Latest News

Everything thats going on at Enfold is collected here

Hey there! We are Enfold and we make really beautiful and amazing stuff.

This can be used to describe what you do, how you do it, & who you do it for.

Navigating RMDs in Retirement

NewsAs a retiree, you have worked hard to accumulate a significant nest egg over the course of your career. However, as you near retirement, you must navigate a series of financial requirements designed to make sure you’re using savings appropriately. That’s where Required Minimum Distributions come in.

When it comes to retirement plan distributions, IRS rules require everyone with a retirement account to take required minimum distributions (RMDs) once they reach a certain age. Since IRA distributions are usually taxable right away, the question of what to do with the money is often entwined with a desire to find tax-efficient strategies simultaneously.

Here are some strategies to help you navigate RMDs as you transition to retirement.

What is an RMD?

A required minimum distribution (RMD) is the amount of money that must be withdrawn from employer-sponsored retirement plans by owners, and qualified retirement plan participants of retirement age.

In 2023, the age at which you must begin taking RMDs changed to 73 years. Account holders must therefore start withdrawing from a retirement account by April 1, following the year they reach age 73. The account holder must withdraw the RMD amount each subsequent year based on the current RMD calculation.

Another significant change from Secure 2.0: Starting in 2024, holders of designated Roth 401(k) accounts will no longer be required to take RMDs from them (during their lifetime). This rule is already true for Roth IRAs.

Which Retirement Accounts Require RMDs?

Most—but not all—retirement accounts have RMDs, from individual retirement accounts (IRAs) to employer-sponsored plans. Those that do include:

403(b) plans

RMD rules do not apply to Roth IRAs, which are funded with after-tax dollars. However, there’s one exception: Upon the account owner’s death, beneficiaries may be required to take an RMD from that account every year or face a penalty.

Understand the RMD Calculation

To determine your RMD, you need to calculate the amount you must withdraw based on your account balances as of December 31 of the previous year. The IRS has established useful resources online that specify life expectancy based on age and other factors, such as whether you are married and your spouse’s age. It’s important to note that your RMD amount will change from year to year based on changes in your account balance. Therefore, it’s essential to recalculate your RMD amount each year to ensure that you are withdrawing the correct amount.

Here is the RMD table for 2023, based on the Uniform Lifetime Table of the IRS, which is the most widely used table. The IRS has other tables for account holders and beneficiaries of retirement funds whose spouses are much younger.

Retiree Age Distribution Chart

Retiree Age Distribution Chart

Source: Internal Revenue Service (IRS)

Consider Charitable Giving

The IRS provides assistance to those who prioritize charitable donations through qualified charitable distributions. This method allows for a direct transfer of up to $100,000 per year from an IRA to a qualified charity, which counts towards the RMD. While this option is available for both spouses, the $100,000 distribution allowance is not shared in joint returns. Therefore, if one spouse donates $75,000, the other can still donate up to the full $100,000.

Andrew A. Agemy, Founder and CEO of Agemy Financial Strategies, highlights that “Utilizing qualified charitable distributions can be an effective strategy for managing RMDs while also reducing taxable income.“

This approach can provide significant benefits for those looking to optimize their retirement savings and support charitable causes.

Take Advantage of Roth Conversions

A viable option to explore is the conversion of a regular IRA to a Roth IRA. Traditional IRAs are funded with pre-tax dollars, while after-tax dollars fund Roth IRAs. Roth IRA payouts and capital growth are tax-free and can be inherited without inheritance tax. Additionally, Roth IRAs are not subject to RMDs, making them a smart choice for retirees.

According to Agemy, “Roth conversions are key when it comes to reducing taxes over the long term.” The conversion process will require payment of income taxes on the IRA holdings, but it provides flexibility. The conversion doesn’t have to include all assets in the regular IRA account, which maximizes tax efficiency. This is particularly useful if your tax rate is projected to increase in the future.

For those with substantial traditional IRA or 401(k) balances, converting some of those funds to a Roth IRA may be advantageous. This conversion offers the opportunity to avoid future RMDs and improve tax efficiency.

Can You Delay RMDs?

There are a few instances where you may be able to delay RMDs. These include:

Penalties are a consideration if you forget to take out your RMD. With the passing of Secure ACT 2.0 the missed RMD penalty dropped to 25% in 2023 and is dropped to 10% if fixed during the correction window.

Consult with a Financial Advisor

Retirees with substantial retirement account balances may find navigating RMDs to be a complex process. However, working with a Fiduciary Advisor can simplify the process by developing a comprehensive retirement income plan that includes RMDs, tax planning, and other critical factors.

The fiduciary advisors at Agemy Financial Strategies will work alongside you to strategize the best way to minimize taxes in retirement. We work tirelessly to provide a reliable retirement income stream that can withstand volatile market conditions, allowing you to enjoy the best possible retirement lifestyle.

If you’re interested in learning more about navigating RMDs and planning for a secure retirement, contact us here today.

Trust Solutions for High-Net-Worth Estates

NewsApril 26, 2024

Estate planning is essential for high-net-worth individuals, who often have significant assets to pass on to their families. One of the most effective ways to protect HNW estates is through the use of different types of trusts. Here’s what you need to know.

Busy schedules and high-stress environments often lead many wealthy individuals to delay the critical process of including trusts in their estate plans. According to a recent survey from Caring.com, over half of the wealthiest Americans have implemented no form of estate plan—no will, trust or advance directive. A staggering 54% attribute their inaction to procrastination.

With the right knowledge, trusts offer a powerful solution for preserving your legacy and helping secure your assets. At Agemy Financial Strategies, we believe trusts are one of the most undervalued financial tools for managing your hard-earned wealth.

Join us as we explore how trusts in your overall estate plan can help you protect your family’s future and achieve your financial goals.

First is Understanding The Importance of Estate Planning

Estate planning is a crucial aspect of retirement planning as it allows retirees to set a blueprint for the distribution of their assets after their passing. Without an estate plan, retirees risk leaving their loved ones without clear instructions on handling their estate. Poor planning can lead to confusion, disputes, and potentially costly legal battles.

35% of American adults say they have personally experienced family conflict or know someone who has due to not having an estate plan in place. Creating a comprehensive plan helps ensure your assets are distributed according to your wishes, minimizing the likelihood of family conflict.

Before consulting with a fiduciary advisor to start your estate plan, take some time to reflect on your posthumous wishes, as well as some critical questions and scenarios, including:

Although it may be challenging to initiate, discussing your intentions with your loved ones in advance allows you to convey your wishes clearly and allows everyone to ask questions or express their concerns.

Trusts serve as effective tools for high-net-worth individuals (HNWI) by protecting assets, minimizing taxes for beneficiaries, and helping provide precise allocation of wealth. Essentially, trusts are legal entities that hold assets for designated beneficiaries. Trusts provide several benefits for high-net-worth individuals:

In addition to these primary advantages, trusts can be tailored to achieve specific goals, such as charitable giving and preserving wealth across generations. Now that we’ve covered the basics of trusts let’s explore trusts that may benefit high-net-worth individuals.

Types of Trusts Available

Each type of trust presents unique advantages and considerations, and the suitability of a specific trust structure depends on individual circumstances and goals. Trusts are powerful tools for high-net-worth retirees who aim to preserve their wealth and legacy for future generations. Here’s a look at several common types of trusts.

1. Living Trust

A Living Trust is created during your lifetime and it designates a trustee who will manage assets for your Beneficiary or Beneficiaries after your passing.

2. Intentionally Defective Grantor Trusts (IDGTs)

These irrevocable trusts are advantageous for estate tax reduction and wealth transfer. IDGTs allow assets to be excluded from the grantor’s estate for tax purposes while the grantor pays income tax on trust earnings.

3. Revocable Trusts & Irrevocable Trusts

4. Charitable Trusts

Charitable trusts are designed to allow individuals to donate assets to a charitable organization while still retaining some benefits from those assets. With this type of trust, the grantor transfers assets to the trust, making payments to the grantor based on an agreed-upon formula. After the grantor passes away, the remaining assets in the trust are distributed to the designated charity.

Charitable trusts offer several benefits:

These types of trusts can be tailored to meet individual goals and structured in various ways to suit different situations. It is important to work with an experienced fiduciary advisor to determine if a charitable trust is appropriate for your estate planning needs.

5. Dynasty Trusts

Dynasty trusts are designed to perpetuate wealth management across multiple generations while minimizing tax liabilities. By keeping assets within the trust, dynasty trusts can protect wealth from estate taxes and creditors, ensuring a lasting legacy for future descendants. Consulting with a knowledgeable fiduciary advisor is essential to determine the most appropriate trust strategy for maximizing estate protection and achieving long-term financial objectives.

The above list serves as just a few trusts available for HNWIs. Others to discuss with your fiduciary advisor include:

Why Trusts Are Important

Setting up a trust is essential for asset protection and ensuring tax-efficient wealth transfer. Trusts play a crucial role in reducing estate tax exposure, enabling more assets to be passed to beneficiaries in a tax-efficient manner. By minimizing estate taxes, trusts offer significant benefits to estate planning.

While estate tax rates are currently progressive, it’s crucial to understand the tax rates applicable to your situation. Many states, including Connecticut, impose estate taxes with lower asset thresholds than the federal government. The table below outlines each state’s exclusion amount.

Living in a state with an estate tax can be advantageous, as your estate tax bill is generally subtracted from your taxable estate before calculating what you owe the IRS. Consulting with an experienced fiduciary advisor is key to selecting the most suitable trust to meet your unique needs and goals.

Working With a Fiduciary Advisor

Estate planning that includes the right types of trusts can be challenging, especially for those with a high net worth. You want to protect your family, assets, and business while gaining peace of mind knowing you’re prepared and in control. That’s why when estate planning for HNW estates, it’s essential to work with an adviser highly experienced in this area of retirement planning.

Working with fiduciaries is essential when establishing a trust. They can help ensure that your wishes are met and your assets are protected. An experienced fiduciary advisor can help you navigate complex legal and financial issues and determine the best type of trust for your specific needs and goals. They can also help confirm that your trust is structured to provide the maximum benefit to your beneficiaries.

Agemy Financial Strategies has a team of skilled fiduciary advisors who excel at helping clients create robust and meaningful trusts. We are committed to providing our clients with the highest level of service and will work with you every step to help ensure that your trust meets your unique needs and goals.

Final Thoughts

For high-net-worth retirees, trusts are pivotal in preserving assets and facilitating tax-efficient wealth distribution. Partnering with Agemy Financial Strategies can help bring you peace of mind regarding effective estate planning. Our experienced team is dedicated to helping you secure your legacy and confidently achieve your financial goals.

Schedule a complimentary strategy session with us to learn more about leveraging trusts for your estate planning needs.

Generating Passive Income in Retirement

NewsThe key to being able to enjoy freedom and comfort in retirement is to have a strategy to develop passive streams of income – and then implement this strategy intelligently.

Retirement should be a time of relaxation and enjoyment, free from financial worry. Many retirees, however, find themselves struggling to maintain their desired lifestyle on a fixed income.

Preparing for retirement has become more demanding, given the increased risks and rising costs associated with healthcare, housing, and long-term care. As a result, retirees may need to seek other sources of income to supplement their retirement savings.

One solution that retirees turn to is generating passive income. Passive income can be an excellent way to earn money without working actively, providing financial security and stability during retirement. In this blog post, we will explore a variety of strategies to generate passive income in retirement, helping you achieve financial freedom and maintain a comfortable lifestyle. Here’s what you need to know.

What is Passive Income?

Generating passive income is a way to earn a steady stream of money with minimal daily effort. However, it’s important to note that earning passive income is not a “get-rich-quick” scheme, as it requires some initial effort and investment. For instance, some passive income ideas such as creating a blog or an app may require significant time and financial investment at the outset.

Nonetheless, if you take the time to establish a passive income stream, it could eventually generate income while you sleep. Some key benefits of passive income include:

Buying Real Estate

Owning rental properties can be an excellent way to generate passive income during retirement. As a retiree, you can purchase a rental property and rent it out to tenants, providing you with a steady stream of income. However, before diving into real estate investment, it’s crucial to do your due diligence.

Firstly, it’s recommended to pay off your home before purchasing an investment property with cash. Taking on debt to buy a rental property can be risky and may not be a wise financial decision during retirement. Additionally, owning a rental property requires effort and maintenance to ensure it remains a source of income.

When purchasing a rental property, it’s essential to decide how you want to manage it. If you plan to manage it yourself, consider buying a property that is conveniently located for you to visit regularly. As an alternative, you can hire a property management company to handle the day-to-day operations, but this will come at an additional cost.

On the plus side, there are tax benefits to take advantage of. As a real estate investor that holds income-producing rental property, you can deduct depreciation as an expense on your taxes. That means you’ll lower your taxable income and possibly reduce your tax liability. If the idea of being a part-time landlord doesn’t interest you, there is another option to invest in real estate that offers passive income opportunities. Real estate investment trusts (REITs).

Invest in Real Estate Investment trusts

Real estate investment trusts (REITs) allow investors to pool their money with other investors to purchase properties. In essence, it’s a mutual fund that invests in real estate instead of stocks.

REITs can be a good investment option for seasoned investors. However, if you’re just starting, it’s advisable to focus on building your wealth before investing in REITs. Although there are some reliable REITs in the market, there are still many that use debt to purchase properties, which increases the risk for investors.

It’s crucial to seek advice from an investment professional, such as a Fiduciary Advisor, before investing in REITs. They can help you assess the risks and determine whether investing in REITs aligns with your financial goals and overall investment strategy. By working with a financial professional, you can make informed decisions and potentially generate passive income through real estate investing.

Take Advantage of High-Yield Savings Accounts

Aside from rental properties and REITs, there are other ways retirees can generate passive income. One such way is through high-yield savings accounts, which can help reach short-term financial goals and provide a source of passive income.

Many online banks and financial institutions offer savings accounts and money market accounts with annual percentage yields (APYs) ranging from 3-4%. This yield is significantly higher than the national average for savings accounts, which is only 0.37% as of March 2023 (according to the Federal Deposit Insurance Corporation (FDIC).

Online banks can offer higher rates due to their lower overhead costs compared to traditional brick-and-mortar banks. For instance, if you have a fully funded emergency fund of $25,000 in a savings account or money market account with a 4% APY, you can earn $1,000 in interest growth over the next year without doing anything. The more you save, the more interest you can earn.

It’s crucial to compare rates and terms of different savings accounts and money market accounts and choose one that aligns with your financial goals and needs. While high-yield savings accounts may not provide as much passive income as rental properties or REITs, they offer a lower-risk and hassle-free option for retirees looking to generate additional income.

Invest in Dividend Stocks

Dividend-paying stocks are another excellent way to generate passive income. Many companies pay dividends to their shareholders, which can provide you with a regular source of income. Dividends are paid per share of stock, so owning more shares can result in higher payouts.

However, selecting the right stocks can be tricky, and that’s where an experienced Fiduciary Advisor can provide valuable guidance. They can help you find exchange-traded funds (ETFs) and mutual funds that align with your investment objectives. ETFs are a great option because they’re easy to understand, liquid, and typically less expensive than mutual funds.

By working with a Fiduciary Advisor, you can choose the right dividend-yielding stocks to help generate passive income with minimal effort.

Remember, passive income isn’t “free money” nor is it “risk-free”. Every move you make with your money has risk involved, so once again, always consult with your financial advisor before making passive income moves.

Final Thoughts

Generating passive income in retirement can help you maintain your desired lifestyle and achieve financial freedom. By diversifying your investments and exploring various income-generating opportunities, you can help create multiple streams of passive income that will support you throughout your retirement years.

At Agemy Financial Strategies, our Fiduciary Advisors can work with you to create a tailored game plan that aligns with your financial goals. Having a Fiduciary by your side can help ensure that your needs are met on your road to retirement and beyond. By working with us, you can make informed decisions and help create a secure financial future for you and your family.

If you’re ready to start the conversation, get in touch with us here today to schedule your complimentary consultation.

Your Last-Minute Tax Checklist

NewsApril 11, 2024

Taxpayers across the United States anticipate a looming deadline: Tax Day. Falling on Monday, April 15th, this date evokes a sense of urgency and, for many, a hint of stress as they rush to gather essential documents, receipts, and forms.

An estimated 28% of Americans are unaware of this year’s tax filing deadline. Agemy Financial Strategies is here to provide the necessary guidance and assistance, offering careful planning to help you seize the opportunity to optimize your financial situation. Here’s what you need to know.

The key to a smooth Tax Day experience lies in careful preparation. Here’s a checklist of essential items you’ll need to gather before the April 15th deadline:

Compiling these documents and information ahead of time can help you streamline the tax filing process and minimize the risk of errors or oversights.

Understand Changes to Tax Brackets

Understanding tax bracket changes for the 2023 tax year is crucial for taxpayers to navigate their financial planning effectively. Tax brackets are revised periodically to adjust for inflation and changes in the tax code. While the tax rates have remained unchanged, there has been a notable 5.4% increase in the federal income tax brackets.

Staying informed about these changes can help empower individuals and businesses to make informed decisions regarding their income, investments, and overall financial strategy. Taking advantage of available tax deductions and credits can also help minimize your tax liability.

Maximize Available Deductions and Credits

Maximizing deductions and credits is a savvy strategy for taxpayers looking to lower their taxable income and reduce their tax liability. Deductions such as contributions to retirement accounts, including traditional IRAs or 401(k)s, help individuals save for the future and offer immediate tax benefits by lowering taxable income.

Charitable giving can also be a tax-smart strategy, particularly for retirees with substantial assets. It can help lower withdrawal taxes from your tax-deferred retirement accounts, including Required Minimum Distributions (RMDs). Additionally, it can help reduce your taxable estate and minimize the tax liability for your account beneficiaries. However, it’s important to note that generally, you should be over the age of 59½ to avoid early withdrawal penalties.

To help maximize these tax benefits, consider seeking advice from a financial advisor. They can provide insights into optimizing your tax advantages. Strategies such as grouping charitable donations into a single year or establishing charitable trusts are effective ways to enhance the tax benefits of charitable giving. By strategically maximizing deductions and credits, taxpayers can help optimize their tax situation and maximize their financial resources.

Manage Your Tax Deadline Effectively

The IRS allows retirees who cannot file their tax returns by the April 15th deadline to request a six-month extension. This extension can be helpful in situations where a taxpayer needs a tax form or additional time to prepare their return. Taxpayers can request an extension for free via IRS Free File, regardless of their income.

It’s essential to note that while an extension will give retirees additional time to file their returns, it doesn’t extend the deadline to pay their federal taxes. Your tax bill has to be paid by the April 15th deadline. In cases where a taxpayer is missing a tax form, they can estimate their tax bill by using tax software and inputting estimates for any missing forms.

It’s also worth noting that requesting a federal extension doesn’t automatically extend the deadline for state tax returns. Those who need additional time to file their state tax returns must request a separate extension.

There is no penalty for filing an extension. However, not paying on time or enough, or failing to file altogether, may cost you.

After you file the extension, you’ll have until October 15th to gather your documents and finish your filing. When you complete your return, you should include the amount you’ve already paid in the payments section of your Form 1040.

Minimize Your Tax Burden With a Financial Advisor

While gathering the necessary paperwork is essential, it’s only one piece of the puzzle. Partnering with a skilled financial advisor can take your tax planning to the next level by helping you strategically manage your finances throughout the year to minimize your tax burden.

At Agemy Financial Strategies, we can help you explore options to help ensure you take advantage of tax strategies that can minimize your tax liability while boosting your savings. Here’s how our advisors can assist you in creating a tax plan strategy:

Get an Extension

Not ready to file on Monday? Taxpayers who can’t file by the deadline of April 15, 2024, should request an extension before that deadline. Remember, however, that an extension to file is not an extension to pay taxes. If they owe taxes, they should pay them before the due date to avoid potential penalties and interest on the amount owed. Apply for your extension here.

Last Thoughts

Tax Day doesn’t have to be a dreaded deadline. By gathering the necessary documents and partnering with a financial advisor to develop a tax plan strategy, you can confidently navigate the tax filing process and even potentially minimize your tax burden.

Agemy Financial Strategies is dedicated to providing knowledgeable guidance on tax planning strategies to help you minimize future tax burdens. Our team is here to help you every step of the way, helping ensure that your retirement years are filled with immense fulfillment.

With our guidance, you can embrace the opportunity to optimize your financial situation and secure a brighter financial future. Contact us today to get started and schedule your complimentary strategy session here.

Knowledge is Power this Financial Literacy Month

NewsUnderstanding how to manage money effectively is fundamental on your road to retirement.

Retirement should be a time of joy spent with loved ones and enjoying the fruits of one’s labor. However, retirees and soon-to-be retirees often feel vulnerable amidst rising inflation and unpredictable markets. Yet, with careful planning, you can protect your retirement from market turbulence and financial worries.

To empower you to retire with peace of mind, we’ve gathered retirement planning strategies for new retirees and those looking to fine-tune their plans. These insights will help you approach retirement with optimism. Here’s what you need to know.

When it comes to retirement planning, defining your goals is a crucial first step. Retirement can mean different things to different people, so it’s necessary to think about what you want your retirement to look like.

For some, retirement may involve traveling to new destinations, exploring hobbies and interests, or spending quality time with loved ones. Others may opt to continue working in some capacity during their retirement, while others may have different plans altogether. Whatever your aspirations, clearly understanding your retirement goals is essential.

Once you’ve identified your retirement objectives, you can start crafting a plan to achieve them. This plan should take into consideration various factors, including:

Planning for retirement is an essential component of financial literacy. When you define your retirement objectives and chart a course of action, you make significant strides toward accomplishing a successful retirement.

Enhance Your Investment Approach

The primary objective of investing is to achieve high returns, but with higher returns comes a higher level of risk. In order to help optimize your returns and minimize potential risks, it’s crucial to diversify your investment portfolio. Your investment strategy should be determined by several factors, such as:

The goal of investing is when the value of your investments goes up, you can earn money on them. For example, a stock’s price won’t stay the same forever—ideally, the company grows and makes money, and it becomes more valuable overall. Historically, investments in assets like stocks, bonds, and real estate offer higher average returns than traditional savings accounts. While financial markets offer no certainties, investing opens doors to accelerated wealth accumulation, outpacing the growth achievable through saving alone.

By carefully considering these variables, you can determine the best investment strategy for your retirement savings. It’s important to remember that investments are not one-size-fits-all, and what may work for one person may not work for another. Take the time to research different investment options, and if needed, seek advice from a fiduciary advisor to help ensure your investment decisions align with your retirement goals.

Have an Emergency Savings Fund

Life emergencies happen—and for some, they happen a lot. Large or small, these unplanned expenses often feel like they hit at the worst times. An Emergency Fund acts as a safety net, helping to provide the financial resources you need to navigate unforeseen circumstances – without jeopardizing your long-term financial goals or your hard-earned nest egg.

Adequate cash reserves allow you to make decisions without solely relying on fixed-income sources. You can maintain flexibility in your financial choices, whether pursuing a new opportunity, supporting a loved one, or embarking on a passion project. Cash savings help ensure you won’t have to dip into or liquidate your investments, allowing your retirement portfolio to weather economic uncertainty.

By setting up a dedicated emergency fund, you can help protect yourself from chipping into your savings so you can recover quicker and get back on track towards reaching your larger savings goals.

Most professionals believe you should have enough money in your emergency fund to cover at least 3 to 6 months’ worth of living expenses. But it’s not unwise to save more during times of uncertainty. Building up your emergency fund can help prepare you and set your mind at ease if the unexpected should occur.

Plan for Long-Term Care

If you’ve not planned correctly, perhaps one of the biggest financial setbacks to retirees is long-term care. In 2024, without insurance, monthly long-term care costs might include:

Medicare does not pay for most long-term care expenses because it is primarily designed to cover acute care services for short-term illnesses and injuries. Many individuals opt for private long-term care insurance, Medicaid, or a combination of both to cover the cost of long-term care.

With the likelihood of needing long-term care increasing with age, it’s crucial to consider this aspect in your overall retirement plan. By taking a comprehensive approach to planning for healthcare costs, you can help ensure you have the necessary resources to pay for the level of care you may require.

Track Your Progress & Stay Informed

Monitoring your progress offers valuable learning opportunities. Regularly checking your retirement savings helps you spot potential issues early, like unexpected expenses or market changes. This allows you to take proactive steps, like adjusting your savings rate or rebalancing your investments. Monitoring your progress also helps ensure you’re moving closer to your retirement goals. Aim to review your retirement savings at least once a year and more frequently if your financial situation or investment strategy changes significantly.

Here are some tips to stay accountable during Financial Literacy Month:

Consider Working With a Fiduciary Advisor

Financial literacy is key to making smart financial choices, and a fiduciary advisor can be a valuable ally in helping you confidently navigate a complex financial landscape. If you’re unsure about your path to retirement, teaming up with a fiduciary advisor could provide much-needed support.

A fiduciary advisor is a professional who prioritizes their clients’ interests above all else. They can assist you in crafting a tailored retirement plan and staying focused on achieving your financial goals.

At Agemy Financial Strategies, our fiduciaries are dedicated to empowering our clients with knowledge across various financial domains. Our purpose is to educate retirees – whether that be planning for retirement, legacy planning, wealth management, or just holding your hand when it’s time to leap into retirement. We are celebrating 30 years in business, and we remain steadfast in our dedication to serving and educating retirees.

If you’re interested in learning more about our offerings, see here.

Final Thoughts

Whether you’re nearing the start of your retirement journey or newly retired, this process demands thorough preparation. While it can be stressful to see headlines about threats to the value of your nest egg, a volatile market does not necessarily mean danger for your retirement plans.

At Agemy Financial Strategies, we firmly believe in fostering financial stability and empowerment, particularly in the golden years of retirement. Our retirement income planning services are just one of our many resources designed to help you take control of your financial journey. This Financial Literacy Month, take charge of your retirement journey, overcome challenges, and pave the way for a secure and prosperous future with our team by your side.

Contact us today to schedule your complimentary retirement strategy session.

Connecticut vs. Colorado: Finding Your Ideal Retirement Destination

NewsMany Americans approaching retirement seek out a new location to spend their golden years, searching for a place that offers comfort and necessary resources. Whether you’re contemplating a move out of, into, or within Connecticut or Colorado, Agemy Financial Strategies is here to assist you.

As a financial firm based in Connecticut with offices in Colorado, we can offer you first-hand experience and knowledgeable advice on managing your retirement in these beautiful states. To start, let’s revisit some of the key pros and cons to consider.

Pro 1: Close Proximity to Major Cities

Nestled in the heart of New England, Connecticut exudes a classic charm that attracts retirees seeking a tranquil yet culturally rich environment. Connecticut’s location in the northeastern United States provides easy access to major cities like New York City and Boston.

Retirees can enjoy cultural attractions, world-class dining, and excellent healthcare facilities without traveling far. Connecticut boasts a rich historical heritage, with charming colonial towns, historic landmarks, and renowned museums. Retirees interested in history and culture will find plenty to explore in this picturesque state.

Pro 2: Connecticut Has a Longevity Advantage

For health enthusiasts, the concept of blue zones—areas where individuals consistently live past 100 years—holds significant intrigue. While these zones often exist in distant corners of the world, their longevity secrets offer valuable insights for everyone aiming to extend their lifespans.

According to Forbes Health, a recent study has positioned Connecticut as the fourth-ranking potential Blue Zone in the United States. Blue Zones are characterized by populations that live longer and lead healthier lives overall, with a notable number of residents reaching the centenarian mark. Connecticut stands out as one of the frontrunners among U.S. states primed to evolve into future Blue Zones.

Pro 3: Crime Rates are Falling

There’s a sense of safety, which is comforting to anyone. Connecticut is well known for its great, small community atmosphere. Many residents boast their small town feels more like a family. Connecticut witnessed a significant improvement in its crime rates between 2021 and 2022, as reported in the state’s annual crime report.

The report reveals a 13% decrease in violent crime, dropping from 6,272 offenses to 5,464. This decline marks the lowest violent crime rate per 100,000 residents the state has seen in the past decade. Additionally, property crime offenses also saw a decrease of 3% compared to the previous report.

Cons of Living in Connecticut

Con 1: High Cost of Living

Connecticut ranks among the states with the highest living expenses in the United States, especially regarding housing and taxes. Its cost of living consistently exceeds the national average, with studies indicating it could be anywhere from 17% to 25% higher than the rest of the country.

For retirees, this means their retirement savings may not go as far in Connecticut’s costly environment. Housing costs in Connecticut are generally higher than the national median. According to Zillow, the average home value in Connecticut is estimated to be around $384,244 as of February 2024, a 1-year Value Change of +11.1%

Con 2: High Taxes

Connecticut imposes a range of taxes that can significantly impact residents’ finances. The state’s income tax rates vary from 3% to 6.99%, with a corresponding 7.50% corporate income tax rate. In addition, the state sales tax rate stands at 6.35%, aligning closely with the national average.

Moreover, Connecticut’s property taxes further add to the financial burden, fluctuating based on the property’s assessed value and local tax rates. Compared to other states, Connecticut’s tax system ranks unfavorably, placing 47th overall on the 2024 State Business Tax Climate Index.

Con 3: Limited Outdoor Recreation

Connecticut experiences long, harsh winters characterized by cold temperatures and substantial snowfall, which may be challenging for those who prefer milder climates. While the state has beautiful natural scenery, it may offer fewer outdoor recreational opportunities than states like Colorado. Retirees who relish hiking, skiing, and fishing might yearn for a wider array of options.

Pro 1: Spectacular Scenery

Colorado presents an enticing option for retirees seeking an active lifestyle amidst breathtaking natural landscapes. It is known for its breathtaking natural beauty, sparkling lakes, and picturesque forests.

Colorful Colorado offers retirees abundant outdoor recreational activities, from skiing and snowboarding in the Rocky Mountains to hiking, biking, and fishing in the numerous state parks. Here are just some of the many places you can easily visit when retiring in Colorado:

Pro 2: Low Taxes

Colorado has relatively low taxes compared to many other states, making it an attractive option for retirees looking to stretch their retirement savings. The state income tax range is a low, flat rate of 4.4%, and you get a fair deduction on retirement income. Sales tax may run higher in the state, but it doesn’t apply to groceries or medication. Another great reason to retire in Colorado is that there’s no estate tax. You can leave money to your family without paying those hefty fees, which can be a huge perk.

Pro 3: Retirement Communities are an Abundance

Retirement communities offer an excellent opportunity to connect with like-minded individuals, fostering social interactions and shared interests. Colorado boasts over 240 retirement communities spread across the state, providing ample options for retirees seeking vibrant social environments. Allowing you to have the best of everything with neighbors your age and loads of activities to keep you as social and busy as you want to be.

Cons of Living in Colorado

Con 1: High Cost of Living

Living expenses in Colorado tend to surpass the national average. This holds true for assisted living costs as well. On average, monthly care expenses for assisted living in Colorado range from $3,800 to $6,200, exceeding the national average. In Denver, specifically, the average monthly cost stands around $5,000.

Even in rural and suburban areas, living expenses can be slightly higher than average. In mountain towns like Aspen, however, costs can soar much higher than the national average. Therefore, if you’re working with a tight budget, it’s crucial to thoroughly assess the cost of living in different Colorado cities before making any decisions.

Con 2: Cost of Healthcare

If you’re considering retiring in Colorado, factoring in the cost of care is crucial. Colorado experienced the second-highest increase in private health insurance premiums this year, trailing only Georgia, according to a recent report. The average monthly cost for a 40-year-old with a mid-range silver plan surged by 19.6% in Colorado, rising from $409 to $489 between 2022 and 2023. Nationally, the average premium increase stands at approximately 4%, with an average monthly cost of $560. However, when considering all age groups and coverage types, Colorado’s average rate hike is closer to 10.4%.

Con 3: Traffic Jams

Due to the popularity of Colorado, some residents have been irked by the overcrowding, and in very populated areas, traffic congestion is also a problem. These are somehow inevitable consequences of a popular place. As more and more people move to live there, the population increases and overcrowding continues. For retirees wishing to live in Colorado, the overcrowding can be a problem if you were hoping to move into a quiet and calm environment.

Comparing the Two States

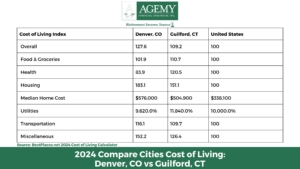

When weighing the options between Guilford, CT and Denver, CO, it’s important to consider several key factors. While Guilford generally offers a lower overall cost of living and provides more affordable housing options compared to Denver, the healthcare expenses in Guilford are notably higher. Therefore, the decision between these two cities may hinge on individual priorities and budgetary considerations. Here’s what we know about comparing Guilford, CT and Denver, CO:

Making Your Decision

Ultimately, the decision between Connecticut and Colorado comes down to your personal preferences, priorities, and lifestyle goals. Working alongside a trusted fiduciary advisor can help your transition to retirement. At Agemy Financial Strategies, our Connecticut and Colorado-based fiduciaries can provide valuable assistance in developing a retirement income plan that encompasses crucial financial factors, such as:

Our fiduciary advisors are committed to working closely with you to maximize your retirement years. We understand that retirement planning looks different for each individual, and with that in mind, we carefully craft your plan to meet your specific needs. For a complete list of our service offerings, see here.

Contact us today for more information on our retirement and financial planning services.