Latest News

Everything thats going on at Enfold is collected here

Hey there! We are Enfold and we make really beautiful and amazing stuff.

This can be used to describe what you do, how you do it, & who you do it for.

REITs vs. Direct Property Ownership: Pros and Cons for Investors

News, Real EstateReal estate has long been a cornerstone of wealth-building, offering opportunities for steady income, diversification, and long-term growth. For those approaching retirement, it’s not just about whether to include real estate in your portfolio—it’s about choosing the right approach to suit your goals and lifestyle.

Deciding what to do with yourself in the period between Christmas and the New Year can feel confusing for us all. More unsettling? The daunting decision between Real Estate Investment Trusts (REITs) and direct property ownership! While the festivities take a quick break, use your time off to research each option, as each has its own benefits and challenges, making it essential to understand how they align with your financial plans.

This blog dives into the pros and cons of both strategies, helping you make informed decisions and position your real estate investments for success in retirement.

What Are REITs?

Real Estate Investment Trusts (REITs) own, operate, or finance income-generating real estate. They pool funds from multiple investors, allowing shareholders to own a portion of large-scale properties without directly managing them. REITs are traded on public stock exchanges, making them an accessible and liquid investment vehicle.

More than 45% of American households own REITs, nearly double the estimate from two decades ago. They can be a good fit if you want the diversification benefits of real estate without the commitment and responsibilities of directly owning property. To better understand how REITs work, let’s explore the three main types available to investors, each with unique features and benefits:

Now that we know more about what REITs entail let’s look at the pros and cons.

Pros of REITs

One of the most significant benefits of REITs is their high liquidity. Since REIT shares are traded on stock exchanges, investors can quickly buy or sell them, unlike physical real estate transactions, which can take weeks or months. This liquidity is particularly advantageous for investors needing immediate access to funds without being locked into long-term real estate ownership.

REITs allow investors to spread their exposure across various properties, sectors, and geographies. For example, a single REIT may include assets like shopping malls, apartment complexes, healthcare facilities, and industrial warehouses. This built-in diversification can help reduce the risk of potential loss that could occur if an individual property or sector underperforms. It’s an efficient way to participate in the real estate market without the concentration risk of owning one or two properties.

REITs offer a low barrier to entry compared to direct property ownership. Instead of needing tens or hundreds of thousands of dollars for a down payment on a property, investors can gain exposure to real estate markets with the cost of a single REIT share. This accessibility can make REITs a practical choice for small-scale investors or those just starting to diversify their portfolios into real estate.

Since REITs are traded on stock exchanges, they are subject to the same market volatility as other publicly traded securities. Their values can fluctuate based on economic conditions, interest rates, or changes in investor sentiment, regardless of the underlying real estate performance. This volatility can be challenging for investors seeking stability or those uncomfortable with the stock market’s swings.

Investing in REITs means relinquishing decision-making power to the REIT’s management team. Investors cannot control which properties the REIT buys, sells, or develops. This lack of control can be a drawback for those who prefer a hands-on approach to managing their investments or want to focus on specific property types or locations.

While REITs often pay attractive dividends, these payouts are typically taxed as ordinary income rather than benefiting from the lower tax rates associated with qualified dividends or long-term capital gains. This can result in a higher tax burden for investors, particularly those in higher tax brackets. For tax efficiency, REITs may be better suited for tax-advantaged accounts like IRAs or 401(k)s.

What Is Direct Property Ownership?

Direct property ownership involves purchasing and owning physical real estate, such as residential properties, commercial spaces, or undeveloped land. Investors earn income by leasing the property or profiting from its appreciation over time. This approach requires hands-on involvement or the hiring of property management services.

Unlike REITs, direct ownership gives investors full control over property management and decision-making. However, it comes with responsibilities like tenant management, property upkeep, and navigating real estate market fluctuations.

Let’s look deeper at the pros and cons of direct property ownership.

Pros of Direct Property Ownership

One of the primary benefits of direct property ownership is the ability to build equity over time. As you pay down the mortgage, your ownership stake in the property increases. This creates a valuable asset that can be leveraged for future investments or financial needs. Unlike other investments, real estate allows you to combine equity growth with income generation, such as rental payments, making it a powerful wealth-building tool.

Real estate has a historical tendency to appreciate over time, offering investors the potential for substantial capital gains. Investors can benefit from increasing property values by holding long-term property long-term, particularly in growing markets or areas with rising demand. This potential for growth makes real estate a valuable component of a long-term investment strategy.

Real estate is often considered a natural hedge against inflation because property values and rental income typically rise over time, outpacing it. This ability to preserve and potentially increase purchasing power during inflationary periods makes real estate a reliable store of value. This characteristic makes direct property ownership particularly attractive for investors seeking long-term stability.

One of the most significant drawbacks of owning physical property is its lack of liquidity. Unlike REITs or stocks, selling a property can take several months and involves high transaction costs, including real estate agent commissions, closing fees, and potential repairs or upgrades to prepare the property for sale. This lack of liquidity can be a drawback for retirees who need quick access to funds.

Direct property ownership requires active involvement, making it far from a passive investment. Owners are responsible for property maintenance, tenant relations, and compliance with local laws and regulations. Even when hiring a property manager, the owner is ultimately accountable for decisions and outcomes, which can still demand time and effort.

The value and income real estate generates are heavily influenced by local market conditions, economic trends, and interest rate fluctuations. For instance, an economic downturn or oversupply of rental properties in a specific area can lead to declining property values and rental income. Similarly, rising interest rates can make mortgages more expensive, reducing affordability and demand. These factors can create unpredictable fluctuations in income and value, requiring property owners to carefully research and monitor market conditions to mitigate risks.

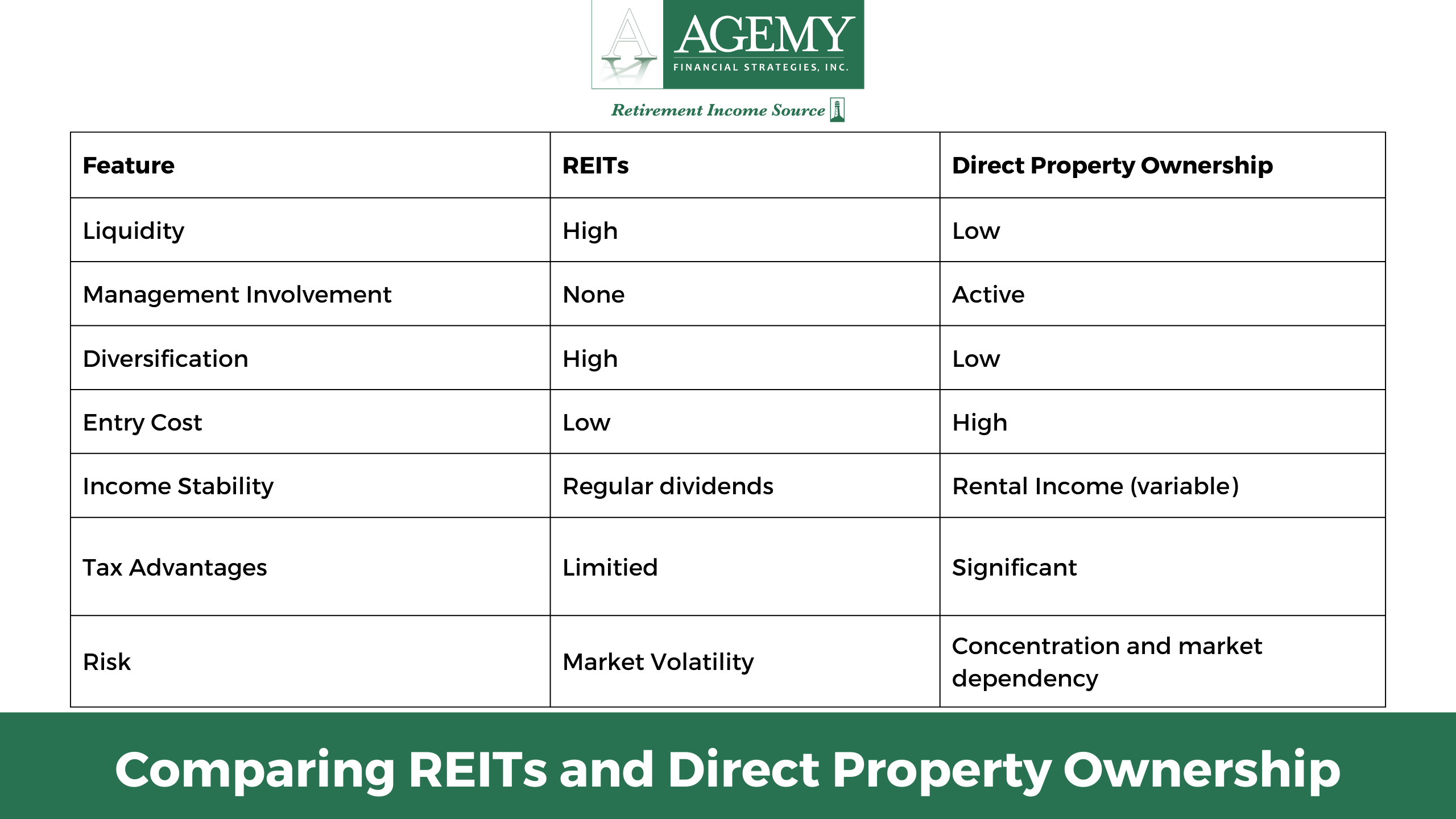

Key Considerations for Investors

Choosing between REITs and direct property ownership depends on your financial goals, time horizon, risk tolerance, and tax strategy. Each option has unique strengths and potential drawbacks; understanding these factors can help you make an informed decision.

To make this decision easier, we’ve outlined the key differences between REITs and direct property ownership in the table below. Use it as a quick reference to compare their features side by side:

Partner With a Fiduciary Advisor

Investing in real estate during retirement can pose complexities, especially for those managing significant portfolios. If you’re looking for a fiduciary advisor with extensive experience in real estate investments, Agemy Financial Strategies is here to help.

Fiduciary advisors are legally obligated to prioritize your best interests, delivering impartial advice and recommendations aligned with your financial goals. Our seasoned professionals can help you identify opportunities and make well-informed decisions tailored to your unique needs and objectives.

Our advisors are adept at seamlessly integrating your real estate investments into your investment portfolio, helping to ensure they remain balanced and diversified. To explore our full-service offerings, see here.

Final Thoughts

REITs and direct property ownership offer unique advantages, making the right choice dependent on your financial goals, risk tolerance, and time horizon. At Agemy Financial Strategies, we help investors navigate the complexities of real estate investments for their financial portfolios. For over 30 years, our team of fiduciaries has guided clients in exploring opportunities in REITs and other investment vehicles to build resilient, diversified portfolios.

Contact us today to learn how we can help you achieve your financial aspirations and make informed decisions about real estate investments.

Disclaimer: This blog is intended for educational purposes only and should not be considered financial, tax, or legal advice. The information provided is general and may not apply to your financial situation. Investment decisions should always be based on your unique circumstances, goals, and risk tolerance. We recommend consulting a qualified financial advisor, such as our team at Agemy Financial Strategies, for personalized guidance tailored to your needs. Past performance does not indicate future results, and all investments carry inherent risks, including potential loss.

I’m High-Net-Worth. When Should I Start Estate Planning?

Estate Planning, NewsIf you have substantial wealth, the need for estate planning becomes even more significant due to the complexity of your financial situation. But when should you start estate planning if you fall into the HNWI category?

Estate planning is crucial for managing your wealth and protecting your assets so that they are distributed according to your wishes after your passing. In this blog, we will explore the importance of early estate planning for high-net-worth individuals and the key considerations to remember. Here’s what you need to know…

Estate planning is a solid guide on how you wish your assets to be distributed after passing. Whether your goal is to establish a lasting legacy or secure the financial well-being of your loved ones, starting estate planning early helps to ensure that your intentions are documented and legally binding.

A recent survey showed 73% of respondents had no estate plan. What’s even more surprising is that among respondents aged 75 and older, 72% were found to be without an estate plan. While it can be an uncomfortable topic to think about and discuss, postponing estate planning for too long can lead to potential complications and difficulties.

Let’s look deeper at some of the benefits of estate planning for high-net-worth individuals.

The Benefits of Establishing A Trust

As a HNWI, establishing a trust can be a powerful tool for achieving various financial goals and protecting your assets. Trusts offer flexibility, control, and numerous benefits, making them popular among individuals with substantial wealth.

There are various types of trusts, each designed to serve different purposes. Common types include revocable living trusts, irrevocable trusts, charitable trusts, and special needs trusts. Trusts can help shield your assets from creditors, lawsuits, and other threats. High-net-worth individuals can benefit from using irrevocable trusts for asset protection and estate tax planning.

Some trusts allow you to serve as the trustee, maintaining control while enjoying the benefits of asset protection and tax planning. The federal estate tax ranges from 18% to 40% and generally only applies to assets over $12.92 million in 2023 or $13.61 million in 2024. It’s important to consult with a financial advisor who can help you navigate the complexities of trusts to preserve, protect, and distribute your wealth according to your wishes.

Estate planning transcends the mere allocation of assets; it involves pivotal decisions regarding the inheritors of your wealth. For high-net-worth individuals, the meticulous selection of trustees and beneficiaries is paramount in crafting a robust estate plan.

Beneficiaries, slated to inherit your assets upon your passing, can encompass a range of individuals or entities, from beloved family members and friends to charitable organizations close to your heart.

Trustees, on the other hand, assume the pivotal role of overseeing and executing the distribution of assets in alignment with your meticulously outlined estate plan. Their role is instrumental in ensuring the proper management of your wealth.

By thoughtfully handpicking both beneficiaries and trustees, you lay the foundation for effectively realizing your estate plan’s objectives. Furthermore, this strategic selection significantly reduces the likelihood of conflicts and delays, assuring you that your assets will be disbursed precisely as you intended.

Minimizing Tax Liabilities

Reducing taxes on what you leave behind is a common estate-planning goal. Estate planning is about protecting your loved ones from potential IRS tax burdens. Essential to estate planning is transferring assets to heirs to create the smallest possible tax burden. Here are some key points to consider:

Life is constantly changing, and so should your estate plan. Changes in your family structure, financial situation, or legal regulations might necessitate updates to your plan to guarantee it remains aligned with your goals. A fiduciary advisor can help you with any changes that life may bring and help you adapt your plan accordingly.

Estate planning can be challenging — especially for those with a high net worth. You want to protect your family, assets, and business and gain peace of mind knowing you’re prepared and in control. Therefore, it’s essential to regularly review and update your estate plan to confirm it remains aligned with your goals and takes advantage of any new tax-saving opportunities.

An experienced fiduciary advisor can provide valuable advice and guidance regarding estate planning. At Agemy Financial Strategies, our team of skilled fiduciaries excels in assisting clients with creating robust estate plans. We are committed to providing our clients with the highest level of service, and we will work with you every step of the way to confirm that your estate plan needs are taken care of.

Last Thoughts

Estate planning is not just about wealth preservation; it’s about leaving a lasting legacy that reflects your values and priorities. Working with professionals to establish trust is essential to help guarantee your wishes are met, and your assets are protected.

At Agemy Financial Strategies, you can rest assured knowing that your financial affairs are in capable hands. If you want to learn more about how trusts can benefit your estate planning needs, schedule a complimentary strategy session with us today.

Disclaimer: This content is for educational purposes only and should not be considered financial or investment advice. Please consult with the fiduciary advisors at Agemy Financial Strategies before making any investment decisions.

Is Your Retirement at Risk? 5 Key Threats You Should Know

News, Retirement PlanningPlanning for retirement is a complex journey, with numerous factors influencing your financial security. While a single issue may not derail your plans, a combination of common yet often overlooked risks can significantly impact your retirement outlook.

A recent study found that nearly half of American households could run out of money in retirement if they cease working at 65. Understanding these hidden threats and taking proactive steps to mitigate them can mean the difference between a secure, fulfilling retirement and one filled with financial stress.

In this blog, we’ll uncover five major risks to your retirement that you won’t want to ignore. We will share how tips for strategic planning can help you navigate these challenges, allowing you to retire on your terms with more confidence and peace of mind.

1. Poor Asset Allocation: Finding the Right Balance

Improper asset allocation is one of the biggest risks to retirement savings. Many assume retirement demands a dramatic shift to conservative investments like bonds or cash equivalents. While reducing risk is wise, going too conservative can also hinder your savings growth, leaving you vulnerable to inflation.

A recent study was conducted to gain insight into investors’ alternative investments in workplace retirement savings plans. The study revealed solid interest in private assets despite a significant knowledge gap. Among those who expressed interest in private investments, most would take a measured approach with their retirement plan allocations (Schroders):

The ideal asset mix depends on individual goals, time horizon, and risk tolerance. Partnering with a fiduciary advisor can help you find the optimal balance and craft a plan that adapts to market conditions and personal changes. This approach can help keep your portfolio resilient and aligned with long-term goals.

2. Running Into Unexpected Expenses

When unexpected expenses arise, they can significantly affect your long-term financial health, particularly in retirement. These unplanned costs can quickly deplete your retirement savings, whether it’s a medical emergency, family support, or sudden home repairs. Nearly 6 in 10 (59%) U.S. adults feel unprepared for financial emergencies, indicating a widespread need for better financial planning.

This highlights the importance of a well-structured emergency fund. An emergency fund acts as a financial buffer, allowing you to manage surprise expenses without jeopardizing your retirement accounts. Building and maintaining this fund requires careful planning. With professional support, you can establish a cushion that shields your retirement savings from unplanned withdrawals, helping ensure your long-term financial security stays intact.

The “Sandwich Generation” refers to adults simultaneously supporting aging parents and children, a responsibility that can strain financial resources and delay retirement goals. Juggling these family obligations often means taking on additional healthcare, education, and living expenses, leaving less room for retirement savings.

In fact, 90% of Sandwich Generation adults report making a lifestyle change or financial decision because of caregiving responsibilities. Setting boundaries and establishing a structured financial plan is essential for those in this position. Prioritizing retirement savings while supporting family members can help safeguard long-term financial security.

A fiduciary advisor can provide valuable support by developing a balanced plan tailored to your situation. This personalized guidance can make a significant difference in helping maintain financial stability for both your loved ones and your future.

4. Long-Term Care Expenses: Protecting Against Rising Healthcare Costs

Long-term care remains a significant concern for retirees, with the U.S. Department of Health and Human Services estimating that 70% of people turning 65 will need some form of long-term care in their lifetime. Unfortunately, Medicare provides limited coverage for these services, and long-term care insurance can be costly. Planning for these potential expenses is crucial to helping safeguard your retirement savings.

The 2024 American Association for Long-Term Care Insurance (AALTCI) annual Price Index survey shows that the average annual premium for a $165,000 benefit policy without inflation protection is $950 for a single 55-year-old male and $1,500 for a single 55-year-old female. For a 55-year-old couple, the average combined annual premium reaches $2,080. These figures highlight the financial impact of securing long-term care coverage and the importance of including these costs in retirement planning.

A fiduciary advisor can help you navigate various funding options for long-term care, such as health savings accounts (HSAs), hybrid insurance policies, and setting aside dedicated assets within your retirement plan. With a fiduciary’s guidance, you’ll have access to strategies designed in your best interest, helping ensure these costs won’t drain your retirement funds and that you’re better prepared for the future.

5. Ignoring the Impact of Inflation

One of the most common yet underestimated threats to retirement savings is inflation. Over time, inflation erodes the purchasing power of your money, meaning that the same dollar buys less and less each year. For example, if inflation averages just 3% annually, in 20 years, you’ll need nearly twice as much money to maintain the same standard of living. For retirees, this steady cost increase can severely strain savings, particularly when living on a fixed income.

Ignoring inflation’s impact on retirement planning can lead to a financial shortfall when it matters most. Understanding the long-term impact and incorporating strategies to help protect your purchasing power is essential. Working alongside a fiduciary can help you build a portfolio that includes inflation-resistant assets aimed at outpacing inflation over time. By planning and adjusting your portfolio as needed, you can retain the ability to meet rising costs without compromising your financial security in retirement.

A secure retirement doesn’t happen by chance; it requires proactive planning and a clear understanding of the risks that lie ahead. Andrew Agemy, Owner and CEO of Agemy Financial Strategies, emphasizes the importance of a client-focused approach. “Our focus is on serving our clients with an educational process and listening with our hearts, not just our ears. This empowers our clients to make and realize their own solid financial decisions and allows them to remain in control.”

Here is how our team can help you navigate these challenges with confidence:

With Agemy Financial Strategies by your side, you can build a retirement plan designed to empower you and support a financially secure future.

Final Thoughts

Understanding and addressing these five critical retirement risks can make a significant difference in securing a comfortable, worry-free future. By taking proactive steps to help protect your savings and working with a knowledgeable fiduciary advisor, you can be better prepared to navigate unexpected challenges and achieve your retirement goals.

At Agemy Financial Strategies, we’re committed to helping you build a retirement plan that aligns with your vision and financial needs. With our personalized approach, you can plan confidently, knowing you’re well-prepared for the future.

Contact us today to start planning a retirement that fulfills your dreams and provides peace of mind.

Frequently Asked Questions

Q: How can I be sure my retirement plan is on track?

A: Regularly reviewing your retirement plan is essential to staying on course. At Agemy Financial Strategies, we offer ongoing support and periodic reviews to help your plan adapt to changes in market conditions, tax laws, and your personal financial situation. These reviews help you stay aligned with your long-term goals.

Q: What if I don’t know how much I’ll need for retirement?

A: Determining your retirement income needs is a common challenge. Our team at Agemy Financial Strategies helps you estimate these needs by examining your current expenses, desired lifestyle, and potential future costs like healthcare and long-term care. This process gives you a clearer picture of the savings required to maintain your lifestyle.

Q: How do you approach healthcare and long-term care costs?

A: Healthcare and long-term care expenses can be significant in retirement. We explore various options with you, including health savings accounts (HSAs), long-term care insurance, and retirement assets earmarked for medical needs. Planning for these costs in advance helps reduce their impact on your savings.

Q: How does Agemy Financial Strategies help manage inflation risks?

A: Inflation can erode the purchasing power of your savings over time. To combat this, we build inflation-resistant elements into your portfolio, such as stocks, bonds, and other investments that aim to outpace inflation. This approach helps protect your wealth and maintain your standard of living in retirement.

Q: What is the advantage of working with a fiduciary advisor?

A: As fiduciary advisors, we are legally and ethically committed to putting your best interests first. This means that all our recommendations are based solely on what’s best for you, with no conflicts of interest. Our goal is to provide transparent, objective guidance to help you achieve a secure and fulfilling retirement.

Disclaimer: The information provided in this blog is for educational purposes only and should not be taken as specific retirement or investment advice. Retirement and investment strategies should be tailored to each individual’s financial situation, goals, and risk tolerance. Before making any changes to your retirement investments, consult our qualified advisors to ensure these decisions align with your personal retirement objectives.

What You Need to Know About RMDS in 2025

News, Tax PlanningAs we approach the end of 2024, reviewing your retirement goals is a prime opportunity. One essential aspect to consider? Required Minimum Distributions (RMDs).

RMDs are a cornerstone of many retirement strategies, yet their complex rules and tax implications can make them challenging to navigate. Planning ahead can help you stay on track and optimize your retirement withdrawals.

With new RMD regulations set for 2025, understanding these changes can help you optimize your financial plans. In this blog, we’ll break down the fundamentals of RMDs, highlight the upcoming updates, and share practical tips to help you manage your distributions effectively.

Understanding Required Minimum Distributions (RMDs)

RMDs are mandatory withdrawals from certain retirement accounts once you reach a specific age. These withdrawals, which have grown tax-deferred over time, help retirement funds become taxable income. RMDs apply to the following accounts:

The annual amount you must withdraw is calculated based on your age, life expectancy, and account balance at the end of the previous year. Failing to take the required amount can result in significant tax penalties. Let’s take a look at key changes to look for in 2025.

As retirement planning continues to evolve, the latest updates to RMDs reflect efforts to provide more flexibility and tax advantages for retirees. The SECURE 2.0 Act introduced several new rules that impact how and when retirees must take distributions from certain accounts and adjust penalties. Below are the main changes for 2025 and beyond, designed to give retirees more control over their withdrawals and tax planning:

1. Increased RMD Starting Age: The age at which individuals must begin taking RMDs has been raised. In 2023, the age increased from 72 to 73, and it will further rise to 75 beginning in 2033.

2. Reduced Penalties for Missed RMDs: The penalty for failing to take an RMD has been reduced from 50% to 25% of the missed amount. If the missed RMD is corrected promptly, the penalty can decrease to 10%. Remember that the IRS has waived penalties for failing to take RMDs for certain inherited IRAs. For more information, see here.

3. Elimination of RMDs for Roth 401(k)s: Previously, Roth 401(k) accounts were subject to RMDs. Under the new rules, RMDs are no longer required for Roth 401(k)s, aligning them with Roth IRAs. It’s important to note that post-death minimum distribution rules, which also apply to Roth IRAs, still apply.

4. Annuities and RMDs: The SECURE 2.0 Act introduces provisions to make certain annuities more attractive within retirement plans. It allows certain types of annuity payments and clarifies qualifying longevity annuity contracts (QLACs) rules, including increasing the dollar limit to $200,000 and removing the 25% account balance cap.

5. RMDs for Surviving Spouses: Surviving spouses can now elect to be treated as the deceased account owner for RMD purposes, potentially delaying the start of RMDs if the surviving spouse is younger than the deceased. This election is irrevocable and requires notifying the account administrator.

6. Qualified Charitable Distributions (QCDs): The annual limit for QCDs, which count toward RMDs, is now indexed for inflation, starting at $105,000 in 2024. A one-time QCD of up to $50,000 is also allowed through certain charitable remainder trusts or gift annuities.

Why These Changes Matter

The recent adjustments to RMD rules are more than just technical updates—they bring valuable flexibility that can significantly benefit retirees. Here are some of the primary advantages of these changes:

1. Enhanced Growth Potential for Retirement Savings: Delaying RMDs means retirement accounts can stay invested and grow tax-deferred for longer. This change can be particularly beneficial for retirees who do not immediately need income from their retirement accounts, as it gives their investments more time to compound, potentially increasing their overall retirement nest egg.

2. More Control Over Roth 401(k) Withdrawals: With the removal of RMD requirements for Roth 401(k) accounts, retirees now have the same control as they do with Roth IRAs. This means they can choose when or if they want to withdraw from these accounts, providing a tax-free income source that can be preserved and used strategically within their broader retirement plan.

3. Reduced Penalties for Missed RMDs: The lower penalties for missed RMDs, combined with an opportunity for further reduction if corrected promptly, provide relief for retirees who may inadvertently miss their RMD deadline. This change reduces the financial impact of an honest mistake, making the RMD system more forgiving and manageable.

4. Options for Legacy and Charitable Planning: The increased flexibility around QCDs and the inflation-indexed annual limits make charitable giving a viable strategy for retirees looking to meet their RMD requirements while supporting causes they care about.

How to Calculate Your RMD in 2025

Calculating your Required Minimum Distribution (RMD) in 2025 is straightforward, with a few key steps. The IRS provides tables that determine your life expectancy factor based on your age, which you’ll use to calculate your RMD. Here’s a step-by-step guide:

Below is a portion of the IRS Uniform Lifetime Table to illustrate life expectancy factors by age:

Source: Internal Revenue Service (IRS)

Common Mistakes to Avoid

Navigating RMDs can be challenging; even small missteps can have significant financial consequences. Being mindful of some of the most frequent pitfalls can help you protect your retirement savings and maximize the benefits of these withdrawals. Here are three key mistakes to watch out for when planning your RMDs:

Working with a fiduciary can help ensure that your RMDs are managed to align with your financial goals and help you make the most of your retirement savings.

Working With an Advisor

New tax laws, potential shifts in Medicare premiums, income bracket adjustments, and evolving rules around charitable giving mean that your retirement income strategy may need some fine-tuning. Staying informed is essential for making the most of these adjustments and preparing your RMDs effectively.

At Agemy Financial Strategies, we provide personalized insights into your RMD responsibilities and tax-efficient strategies to help you manage these distributions. Our fiduciary advisors are dedicated to helping you meet your RMD obligations while optimizing your financial situation within IRS guidelines. We’ll work closely with you to assess your income needs in retirement and develop a plan that aligns with your financial goals and adapts to new regulations.

As part of our commitment to supporting your financial well-being, we offer tools like our free online RMD Calculator to help you estimate your required withdrawals. For more details on our services, please see our service offerings page here.

Final Thoughts

Navigating RMDs effectively requires staying informed about changing rules and understanding how these mandatory withdrawals impact your retirement income. Planning, keeping abreast of IRS updates, and consulting with financial advisors can help ensure that RMDs work in your favor while minimizing tax liabilities.

At Agemy Financial Strategies, our team is here to provide personalized guidance and support tailored to your financial needs and goals. Let us help ensure your tax obligations are appropriately managed throughout your retirement.

Preparing for 2025 doesn’t have to be overwhelming—let us help guide you toward a well-planned and prosperous new year. Contact us today to schedule your complimentary consultation.

Disclaimer: The information provided in this blog is for educational purposes only and is not intended as specific financial or investment advice. Each individual’s financial situation is unique, and any changes to your retirement income strategy or RMD planning should be discussed with a qualified financial advisor. We recommend consulting with our team at Agemy Financial Strategies to ensure your decisions align with your financial goals, risk tolerance, and the latest IRS regulations.

Financial Wellness: December Checkup

NewsGiven the volatile year we’ve encountered, checking in on your retirement plan may make a lot of sense this December.

As we approach the end of the year, it’s the perfect time for retirees to conduct a comprehensive financial checkup. December is not just a month for holiday cheer; it’s also an opportune moment to ensure your financial health is in excellent shape for the year ahead. In this article, we’ll explore the importance of a December financial checkup and provide valuable insights from the team here at Agemy Financial Strategies to help you navigate this crucial process.

Review Your Retirement Goals

Before diving into the nitty-gritty of your finances, take a step back and review your retirement goals. Are you on track to achieve what you set out to accomplish? Have there been any significant life changes that require adjustments to your financial plan? Whether it’s traveling more, supporting grandchildren, or simply enjoying a comfortable retirement, ensure your goals align with your current circumstances.

Sometimes, a few changes to your plan now can help you cross the finish line, even if market conditions are less than fully cooperative. Are you doing even better than anticipated? Maybe now is a good time to reduce your risk exposure to lock in that progress and protect against future market volatility.

Agemy Tip: Use our free online retirement goal calculators and other retirement resources here to evaluate your progress and make necessary adjustments.

Assess Your Investment Portfolio

A key component of any financial checkup is assessing your investment portfolio. Review your asset allocation to ensure it aligns with your risk tolerance and retirement timeline. December is an excellent time to rebalance your portfolio if necessary, as it can help you stay on track to meet your long-term financial objectives.

Agemy Tip: Our fiduciary advisors offer educated investment advice to help you analyze your investment portfolio’s performance and make informed decisions.

Tax Planning

December is your last chance to make tax-efficient moves for the year. Explore opportunities to minimize your tax liability by considering strategies such as tax-loss harvesting, maximizing contributions to tax-advantaged accounts, and reviewing potential deductions or credits.

Agemy Tip: These strategies can be complex; our team is well-versed in tax planning and can help you implement them.

Social Security and Medicare

Retirees must also consider Social Security and Medicare in their financial checkup. Are you eligible for Social Security benefits, and have you maximized your claiming strategy? Review your Medicare coverage to ensure it meets your healthcare needs. And don’t forget to cover Long-Term Care in your retirement plan.

Agemy Tip: If you need assistance navigating the complexities of Social Security, Medicare, or Long-Term Care planning, see here.

Emergency Fund and Insurance

As you head into retirement, having an adequate emergency fund and appropriate insurance coverage becomes paramount. Ensure you have enough cash reserves to cover unexpected expenses and review your insurance policies to make sure they adequately protect your assets and loved ones.

Agemy Tip: Explore our guide on building an emergency fund here and choosing the right insurance coverage here.

Estate Planning

Preparing for life after retirement involves much more than financial considerations. An estate plan ensures that your assets are protected and distributed according to your wishes, minimizing the burden on your loved ones and leaving a lasting legacy. Review your will, trusts, and beneficiary designations to ensure they align with your wishes. Consider consulting with Agemy’s estate planning professionals to make any necessary updates.

Agemy Tip: Agemy Financial Strategies offers valuable insights into estate planning; for more information on estate planning for the new year, see here.

Set Up an Annual Review

An annual financial review gives you a chance to evaluate your financial position. Many changes can affect your investments during the course of a year. It’s important to monitor your retirement and investment accounts regularly and make adjustments annually to stay on track.

You can schedule an appointment with a fiduciary advisor at any time of the year, but if it’s been a while since you last spoke with one (or have never spoken with one), you may be due for an end-of-year review. You should consider chatting with a fiduciary, especially if you have major life changes coming up in the new year — like a move to a new state, a home purchase, or even need changes to beneficiaries in your estate plan — so they can help you create a solid financial plan for those events.

Agemy Tip: We understand that annual reviews are an important part of anyone’s retirement plan. We strive to provide comprehensive advice and guidance so that you can make informed decisions about your investments, estate plans, and other financial strategies. Let us help you chart the path to a secure financial future with a complimentary strategy session here.

Conclusion

A December financial checkup is a vital step in maintaining your financial wellness. By reviewing your retirement goals, assessing your investment portfolio, planning for taxes, optimizing Social Security and Medicare, and addressing other financial aspects, you can set the stage for a financially secure and worry-free retirement. Agemy Financial Strategies’ resources and tools can be invaluable in this process, providing you with the guidance you need to make informed decisions and secure your financial future.

Checking in on your retirement plan doesn’t just entail making sure you are saving enough money. It also means helping ensure the savings you’ve worked so hard to accumulate will be there when you need it. Remember, it’s never too late to take control of your finances and make adjustments as needed. Start your December financial checkup today, and may you enjoy a prosperous and stress-free retirement in the coming year.

Disclaimer: This content is for educational purposes only and should not be considered financial or investment advice. Please consult with the fiduciary advisors at Agemy Financial Strategies before making any investment decisions.

Building Sustainable Income for a Long Retirement

News, Retirement Income PlanningLongevity is rewriting the retirement rulebook. With Americans reaching age 65 now expecting to live an additional 20 years on average, and nearly one in seven making it past 95, the need for a reliable, long-lasting income has never been more critical.

Building wealth and creating a steady income stream to support you through the decades ahead becomes essential as retirement approaches. In this blog, we will explore effective income strategies and provide valuable insights for those looking to create a financial foundation that endures the test of time. Here’s what you need to know.

Why Income-Generating Investments Are Crucial for a Long Retirement

As life expectancy rises, retirement planning must adapt to ensure financial resources endure. Traditional savings alone may fall short of keeping up with inflation and unexpected expenses, making it crucial to incorporate income-generating investments. Designed to provide regular cash flow rather than solely relying on appreciation, these investments play a vital role in maintaining financial stability.

By including income-generating assets, investors nearing retirement can sustain their lifestyle and cover ongoing expenses without eroding their principal savings. Here are some common investment vehicles that can help generate steady income:

Building a sustainable portfolio designed for consistent income can help you gain peace of mind, knowing you have the financial support to handle a longer retirement and the unexpected costs that may come with it. Working with an advisor can help you select the right investment based on your unique financial situation.

Building a Diversified Portfolio for Stability

Diversification is key to helping reduce risk while generating income from investments. By spreading investments across different asset classes—such as stocks, bonds, real estate, and alternative assets—investors can help protect themselves from market volatility and enhance the potential for steady income. Here’s a look at some advantages of a diversified portfolio:

Fixed-income securities, such as bonds and bond funds, are often the cornerstone of income-focused portfolios for retirees. They offer regular interest payments that can help provide a predictable income stream, particularly appealing to those nearing or in retirement. Fixed-income securities can vary significantly regarding risk and yield, so understanding their distinctions is essential.

Types of Fixed-Income Securities

Income from Real Estate: A Tangible Asset with Growth Potential

For investors interested in physical assets, real estate offers a compelling opportunity to generate income through rental payments and benefit from potential property appreciation. Many investors choose real estate for its income potential and its ability to diversify their portfolios. Here are some key benefits of real estate investments:

Working with a fiduciary advisor can help enhance your real estate investment strategy. They can offer tailored guidance to help manage risks and protect income, helping your investments align with your financial goals.

Dividends as a Source of Passive Income

Dividend stocks provide a way to earn income without selling investments. Companies in sectors like utilities, consumer goods, and healthcare often have stable dividend-paying stocks. Dividend-focused funds are another way to diversify income sources, as they pool stocks from multiple companies that pay dividends.

Evaluating Dividend-Paying Stocks

The Importance of Tax-Efficiency in Income Generation

Taxes can significantly impact the net income received from investments, so structuring your investment portfolio to help minimize tax liability becomes crucial. A well-planned, tax-efficient strategy can help enhance the longevity of your assets and allow you to keep more of your hard-earned income.

Working with a fiduciary can be invaluable when building a tax-efficient income strategy. They can help you structure an income-focused portfolio that helps minimize taxes while meeting your financial needs.

Managing Risk to Protect Income

Generating income from investments involves balancing income potential with effective risk management. For retirees and those nearing retirement, protecting your principal is crucial. Here are some strategies to help mitigate risk while prioritizing income generation:

Working with a fiduciary advisor can further support effective risk management, helping you tailor your portfolio to protect your income and financial security.

Working with an Advisor for Personalized Income Strategies

Crafting a personalized investment strategy to generate steady income can be complex, especially as retirement approaches. A knowledgeable advisor provides essential guidance, helping to create a tailored plan that meets income needs without compromising financial security. At Agemy Financial Strategies, our team of fiduciaries is here to guide you through the process, helping ensure that your money works efficiently to support a comfortable retirement.

Benefits of Professional Guidance

Our team is committed to providing the insights and resources you need to make confident decisions about your financial future. To learn more about our full range of personalized services, see here.

Creating a Sustainable Income Plan With Agemy

Building a reliable income stream from investments is essential to helping you achieve financial stability throughout retirement. The objective is to craft a diversified portfolio that not only generates steady income but also preserves capital for the long term. At Agemy Financial Strategies, we’re here to help you create an income-focused portfolio tailored to your unique financial goals and needs.

Contact us today to learn more about how our team can support your journey toward a sustainable and more secure retirement income plan.

Disclaimer: The information provided in this blog is for educational purposes only and should not be considered as specific investment advice. While we aim to provide valuable insights, every individual’s financial situation is unique, and changes to your investment portfolio or financial strategies should only be made after consulting with a qualified financial advisor. We encourage you to reach out to our team before making any investment decisions to ensure they align with your personal goals and risk tolerance.