Tax season is here, and staying ahead of Colorado’s tax landscape is crucial for individuals, families, and business owners alike. Surprisingly, Denver ranks #4 nationwide among the most procrastinating cities when filing taxes—a reminder that early planning can make a significant difference in avoiding last-minute stress and potential tax pitfalls.

Whether you’re a retiree, investor, or entrepreneur, understanding state tax laws can help you legally minimize liabilities and maximize financial opportunities. At Agemy Financial Strategies, our Denver team provides guidance tailored to Colorado’s unique tax structure.

In this blog, we’ll break down the essential elements of Colorado tax planning—including income tax rates, deductions, investment strategies, and estate considerations—to help you optimize your financial future.

Understanding Colorado Standard Deductions

Unlike many states, Colorado does not offer a standard deduction. Typically, standard deductions provide a simplified way to lower taxable income, while itemizing allows taxpayers to claim specific eligible expenses. Colorado has a flat income tax rate of 4.0%, meaning all taxpayers, regardless of income level, are taxed at the same rate. This rate was reduced from 4.40% in 2024 following a ballot measure to help lower tax burdens.

For higher-income earners, an additional factor comes into play. In 2023, Colorado began requiring an “add-back” for taxpayers with a federal adjusted gross income (AGI) of over $300,000. Any federal deductions that exceed state-imposed limits must be added back to taxable income, whether standard or itemized. The limits are as follows:

Sales Tax in Colorado

Colorado’s state sales tax rate is 2.90%, one of the lowest in the country. However, local governments and special districts can impose additional sales taxes, pushing the total rate significantly higher depending on the jurisdiction. Here are a couple of other items that are taxed and tax-exempt:

- Groceries: Exempt

- Clothing: Taxable

- Motor Vehicles: Taxable

- Prescription Drugs: Exempt

Local Sales Tax Variations:

- Denver: 8.81%

- Boulder: 8.85%

- Colorado Springs: 8.20%

- Fort Collins: 7.55%

Since Colorado follows a “home rule” system, which was introduced in 1902, certain cities and counties manage their sales tax collection, leading to different tax applications depending on where purchases are made.

Colorado Property Taxes

Colorado property taxes are relatively low compared to other states, averaging 0.45% of assessed home value—one of the lowest property tax rates in the U.S. For the property tax year 2025, the valuation is 27% of the actual value of the property. For property tax years commencing on or after January 1, 2026, the valuation is 25% of the actual value of the property.

Estate and Inheritance Taxes

The good news for Colorado residents is that the state does not impose an estate or inheritance tax. However, federal estate taxes may still apply to estates exceeding $13.99 million in 2025. While Colorado’s lack of a state estate tax can be beneficial, estate planning is still critical in helping protect your wealth and making sure your assets are distributed according to your wishes. Navigating the complexities of federal estate tax laws and gifting strategies can be overwhelming, but you don’t have to do it alone.

Whether you’re just starting or already in the middle of the process, working with a fiduciary advisor can help you develop a personalized estate plan that aligns with your financial goals, minimizes tax liabilities, and helps provide a smooth transition for your heirs.

Tax Strategies to Consider Before Filing

1. Maximize Retirement Contributions

Contributing to retirement accounts like 401(k)s, IRAs, and Health Savings Accounts (HSAs) can help lower your taxable income while saving for the future. In Colorado, contributions to Traditional IRAs and 401(k)s may be deductible at the federal level, which also impacts state taxes.

- 401(k) Contribution Limits (2024): $23,000 ($30,500 for those 50+)

- IRA Contribution Limits (2024):$7,000 ($8,000 for those 50+)

- HSA Contribution Limits (2024): $4,150 for individuals, $8,300 for families

2. Utilize Colorado’s Retirement Income Exemption

Taxpayers 55 to 64 (or those of any age receiving the income as a death benefit) may exclude the lesser of $20,000 or their taxable retirement income. Taxpayers 65 and older can subtract the lesser of $24,000 or their taxable retirement income.

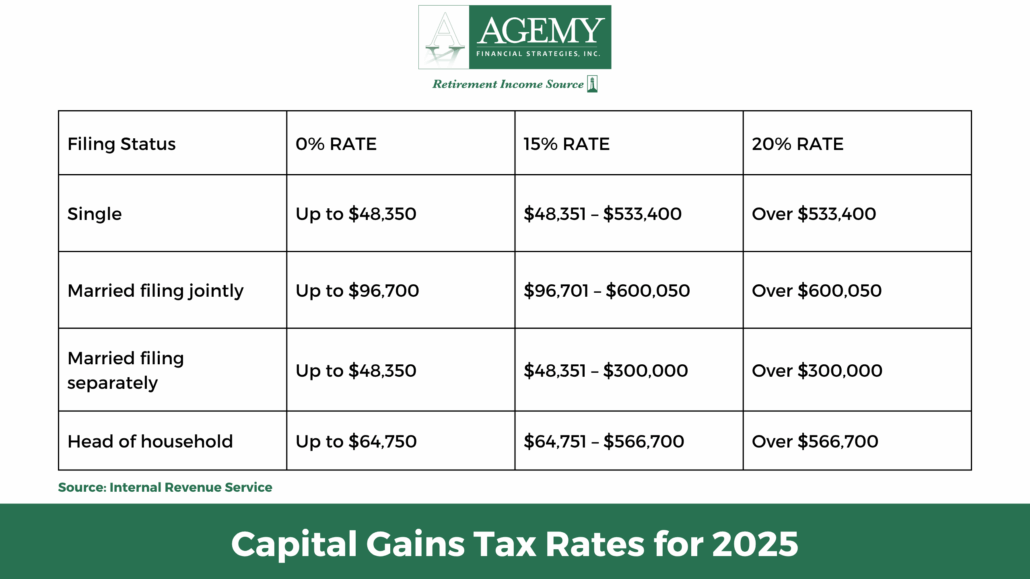

3. Consider Capital Gains Tax Benefits

Colorado allows a subtraction for qualifying capital gains if the asset is owned for at least five years before the sale and acquired on or after May 9, 1994. This could apply to certain business sales, real estate transactions, or stock holdings, making it an essential strategy for long-term investors.

4. Colorado Social Security

Colorado provides tax benefits for retirees by offering a pension and annuity subtraction, which includes Social Security income. While Social Security benefits are taxed at the federal level depending on total income, Colorado residents can exclude some benefits from state taxation.

How Colorado Taxes Social Security Benefits:

- Ages 55 to 64: Up to $20,000 can be excluded from taxable income.

- Ages 65 and older: Up to $24,000 of Social Security and other retirement income can be excluded from taxable income.

Not all Social Security benefits are included in federal taxable income, which affects how much can be subtracted from your Colorado return. The subtraction is only allowed for the portion of Social Security benefits included in federal taxable income, not the total benefits received.

- The Social Security benefits taxable portion appears on line 6b of your federal tax return, while line 6a shows the total benefits received.

- IRS Publication 915 provides a worksheet to determine how much of your Social Security benefits are taxable.

With Social Security frequently making headlines—whether due to potential reforms, future funding concerns, or changes in taxation—many retirees are left wondering how their benefits might be impacted. A fiduciary advisor can help you navigate these uncertainties, helping ensure you have a strategy in place to maximize your benefits while minimizing taxes.

5. Taxpayer Benefits

- Senior Property Tax Exemption: Homeowners 65 and older who have lived in their primary residence for at least 10 years may qualify for a property tax exemption on 50% of the first $200,000 of their home’s value.

- Disabled Veteran Exemptions: Veterans with a 100% disability rating in Colorado may receive a property tax exemption of 50% of the first $200,000 of the full value of their primary residence. This property tax deferral exists for eligible Veterans over the age of 65 and for active duty personnel.

Common Tax Pitfalls to Avoid

Navigating Colorado’s tax laws can be complex, and even small missteps can lead to missed savings or unexpected liabilities. Here are some common tax pitfalls to watch out for:

1. Missing Out on Available Tax Credits

Failing to take advantage of available tax credits can mean leaving money on the table. Here are some key credits that may help reduce your Colorado tax burden:

- Child Care Contribution Tax Credit: Donating to a qualifying childcare organization in Colorado can receive a tax credit equal to 50% of your total donation, with a maximum annual cap of $100,000.

- Renewable Energy Credits: Homeowners who invest in renewable energy—installing solar panels, electric vehicle chargers, or making energy-efficient home upgrades—may qualify for potentially valuable state and federal tax incentives.

- Property Tax, Rent, and Heat Rebate (PTC): Colorado offers rebates to seniors and qualifying individuals who pay property taxes, rent, or heating bills. This rebate, which must be submitted separately from Form DR 0104PTC, can be as much as $1,154 per year. Additionally, if you apply by October 15, 2025, you may receive an extra TABOR refund of up to $354 ($177 for single filers). For more details and application forms, see here.

2. Not Factoring in State and Local Tax Implications

Colorado’s tax structure differs from federal tax laws in important ways. Additionally, certain local taxes—such as property and sales tax rates—vary by county and municipality, affecting homeowners and business owners. Whether you’re managing investment income, planning for retirement, or running a business, understanding these state and local tax implications can help you optimize your tax strategy and avoid unexpected liabilities.

3. Misreporting Business Income

For self-employed individuals, freelancers, and business owners, accurately reporting income is essential to avoiding IRS penalties and staying compliant with federal and state tax regulations. Colorado follows federal guidelines for self-employment and business income.

However, failing to properly document 1099 earnings, deduct eligible business expenses, or account for self-employment taxes can result in audits or financial penalties. Additionally, you may need to navigate multi-state tax obligations if you operate across state lines. Keeping detailed records and working with a fiduciary advisor can help you meet all reporting requirements while maximizing deductions.

How Agemy Can Help with Tax Planning

At Agemy Financial Strategies, we understand that tax planning isn’t just about filing on time—it’s about creating a proactive tax strategy that helps minimize liabilities and maximize your financial potential. Here’s how our team can help:

- Retirement Tax Strategies: Our team helps you optimize 401(k), IRA, and RMD withdrawals to reduce taxes and maximize income.

- Investment Management: Utilize Colorado’s capital gains subtraction, tax-loss harvesting, and tax-efficient portfolio strategies.

- Estate Planning: Minimize estate tax exposure with strategic gifting, trusts, and inheritance planning.

- Tax Planning: Optimize business structures, deductions, and self-employment tax strategies.

Final Thoughts

Navigating Colorado’s tax laws requires strategic planning, whether you’re a retiree, business owner, or investor. Understanding the latest deductions, exemptions, and tax credits is key to helping optimize your tax strategy and maximizing savings. Without proper planning, taxes can erode your wealth over time.

Working with a fiduciary advisor can help you evaluate how tax laws may impact your financial future and develop strategies to minimize liabilities. At Agemy Financial Strategies, we assist retirees and high-net-worth individuals in implementing proactive tax planning strategies to help preserve their wealth and enhance their retirement security.

Contact our fiduciary team today to create a tax plan that aligns with your long-term financial goals.

Frequently Asked Questions (FAQs)

Can I deduct property taxes on my Colorado tax return?

Colorado does not have a separate deduction for property taxes. However, if you itemize deductions at the federal level, your property taxes may still be deductible. Agemy Financial Strategies can help you evaluate whether itemizing deductions is right for you and identify other tax-efficient strategies to minimize your tax burden.

How does Colorado tax capital gains?

Certain long-term capital gains (assets held for at least 5 years without interruption) may qualify for a subtraction on your Colorado return. However, standard capital gains tax rates apply at the federal level. Our team can help assess the tax implications and develop strategies to manage capital gains efficiently. By aligning your portfolio with tax-smart planning, we help you keep more of what you earn.

Do I need to file a state tax return in Colorado if I don’t work there full-time?

If you reside in Colorado for any portion of the year or earn income sourced from Colorado, you may be required to file a Colorado tax return, even if you work remotely. Tax rules for part-year residents and remote workers can be tricky. Agemy Financial Strategies can help you determine your filing obligations, avoid potential penalties, and develop a strategy that checks your tax liabilities.

How does Colorado tax retirement account withdrawals?

Withdrawals from 401(k)s, IRAs, and other retirement accounts are subject to a 4.0% flat income tax, but retirees can benefit from the pension and annuity subtraction to reduce taxable income. The amount you can subtract depends on your age and income sources. Federal taxes on retirement distributions still apply, and without proper planning, required minimum distributions (RMDs) could push you into a higher tax bracket. Agemy Financial Strategies assists in tax-efficient retirement planning, helping you structure withdrawals to reduce taxes and preserve your wealth.

Disclaimer: This content is for educational purposes only and should not be considered tax, legal, or investment advice. Tax laws and financial regulations change over time, and individual tax situations vary. Please consult the fiduciary advisors at Agemy Financial Strategies to assess how these tax strategies apply to your unique circumstances.

4. Plan for Estate and Gift Taxes to Preserve Generational Wealth

4. Plan for Estate and Gift Taxes to Preserve Generational Wealth What Are Estate, Gift, and Generation-Skipping Transfer Taxes?

What Are Estate, Gift, and Generation-Skipping Transfer Taxes?  State Estate Taxes: Another Layer to Consider

State Estate Taxes: Another Layer to Consider

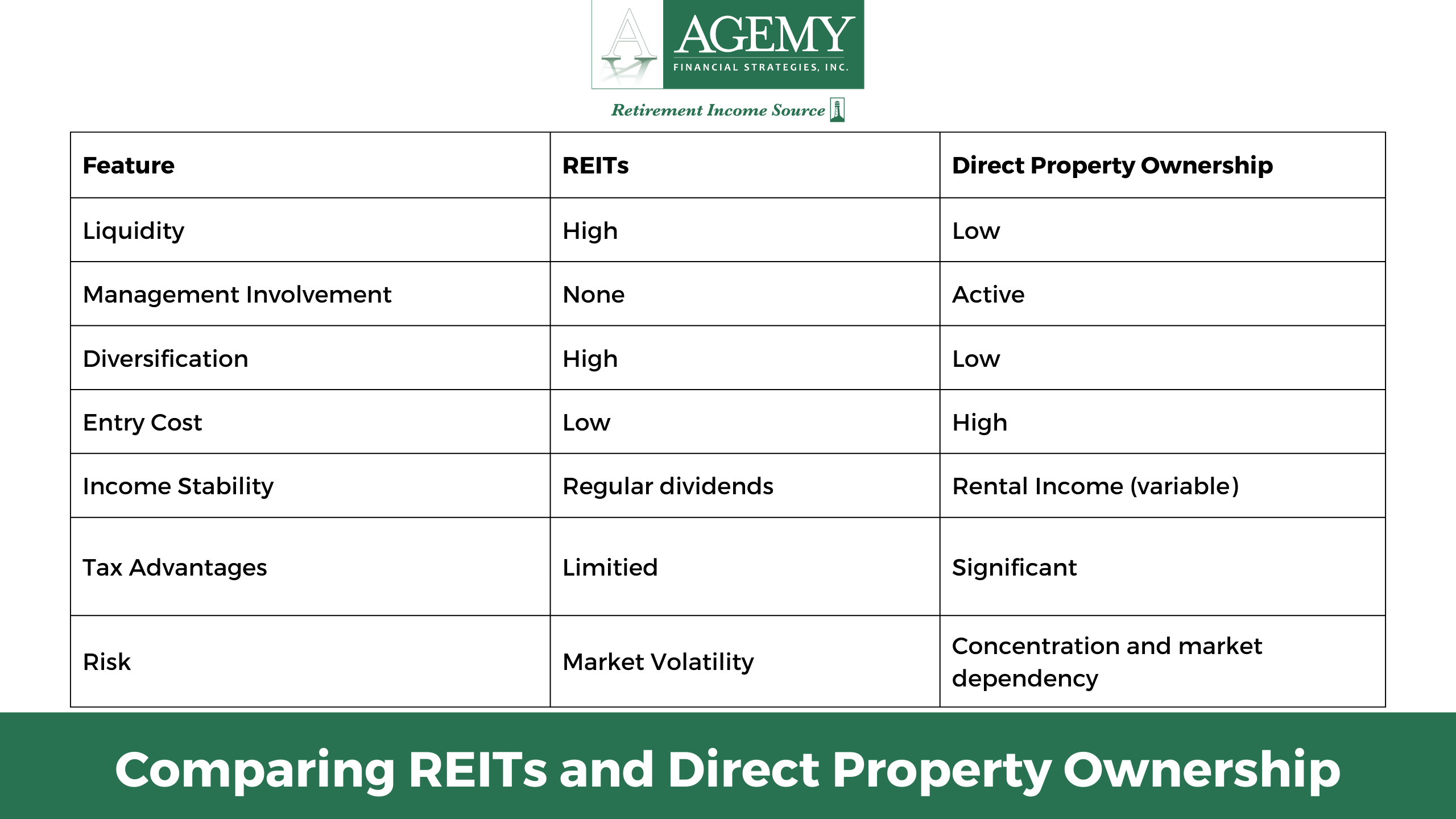

Cons of REITs

Cons of REITs

Cons of Direct Property Ownership

Cons of Direct Property Ownership

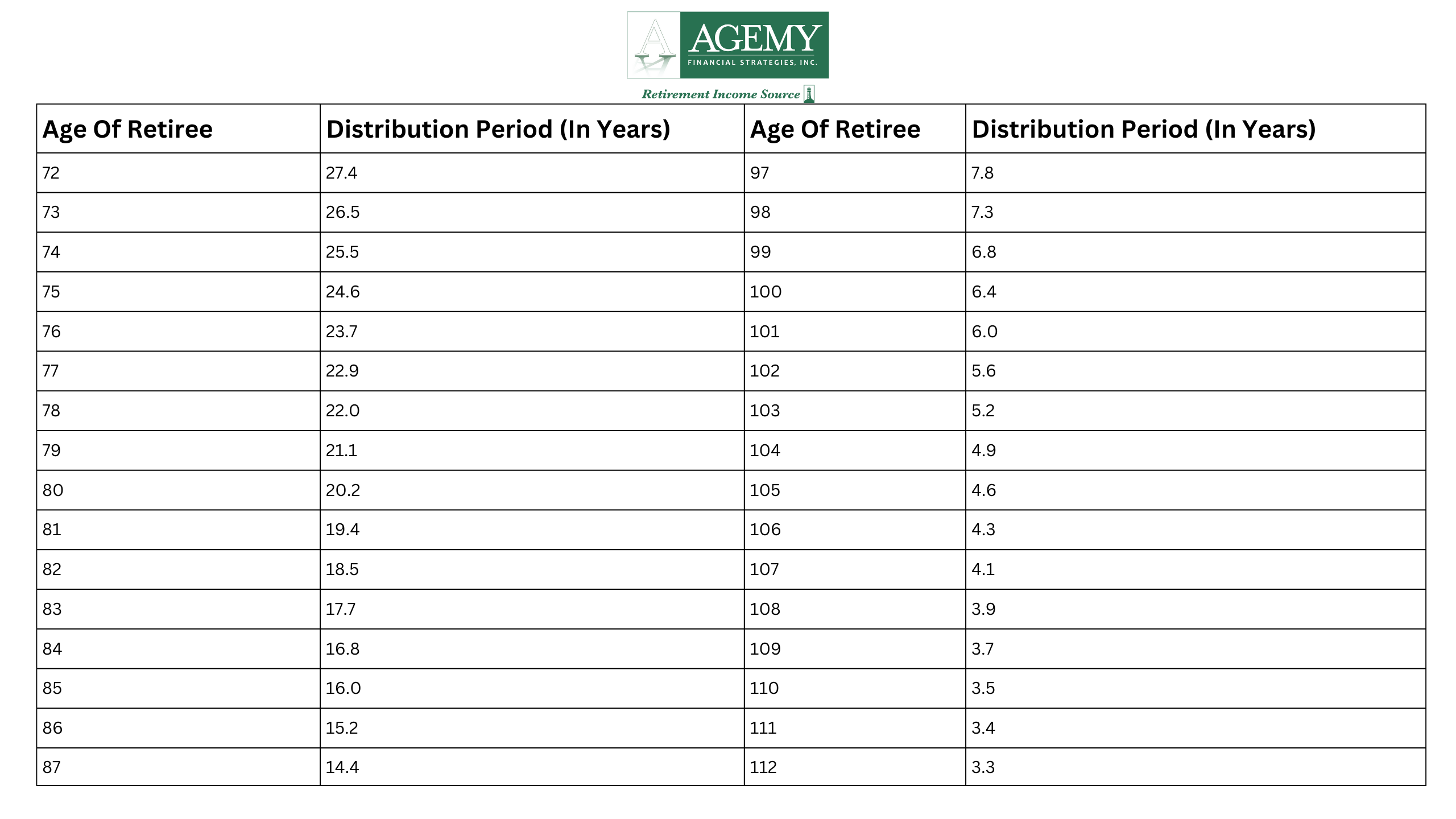

Key Changes to RMDs for 2025

Key Changes to RMDs for 2025

1. Smart Asset Location: Putting Investments in the Right Accounts

1. Smart Asset Location: Putting Investments in the Right Accounts

4. Maximizing Retirement Account Contributions

4. Maximizing Retirement Account Contributions The Importance of Proactive Tax Planning

The Importance of Proactive Tax Planning