Distributions (QCDs)

Charitable giving can be both philanthropic and tax-efficient through Qualified Charitable Distributions (QCDs).

What is a QCD?

- A direct transfer from your IRA to a qualified charity.

- Only available for individuals age 70½ and older.

- Up to $100,000 per year can count toward your RMD without being included in taxable income.

Why it matters:

- QCDs help reduce taxable RMD income.

- They satisfy your RMD requirement while supporting causes you care about.

- Especially useful for wealthy retirees with philanthropic goals.

C. Timing and Frequency of RMDs

Although RMDs must be completed by year-end, you have flexibility in when and how often withdrawals occur:

- Lump sum: simple, but can spike income.

- Periodic distributions (monthly, quarterly): smooths income and may help with tax planning.

- Planned timing with cash flow needs: aligns distributions with expenses or investment rebalancing.

D. Tax Diversification: Balance Between Account Types

A diversified retirement portfolio should include:

- Tax-deferred accounts (Traditional IRA/401k)

- Tax-free accounts (Roth IRAs)

- Taxable investment accounts

With these layers, you gain flexibility in withdrawal strategies that can help minimize the tax impact of RMDs. For example:

- Use taxable accounts to fund spending needs early in retirement.

- Defer tax-deferred withdrawals until required.

- Use Roth assets strategically to manage income in high tax years.

E. Strategic Asset Location

This involves placing investments in the accounts where they’re most tax-efficient:

- High-growth assets (like equities) may be better in tax-free or tax-deferred accounts.

- Low-yield assets may live in taxable accounts.

- Municipal bonds often suit taxable accounts because of tax-free interest.

Proper asset location can help reduce taxes over time and affect RMD outcomes.

4. RMDs and Estate Planning

For high-net-worth individuals, RMDs intersect strongly with estate planning. The decisions you make now will shape how your assets pass to heirs, how taxes are applied, and how your legacy is preserved.

A. Stretch or Inherited IRAs

Prior to the SECURE Act of 2019, beneficiaries could “stretch” IRA distributions over their lifetime. Today, most non-spouse beneficiaries must distribute accounts within 10 years, accelerating taxable income.

Key impacts:

- Heirs may face steep tax bills if distributions are large.

- Strategic planning during your lifetime can mitigate tax shock for beneficiaries.

B. Trusts and Beneficiary Designations

Aligning beneficiary designations and trust structures with your overall estate plan helps ensure that assets flow as intended.

- Carefully drafted trust language, especially for retirement accounts, can prevent unintended tax consequences.

- Coordination between your financial advisor and estate attorney is vital.

C. Gifting Strategies

Gifting retirement assets before death can help reduce the size of your RMD base.

- Lifetime gifts reduce the value of your taxable estate.

- Some clients use gifts to transfer assets to children or trusts, aligning with legacy plans.

5. Navigating RMD Pitfalls and Avoiding Costly Mistakes

Given the complexity of RMD rules, even sophisticated investors can make costly errors. Here are common pitfalls we help clients avoid:

A. Missing the Deadline

The deadline for taking an RMD is usually December 31, with one exception for the first RMD, which can be delayed until April 1 of the year after you reach the required age. However, delaying can lead to two RMDs in one year, doubling taxable income in that tax year.

Penalty for missing an RMD?

The IRS penalty used to be a shocking 50% of the amount not withdrawn. While it has been reduced (to 25% or potentially 10% for corrected distributions), it’s still significant.

B. Miscalculating the Amount

Using incorrect life expectancy tables or outdated IRS rules can lead to under-distribution, exposing you to penalties.

We always verify:

- Current IRS life expectancy tables

- Correct account values

- Proper calculation methods

- Updated rules after legislative changes

C. Ignoring Market Impact

If market values drop, RMDs based on prior high valuations can force distributions during unfavorable conditions:

Example:

If a portfolio fell 20% after December 31, you may be forced to liquidate assets at a loss to meet your RMD.

Solution?

- Maintain sufficient liquidity outside of your retirement account.

- Rebalance regularly to avoid forced selling.

D. Overlooking State Tax Implications

State income taxes vary widely. Some states tax retirement income; others do not. For high-net-worth retirees who split time between states or relocate in retirement, state tax planning is crucial.

6. Modeling RMD Impact: A Hypothetical Case Study

To illustrate the strategic power of RMD planning, let’s consider a hypothetical scenario.

Client Profile

- Age: 74

- Traditional IRA: $6,500,000

- Roth IRA: $1,500,000

- Taxable Investments: $3,000,000

- Tax bracket: 32%

- Charitable goals: $50,000/year

Scenario: No Strategy Applied

- RMD calculated at $6.5M ÷ 22.0 (hypothetical divisor) = $295,455

- Total taxable income jump due to RMD

- No QCDs or Roth conversions

- Result: higher tax bracket, increased Medicare premiums, reduced flexibility

Tax consequence? Potentially several tens of thousands more in taxes annually.

Strategic Plan Implemented

Year 1:

- Roth conversion of $500,000

- QCD of $50,000

- RMD adjusted with a mix of periodic distributions and QCDs

Result:

- Smaller future RMD base

- Reduced taxable income year over year

- Philanthropic goals met tax-efficiently

Long-term impact:

- Reduced tax drag over decades

- More assets left to heirs with favorable tax positioning

- Greater control over income timing

7. Partnering with Agemy Financial Strategies for RMD Excellence

RMD planning isn’t one-and-done. It’s continuous. Changes in tax rules, market performance, personal goals, and estate priorities all influence the plan. That’s why high-net-worth investors choose a proactive partner.

What We Provide

- Customized RMD modeling and forecasting

- Roth conversion strategy tailored to your tax situation

- Charitable planning using QCDs and donor-advised funds

- Tax-efficient withdrawal sequencing

- Coordination with estate and tax professionals

- Ongoing review as laws and circumstances evolve

8. Final Thoughts: RMDs as a Strategic Lever, Not a Mandate

For many retirees, RMDs are viewed with frustration as an unavoidable headache. But for wealthy investors, they are also a strategic lever for:

- Tax planning

- Cash flow management

- Legacy design

- Charitable impact

With thoughtful planning, RMDs don’t have to be a tax burden; they can be an opportunity to align retirement income with your long-term goals.

At Agemy Financial Strategies, we help our clients see beyond the numbers to the impact those withdrawals have on lifestyle, family, and legacy. If you’re managing a multi-million-dollar portfolio and want to ensure your RMD strategy is optimized for tax efficiency, flexibility, and peace of mind, we’re here to help.

Contact us today at agemy.com.

Investment advisory services are offered through Agemy Wealth Advisors, LLC, a Registered Investment Advisor and fiduciary to its clients. Agemy Financial Strategies, Inc. is a franchisee of Retirement Income Source®, LLC. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC are associated entities. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC entities are not associated with Retirement Income Source®, LLC. The information contained in this e-mail is intended for the exclusive use of the addressee(s) and may contain confidential or privileged information. Any review, reliance or distribution by others or forwarding without the express permission of the sender is strictly prohibited. If you are not the intended recipient, please contact the sender and delete all copies. To the extent permitted by law, Agemy Financial Strategies, Inc and Agemy Wealth Advisors, LLC, and Retirement Income Source, LLC do not accept any liability arising from the use or retransmission of the information in this e-mail.

Key Changes to RMDs for 2025

Key Changes to RMDs for 2025