September 16, 2024

We’re all familiar with Required Minimum Distributions (RMDs), but new rules have made it more crucial than ever to plan carefully. Failure to do so could result in a costly tax burden and erode your retirement savings. In this blog, we’ll explore strategies to optimize your RMDs and avoid financial pitfalls, while also uncovering a lesser-known RMD trap that could impact your retirement healthcare plan.

Retirement should be about enjoying the fruits of your labor, not worrying about complicated financial decisions. Yet, one decision that often goes overlooked is what to do with your Required Minimum Distributions (RMDs). For many retirees, the default action might be to deposit these funds directly into their checking accounts. Still, this approach can lead to missed opportunities for tax efficiency, growth, and strategic financial planning. But there’s good news—you have options.

Let’s dive into smarter ways to handle your RMDs, helping ensure they align perfectly with your retirement goals and keep your money working for you.

Understanding RMDs

Required Minimum Distributions (RMDs) are mandatory withdrawals from certain tax-advantaged retirement accounts that owners must make at retirement age. The IRS states this age threshold to help ensure retirees begin drawing down their retirement savings and paying taxes on deferred income. The Secure 2.0 Act raised the age that account owners must begin taking RMDs. For 2023, the age at which account owners must start taking required minimum distributions goes up from age 72 to age 73, so individuals born in 1951 must receive their first required minimum distribution by April 1, 2025.

Understanding the timing and requirements for RMDs is crucial for retirement planning. While RMDs are unavoidable, how you manage them can significantly impact your financial health and long-term retirement strategy. To estimate your RMDs, use our free online RMD Calculator here. Consulting with a fiduciary advisor can help ensure compliance with RMD rules.

Why Avoid Dumping RMDs into Checking Accounts?

If you don’t immediately need the cash from your RMDs, there are smarter ways to handle these funds than depositing them into a checking account. By exploring alternative strategies, you can make your RMDs work harder for you. Here’s why avoiding a direct deposit into your checking account might be the better choice:

- Potential Tax Implications: Moving your RMDs straight into a checking account can inflate your taxable income, potentially pushing you into a higher tax bracket. This can also affect your Social Security benefits and Medicare premiums.

- Missed Growth Opportunities: Cash sitting in a checking account typically earns little to no interest. By reinvesting or reallocating these funds wisely, you can continue to grow your wealth even in retirement.

- Overspending Risk: A large influx of cash into a checking account can tempt some retirees to overspend, derailing their carefully planned retirement budgets.

Before making any withdrawals, it’s advisable to consult with a fiduciary to understand the tax implications fully. They can provide personalized guidance based on your financial situation and help you make informed decisions about your retirement withdrawals.

1. Reinvest in a Taxable Brokerage Account

1. Reinvest in a Taxable Brokerage Account

One of the most straightforward ways to keep your RMDs working for you is to reinvest them in a taxable brokerage account. While this won’t shield you from taxes on your RMDs, it allows your money to grow. Here’s how it works:

- Growth Potential: By investing in a diversified portfolio of stocks, bonds, and other assets, you can earn a return that outpaces inflation.

- Flexibility: Unlike retirement accounts, taxable accounts offer the flexibility to withdraw funds without penalties, making them ideal for funding major expenses or managing cash flow needs.

2. Qualified Charitable Distributions (QCDs)

Before diving into charitable giving, reflecting on your values and philanthropic goals is essential. Consider the impact you aspire to create and whether you lean towards supporting local, national, or international charities. If you are charitably inclined, QCDs may be an option for you.

Each year, an IRA owner age 70½ or over when the distribution is made can exclude from gross income up to $100,000 of these QCDs. For a married couple, if both spouses are age 70½ or over when the distributions are made and both have IRAs, each spouse can exclude up to $100,000 for a total of up to $200,000 per year. This strategy counts toward your RMD but is not included in your taxable income, providing a win-win situation:

- Tax Benefits: QCDs reduce your taxable income, which can help keep your overall tax bill lower.

- Philanthropic Impact: Supporting causes you care about can be a fulfilling way to utilize your RMDs.

Working alongside a fiduciary advisor can help you evaluate how well your contributions align with your goals. Be open to adjusting your giving strategy as your circumstances and priorities evolve.

3. Set Up a Roth Conversion Ladder

A Roth conversion involves transferring funds from a Traditional IRA or 401(k) into a Roth IRA, requiring you to pay taxes on the amount converted. Unlike regular contributions, there is no limit on the amount you can convert — the annual contribution limit ($7,000 or $8,000 if you’re 50 or older) does not apply to conversions. This strategy can be tailored to your unique financial situation to maximize the benefits of a Roth IRA.

Although you cannot directly convert RMDs, you can strategically plan Roth conversions to reduce future RMDs:

- Tax-Free Withdrawals: Funds in a Roth IRA grow tax-free, and withdrawals are tax-free, providing flexibility and tax efficiency in later years.

- RMD Exemption: Roth IRAs are not subject to RMDs during your lifetime, giving you more control over your retirement assets.

You can use the IRS’s Uniform Lifetime Table to determine the amount you need to withdraw. Working with a fiduciary advisor can help you effectively manage RMD withdrawals. With strategic planning, you can optimize your retirement income and minimize unnecessary tax burdens.

4. Purchase a Deferred Income Annuity

4. Purchase a Deferred Income Annuity

A Deferred Income Annuity (DIA) can be a valuable tool if you want to secure a reliable income stream in your later years. Using a portion of your RMDs to purchase a DIA, you can convert a lump sum into guaranteed payments that begin at a future date, often several years later. Here are some benefits that can offer you peace of mind

- Customized Payments: Payments can be tailored to start at a specific age, providing predictable income to cover essential expenses.

- Higher Payouts: The monthly payments will be larger for longer deferral periods. This helps you to benefit from increased income when you need it most.

- Tax-Deferred Growth: During the deferral period, your funds grow on a tax-deferred basis. This can be particularly advantageous for those in higher tax brackets who wish to delay the taxable event in the future.

With the flexibility to customize payments and the security of guaranteed income, a DIA could be a vital component of a well-rounded retirement plan. Discuss this option with a fiduciary advisor to determine how it fits your overall strategy.

5. Fund a 529 Plan for Grandchildren’s Education

RMDs can also be a tool for leaving a legacy for future generations. By funding a 529 plan, you can help pay for a loved one’s education expenses while also removing taxable income from your estate:

- Tax-Free Growth: Investments in 529 plans grow tax-free, and withdrawals for qualified education expenses are also tax-free.

- Gift of Education: Helping with education costs can be a meaningful way to support future generations without impacting your standard of living.

A Second RMD Hidden Healthcare Trap

Healthcare is expensive, especially as we age – which is why properly planning for these costs now can help your nest egg in your golden years. Did you know 2024 Medicare Part B & D Premiums are based on income? And RMDs may be pushing you into higher Medicare Part B & D Premiums!

As individuals progress through their retirement years, understanding the factors that influence Medicare premiums is crucial. These factors include earned and self-employment income, investment returns, real estate and rental income, retirement withdrawals, Social Security benefits, and pensions.

| Beneficiaries who file individual tax returns with modified adjusted gross income: | Beneficiaries who file joint tax returns with modified adjusted gross income: | Part B Premium | Part D Surcharge |

| Less than or equal to $103,000 | Less than or equal to $206,000 | $174.70 | |

| Greater than $103,000 and less than or equal to $129,000 | Greater than $206,000 and less than or equal to $258,000 | $244.60 | $12.90 |

| Greater than $129,000 and less than or equal to $161,000 | Greater than $258,000 and less than or equal to $322,000 | $349.40 | $33.30 |

| Greater than $161,000 and less than or equal to $193,000 | Greater than $322,000 and less than or equal to $386,000 | $454.20 | $53.80 |

| Greater than $193,000 and less than $500,000 | Greater than $386,000 and less than $750,000 | $559.00 | $74.20 |

| Greater than or equal to $500,000 | Greater than or equal to $750,000 | $594.00 | $81.00 |

Required Minimum Distributions (RMDs) can push you into higher Medicare Part B and Part D premiums because they are considered taxable income. When you take RMDs from your retirement accounts, the amount is added to your adjusted gross income (AGI). If this increase pushes your AGI above certain thresholds, it can cause your Medicare premiums to rise due to the Income-Related Monthly Adjustment Amount (IRMAA).

IRMAA is a surcharge that applies to higher-income Medicare beneficiaries. For those whose income exceeds certain limits, IRMAA can significantly increase the monthly premiums for both Medicare Part B (medical insurance) and Part D (prescription drug coverage). As a result, large RMDs may unintentionally trigger higher Medicare costs, affecting your overall retirement budget.

To avoid having your Required Minimum Distributions (RMDs) push you into higher Medicare Part B and D premiums, consider the following strategies:

- Qualified Charitable Distributions (QCDs): If you’re 70½ or older, you can direct up to $100,000 of your RMD to a qualified charity. This amount won’t be included in your taxable income, helping keep your income below the IRMAA thresholds.

- Roth Conversions: Converting traditional IRA or 401(k) assets to a Roth IRA can reduce future RMDs, as Roth IRAs are not subject to RMDs during the owner’s lifetime. Converting in years with lower income can minimize the tax impact.

- Strategic Withdrawals Before RMD Age: Consider taking withdrawals before you reach the age for mandatory RMDs (age 73) to reduce the size of your retirement account and thus lower future RMD amounts.

- Delay Social Security Benefits: If possible, delay claiming Social Security benefits to reduce your taxable income. This can help you stay under the income thresholds for higher Medicare premiums.

- Income Smoothing: Spread out withdrawals over several years to avoid large, lump-sum withdrawals that could push you into a higher income bracket.

- Monitor Your Income: Keep track of your Modified Adjusted Gross Income (MAGI) and plan withdrawals accordingly to stay below the IRMAA thresholds for Medicare premiums.

- Use Tax-Efficient Investments: Consider investing in tax-efficient accounts or assets that produce less taxable income, helping to control the amount that could push you over the threshold.

By carefully planning your retirement income and utilizing these strategies, you can minimize the impact of RMDs on your Medicare premiums. Consulting with a financial advisor can also help tailor a plan that suits your specific situation.

Working With a Fiduciary Advisor

When it comes to optimizing RMDs, each strategy has nuances and potential financial implications. Tax laws regarding RMDs, Medicare/income bracket changes, and charitable giving law adjustments mean your retirement income strategy must also adapt. Staying informed is crucial to maximizing the benefits of your RMDs. At Agemy Financial Strategies, we are here to offer in-depth insights into your specific RMD responsibilities and explore tax-efficient strategies for RMD management.

Our trusted fiduciary advisors can help you fulfill your legal obligations and provide personalized guidance to optimize your financial situation within the bounds of IRS regulations. We work with you to help assess your retirement income needs and craft a tailored plan aligned with your unique financial goals. Please refer to our service offerings page for a comprehensive list of our services, and don’t forget you can access our free online RMD Calculator here at any time.

Final Thoughts

Avoiding the simple transfer of RMDs into a checking account opens up opportunities to enhance your financial security and make meaningful contributions to your future and those you care about. And planning for Medicare changes along the way will help you avoid unnecessary financial surprises further down the road.

For personalized guidance and to explore the best strategies for your specific needs, consider consulting with Agemy Financial Strategies. Our team of fiduciary advisors is dedicated to helping you navigate the complexities of retirement planning and ensure your RMDs are managed per your goals.

Contact us today to learn more and set up a complimentary consultation.

Understanding the Retirement Landscape

Understanding the Retirement Landscape

Common Mistakes to Avoid

Common Mistakes to Avoid

The Importance of Healthcare in Retirement

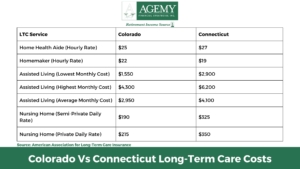

The Importance of Healthcare in Retirement Below is a comparison of long-term care costs between

Below is a comparison of long-term care costs between