For high-net-worth individuals (HNWIs), effective tax planning is just as important as investment growth when it comes to long-term wealth preservation. With the top marginal tax rate in the U.S. at 37% and potential estate tax exemptions set to decline after 2025, strategic tax planning can make a significant impact on reducing liabilities and maximizing financial efficiency.

A well-structured tax strategy allows HNWIs to legally minimize tax burdens, provide compliance with evolving regulations, and preserve more wealth for future generations. In this blog, we explore four essential tax planning strategies to help you optimize your financial position while staying ahead of tax obligations.

Why Having a Tax Strategy is Important

Without strategic tax planning, these factors can significantly erode wealth over time. A proactive tax strategy minimizes tax liability and helps ensure that your investments, estate, and philanthropic efforts align with your long-term financial goals.

- Preserve Wealth: Reducing tax liabilities allows you to keep more earnings and investment gains.

- Enhances Investment Returns: Tax-efficient investing can improve net returns by providing the right assets in the most tax-advantaged accounts.

- Optimizes Charitable Giving: Smart gifting strategies allow you to support causes you care about while receiving tax benefits.

- Safeguards Your Estate: Proper estate planning can help reduce the tax burden on heirs, allowing more of your wealth to be passed down.

By implementing a proactive tax strategy, you can maximize your financial efficiency, maintain compliance with evolving tax laws, and make informed decisions about wealth management. Let’s explore four key tax planning strategies to help you achieve these goals.

1. Optimize Charitable Giving with Strategic Donations

Charitable giving is a powerful tool for tax planning. It allows you to support causes that matter to you while reducing your taxable income. HNWIs have multiple avenues to help structure their giving to maximize tax benefits. Here are some key strategies for charitable giving:

- Donor-Advised Funds (DAFs): These allow you to donate assets and receive an immediate tax deduction while deciding which charities to support later.

- Qualified Charitable Distributions (QCDs): If you’re 70½ or older, you can donate up to $100,000 directly from an IRA to a charity without counting it as taxable income.

- Charitable Remainder Trusts (CRTs): These provide income during your lifetime while benefiting a charity upon passing, offering estate and income tax benefits.

With recent changes in tax laws, considering long-term charitable strategies can enhance your philanthropic impact while securing favorable tax advantages.

2. Leverage Tax-Advantaged Accounts for Retirement and Investment Growth

Even for HNWIs, tax-advantaged accounts provide valuable opportunities to defer or reduce taxes on investment gains. Proper allocation across these accounts can help yield potential benefits over time. Here are some types of tax-advantaged accounts to consider:

- Roth IRA Conversions: While you’ll pay taxes on the conversion amount, your investments grow tax-free, and withdrawals in retirement are not subject to income tax.

- Health Savings Accounts (HSAs): For those with high-deductible health plans, HSAs offer triple tax benefits: contributions are tax-deductible, investments grow tax-free, and withdrawals for qualified medical expenses are tax-free.

- Life Insurance as an Estate Planning Tool: Properly structured life insurance policies can provide tax-free income to beneficiaries while helping mitigate estate tax burdens.

Implementing a strategic approach to utilizing these accounts can help ensure tax efficiency in both the short and long term. Working alongside a fiduciary advisor can help you leverage these accounts.

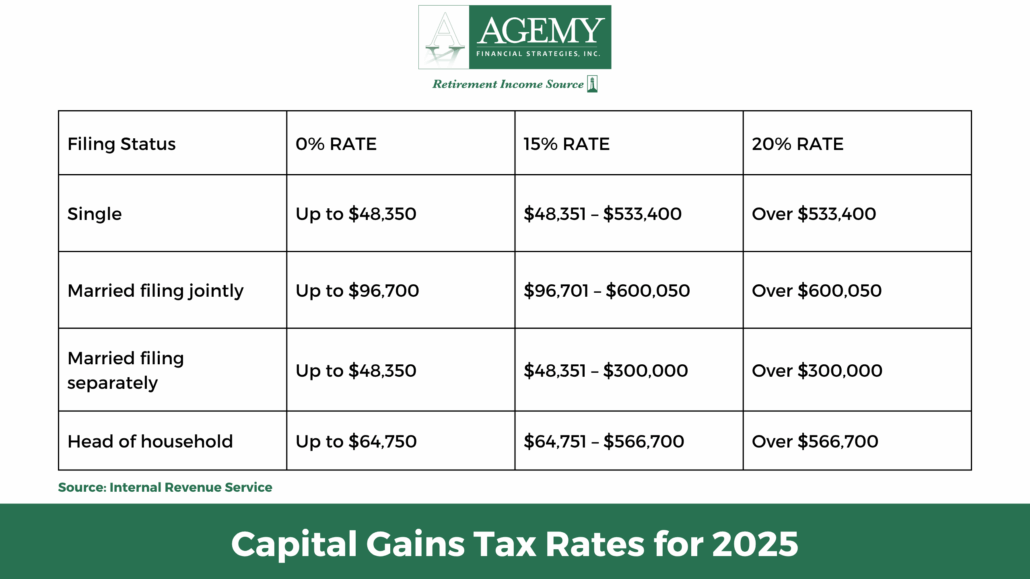

3. Minimize Capital Gains Taxes Through Tax-Loss Harvesting and Asset Location

Capital gains taxes can significantly impact wealth accumulation, particularly for HNWIs with diversified investment portfolios. You can reduce tax liabilities and optimize after-tax returns by strategically managing how and when you sell investments.

- Tax-Loss Harvesting: Offsetting capital gains by selling underperforming investments can help lower your tax bill while maintaining a similar asset allocation.

- Holding Period Strategies: Long-term capital gains rates are significantly lower than short-term rates. Holding investments for more than one year before selling can help reduce taxes.

- Asset Location Optimization: Placing tax-inefficient investments (such as bonds and REITs) in tax-advantaged accounts while keeping tax-efficient investments (like index funds) in taxable accounts can improve overall tax efficiency.

Understanding how different investments are taxed—and strategically aligning them—can help you preserve more of your returns. Working with a knowledgeable advisor helps your portfolio be structured in a way that optimizes tax efficiency while supporting your long-term financial goals.

4. Plan for Estate and Gift Taxes to Preserve Generational Wealth

4. Plan for Estate and Gift Taxes to Preserve Generational Wealth

Estate and gift taxes can take a significant portion of wealth if not strategically managed. Understanding how these taxes operate and interact is essential for crafting a comprehensive wealth preservation strategy. Let’s explore each tax in detail:

- Estate Tax: The exemption amount for people who pass away in 2025 is $13.99 million. Married couples can expect their exemption to be $27.98 million.

- Annual Gift Exclusion: You can gift up to $19,000 per recipient, a $1,000 increase from the 2024 limit. Couples can gift up to $38,000 per recipient without triggering gift tax reporting requirements.

- Lifetime Gift Tax Exemption: The current lifetime exemption stands at $13.99 million per individual, but planning for potential reductions in the exemption can help mitigate future tax burdens.

By proactively planning your estate, you can maximize the wealth passed to future generations while reducing unnecessary tax liabilities.

How Agemy Can Help You with Tax Planning

Navigating the complexities of tax planning can be overwhelming, especially with ever-changing tax laws, investment implications, and estate planning considerations. At Agemy Financial Strategies, our fiduciary advisors work alongside you to create a tailored tax strategy that aligns with your wealth management goals. With a focus on transparency and strategy, our team helps HNWIs:

- Identify Tax-Efficient Investment Strategies: We analyze your investment portfolio to help optimize asset location, maximize tax efficiency, and manage capital gains.

- Mitigate Estate and Gift Tax Burdens: Our team helps structure estate plans to minimize tax liability and protect generational wealth.

- Optimize Retirement and Tax-Advantaged Accounts: We guide you on Roth conversions, tax-efficient withdrawals, and leveraging accounts like HSAs and IRAs.

- Strategize Philanthropic Giving: We help structure charitable contributions through donor-advised funds, trusts, and other vehicles that can potentially benefit your estate and the causes you care about.

Final Thoughts

Effective tax planning is a crucial component of wealth preservation for HNWIs. Staying informed and proactive in your tax strategy helps ensure that your wealth continues to work for you and your family, both now and in the future.

At Agemy Financial Strategies, we help HNWIs develop tax-efficient wealth management plans tailored to their unique financial goals. Our fiduciary advisors provide guidance to help you maximize tax savings, protect your assets, and build a strong financial future.

Contact us today to schedule your complimentary consultation and start planning for a more tax-efficient future.

Frequently Asked Questions (FAQs)

1. How do tax laws impact HNWIs differently than average taxpayers?

HNWIs often face higher marginal tax rates, exposure to estate and gift taxes, and alternative minimum tax (AMT) considerations. Strategic tax planning is essential to help mitigate these factors. Our fiduciary advisors help HNWIs navigate complex tax laws by implementing strategies that help optimize tax efficiency while staying compliant.

2. Are Roth conversions a good strategy for HNWIs?

Roth conversions can be beneficial if done strategically, particularly in lower-income years or before RMDs begin. They help lock in tax-free growth and withdrawals in retirement. Agemy Financial Strategies provides personalized guidance on timing and executing Roth conversions to minimize tax liability and maximize long-term benefits.

3. What happens if the estate tax exemption is reduced?

If the exemption decreases, more estates will be subject to taxation. Proactive gifting strategies can help mitigate the impact. Our advisors work closely with you to help structure your wealth transfers efficiently, allowing more of your assets to be preserved for future heirs and beneficiaries.

4. Can tax-loss harvesting be done year-round?

Tax-loss harvesting can be executed throughout the year, but many investors optimize it toward year-end to offset capital gains from other investments. If you want to integrate tax-loss harvesting into your investment approach, our fiduciary advisors can help you.

5. How do charitable donations reduce my tax bill?

Charitable contributions can lower taxable income, and depending on the donation type (cash, stocks, trusts), they may provide additional tax benefits such as avoiding capital gains taxes. Agemy Financial Strategies helps clients develop a strategic giving plan that maximizes their charitable impact and tax efficiency.

Disclaimer: This blog is for informational purposes only and should not be considered specific tax, legal, or investment advice. Tax laws are subject to change, and individual circumstances vary. Please consult with the qualified financial professionals at Agemy Financial Strategies before implementing any of the strategies discussed.

1. Smart Asset Location: Putting Investments in the Right Accounts

1. Smart Asset Location: Putting Investments in the Right Accounts

4. Maximizing Retirement Account Contributions

4. Maximizing Retirement Account Contributions The Importance of Proactive Tax Planning

The Importance of Proactive Tax Planning