When it comes to retirement planning, the vast majority of Americans have been taught a single, simple rule: Save as much as you can in your 401(k) or traditional IRA. We are told this is the path to security.

And for the accumulation phase of your life, that advice is sound. You received a tax deduction today in exchange for growing your nest egg. But there is a second half to that equation that is rarely discussed with the urgency it requires.

If you are like many of our clients at Agemy Financial Strategies, you may be sitting on a significant retirement account—$500,000, $1 million, or more—and you believe that money is entirely yours.

It’s not.

The IRS: Your ‘Silent Partner’

The reality of a traditional 401(k) or IRA is that you are not the sole owner. You have a silent partner: The IRS. When you eventually withdraw that money, your partner will demand their share. This is the definition of tax-deferred liability. You didn’t avoid the taxes; you simply pushed them into the future.

The problem is that the future is uncertain. When you deferred those taxes decades ago, neither you nor the IRS knew what tax rates would be when you retired. You are, in effect, exposed to an unknown tax liability on your entire balance.

If you have $1 million in a traditional IRA, that is not your usable balance. Depending on future tax rates and your income level, $200,000, $300,000, or even $400,000 of that balance may actually belong to your silent partner. This is why a simple accumulation strategy is no longer sufficient. You must shift your focus to a distribution strategy, and one of the most powerful tools in that arsenal is the Roth Conversion.

The Power of the Roth Conversion: Moving Toward Tax-Free Income

At Agemy Financial Strategies, we are passionate about the benefits of Roth accounts. A Roth conversion is a strategic transaction where you intentionally move funds from a tax-deferred account (like your traditional IRA) to a tax-free account (a Roth IRA).

When you make this move, two powerful things can happen:

- You pay the tax today. You settle your debt with your ‘silent partner’ at known, current tax rates.

- The money grows tax-free forever. The converted amount, plus all subsequent growth, can be withdrawn entirely tax-free in retirement (provided you meet the simple 5-year and 59.5 age rules).

The ultimate goal of a smart Roth move is not just to have money; it is to maximize your net, tax-free retirement income. Converting funds now can help you mitigate the risk of rising tax rates and secure a source of income that is immune to future IRS changes.

Identifying the ‘Retirement Income Valley’

The most critical window for execution is a period we call the Retirement Income Valley.

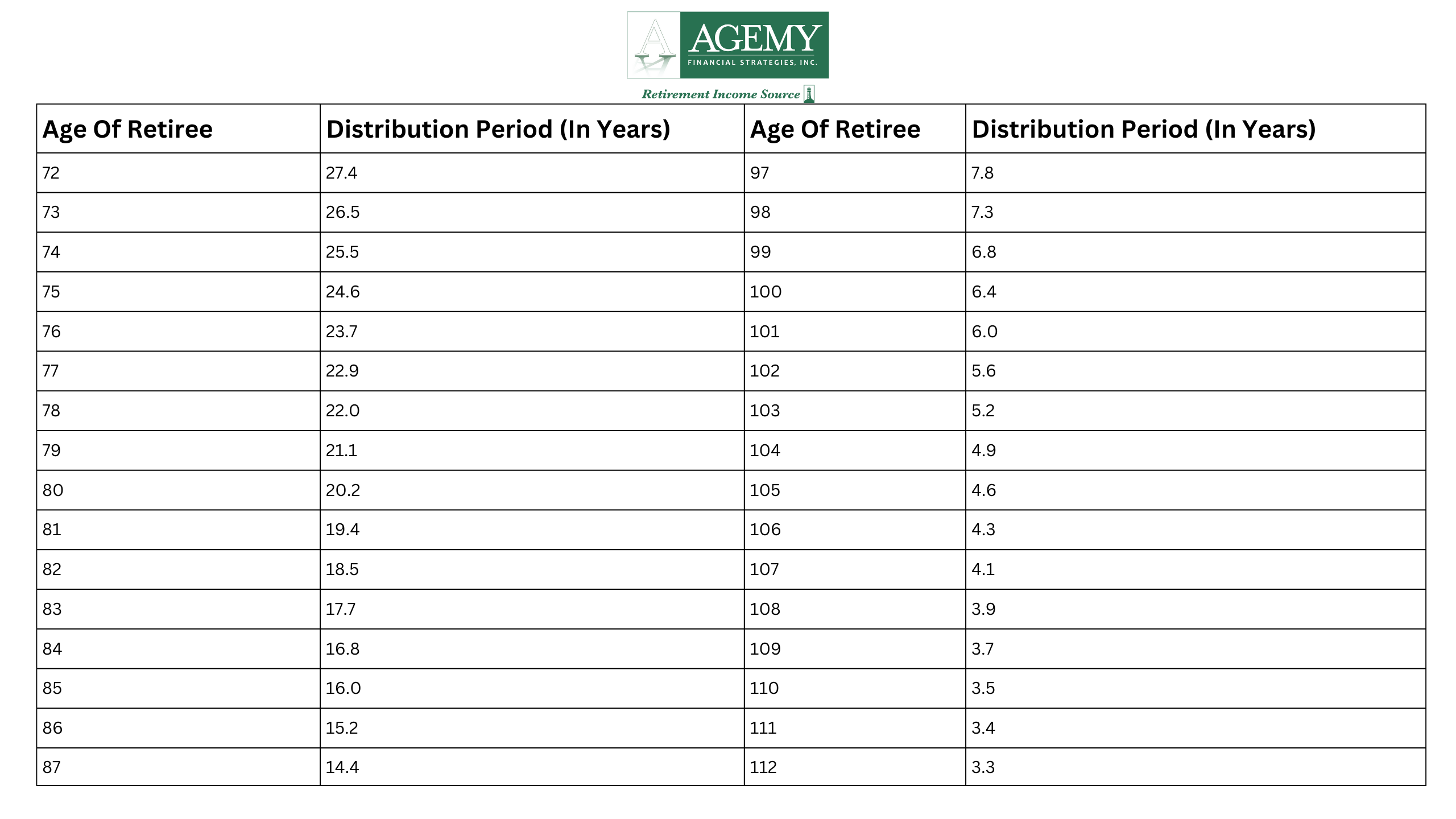

For many, this ‘valley’ is the ideal planning window. It typically occurs after you stop working (reducing your active income to zero) but before you are forced to start taking Required Minimum Distributions (RMDs) from your traditional accounts, which currently must begin at age 73 or 75. It may also include the window before you claim Social Security.

During these specific years, your taxable income may be lower than at any other point in your adult life. This places you in a very low tax bracket. This low-income environment creates a perfect, time-sensitive Opportunity Zone.

Imagine a valley between two mountains. On one side are your peak earning years. On the other side is the mountain of RMDs and Social Security taxation. The years in between are your low-income valley floor. It is in this valley that we can maximize Roth conversions at the lowest possible tax cost.

Instead of paying a 22% or 24% tax rate on distributions later in life, you may be able to convert those same dollars today while you are only in a 10% or 12% marginal tax bracket.

The Three Crucial Brackets You Must Manage

Successfully executing Smart Roth Moves requires managing more than just the standard income tax brackets (10%, 12%, 22%, etc.). We visualize this as having three interconnected levers that must be carefully adjusted. Failing to monitor all three simultaneously can turn a smart move into an expensive mistake.

A successful Roth strategy manages the interaction of these three “brackets”:

- Standard Federal Income Tax Brackets: This is the base layer. A smart strategy converts as much money as possible without unnecessarily pushing you into the next, higher marginal income tax bracket.

- Social Security Taxation: Up to 85% of your Social Security benefit can become taxable income. We must convert carefully so that the conversion income doesn’t exceed the thresholds that trigger full taxation of your benefits.

- IRMAA (Medicare Surcharges): If your converted income pushes your Modified Adjusted Gross Income (MAGI) too high, it triggers IRMAA—the Income-Related Monthly Adjustment Amount. This is a massive “hidden tax” that significantly increases your Medicare Part B and Part D premiums for an entire year. IRMAA thresholds are “cliff brackets,” meaning going $1 over the limit triggers the full fee.

How We Implement ‘Bracket Management’

This level of detailed planning is why working with a dedicated financial strategist can be vital. A simple online calculator cannot account for the way a Roth conversion simultaneously interacts with your ordinary income, your capital gains, your Social Security, and your Medicare premiums.

We help our clients implement true bracket management. The goal is to help maximize efficiency.

Suppose you have substantial “taxable room” left in your current 12% federal income tax bracket. If we convert that exact amount, we pay just 12% on those dollars and move them into a tax-free environment. However, if we fail to account for IRMAA, that same conversion might trigger a $4,000 Medicare surcharge. Suddenly, your effective tax rate on that conversion isn’t 12%; it has skyrocketed to over 30%.

Our planning tools forecast the impact across all three crucial brackets before we execute a single conversion. We aim to help you stay within your low-bracket valley without crashing into the cliffs.

When to Hold Off: The Role of Charitable Planning

While we are firm believers in the power of the Roth, a conversion is not appropriate for every situation. It is critical to analyze the whole financial picture.

For instance, a client with significant charitable intentions might be better served by a different strategy. If you plan to leave assets to a charity, converting to a Roth today means you are paying taxes on money that a tax-exempt entity could have received entirely tax-free later.

In that scenario, utilizing techniques like Qualified Charitable Distributions (QCDs) from a traditional IRA once you reach 70½ can directly satisfy RMD requirements without increasing your taxable income, effectively “bumping up against” the RMD mountain without climbing it. This is why a generalized approach often fails; it’s more beneficial to coordinate conversions with your other legacy goals.

Take the Next Step Toward Your Tax-Free Retirement

You have spent your entire life accumulating your nest egg. Now is the time to ensure you get to keep it. The existing tax rules, especially the low brackets during the ‘Retirement Income Valley,’ present an extraordinary, time-limited window to execute Smart Roth Moves.

At Agemy Financial Strategies, we’re experienced in building distribution plans that give you clarity and control over your taxes. Do not wait until your ‘silent partner’ makes the rules for you.

We invite you to schedule a consultation with Andrew and Daniel Agemy today. Let us help you navigate the valley, manage the crucial brackets, and build a lasting, tax-free income stream for your retirement.

Investment advisory services are offered through Agemy Wealth Advisors, LLC, a Registered Investment Advisor and fiduciary to its clients. Agemy Financial Strategies, Inc. is a franchisee of Retirement Income Source®, LLC. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC are associated entities. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC entities are not associated with Retirement Income Source®, LLC. This content is for informational and educational purposes only and should not be construed as individualized investment, tax, or legal advice. Any review, reliance or distribution by others or forwarding without the express permission of the sender is strictly prohibited. To the extent permitted by law, Agemy Financial Strategies, Inc and Agemy Wealth Advisors, LLC, and Retirement Income Source, LLC do not accept any liability arising from the use or retransmission of the information in this article.

4. Plan for Estate and Gift Taxes to Preserve Generational Wealth

4. Plan for Estate and Gift Taxes to Preserve Generational Wealth

Key Changes to RMDs for 2025

Key Changes to RMDs for 2025

2. SIMPLE IRAs & Catch-Up Contributions

2. SIMPLE IRAs & Catch-Up Contributions

6. New Retirement Savings “Lost and Found”

6. New Retirement Savings “Lost and Found”