Retirement planning is a deeply personal journey, and one of the most pressing questions many Coloradans face is: “Is $1 million enough to retire comfortably in Colorado?”

The answer is nuanced and depends on various factors, including lifestyle choices, healthcare needs, housing decisions, and tax considerations.

At Agemy Financial Strategies, we believe in providing personalized financial guidance. This blog delves into the specifics of retiring in Colorado with a $1 million nest egg, offering insights tailored to the state’s unique economic landscape.

What $1 Million Looks Like in Retirement

Disclaimer: This material is for educational purposes only and does not constitute individualized financial, legal, or tax advice. Consult your professional fiduciary advisors about your specific situation and state-specific rules.

A commonly cited guideline is the 4% safe withdrawal rate (SWR), which suggests withdrawing 4% of your portfolio in the first year of retirement and adjusting that amount for inflation in subsequent years. For a $1 million portfolio, this equates to:

- 4% Withdrawal Rate: $40,000 per year before taxes.

While this serves as a helpful starting point, it’s essential to recognize that market returns, longevity, inflation, and sequence-of-returns risk can significantly impact whether that $40,000 lasts throughout retirement.

- 3.5% Withdrawal Rate: $35,000 per year.

- 5% Withdrawal Rate: $50,000 per year (with a higher risk of depleting the portfolio over time).

The adequacy of these amounts hinges on your annual spending needs after accounting for guaranteed income sources like Social Security, pensions, taxes, and major expenses such as housing and healthcare.

Colorado-Specific Factors: Cost of Living, Housing, Taxes, and Healthcare

Cost of Living

Colorado’s cost of living is approximately 13% higher than the national average, primarily driven by housing costs. This means that a retiree who needs $50,000 a year to live comfortably in a mid-cost state may require closer to $56,500 in Colorado for the same lifestyle.

Housing

The median home price in Colorado is around $541,198, with variations depending on the region. For instance, in Colorado Springs, the median home price has reached a record high of $500,000. If you’re mortgage-free, your housing expenses may be limited to property taxes and maintenance. However, if you still carry a mortgage, these costs can significantly impact your retirement budget.

Taxes

Colorado imposes a flat state income tax rate of 4.4% as of 2025. However, retirees may benefit from deductions on retirement income:

- Ages 55–64: Up to $20,000 in pension or annuity income can be deducted.

- Ages 65 and older: Up to $24,000 in pension or annuity income can be deducted.

This means that for many retirees, withdrawals from traditional IRAs or 401(k)s may be subject to both federal and state taxes, reducing your net spendable income.

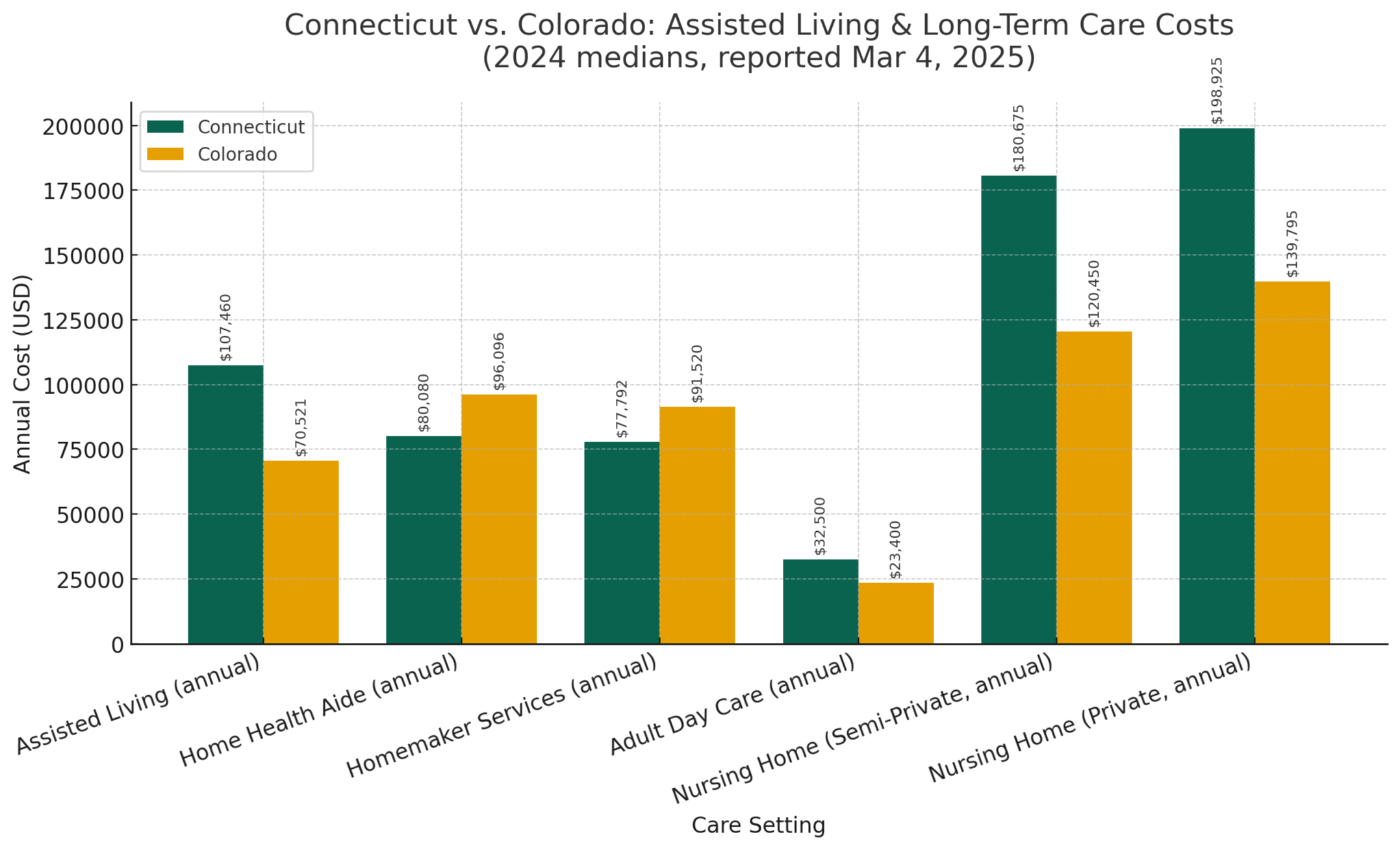

Healthcare and Long-Term Care Costs

Healthcare is often the single largest variable in retirement budgets. While Medicare covers many medical costs starting at age 65, premiums, supplemental plans (Medigap), prescription drugs, dental, hearing, and vision care add expenses. Long-term care, such as home health aides or nursing homes, can be extremely costly and varies by location. It’s crucial to plan for these potential expenses, as they can quickly erode your nest egg.

What Typical Retirees Actually Spend

National analyses show wide variation in retiree spending. Some households live on under $25,000 a year in retirement; others spend $60,000+, depending on lifestyle and location. Retirement researchers estimate average retiree household spending in the $40k–$60k range, depending on age group and region. Colorado’s higher cost of living pushes the local average toward the upper end of that range. Which group you fall into determines whether $1M is likely to be sufficient.

Scenario Analysis: Real Examples for Colorado Retirees

Below are simplified scenarios illustrating how a $1 million portfolio might fare in Colorado:

Scenario A — Modest Lifestyle, Mortgage-Free, Owns Car, Average Health

- Portfolio: $1,000,000 (taxable/Roth/IRA mix)

- Guaranteed income: Social Security $20,000/year

- Desired spending: $55,000/year gross

- Gap to fund from portfolio: $35,000/year

- Withdrawal rate required: 3.5%

Outcome: At a conservative 3.0–3.5% sustainable withdrawal rate, and if healthcare costs remain typical and taxes are managed, this retiree likely can sustain a comfortable, moderate Colorado retirement.

Scenario B — Active Lifestyle, Travel, Second Home, Some Healthcare Costs

- Portfolio: $1,000,000

- Social Security: $18,000/year

- Desired spending: $85,000/year

- Gap to fund from portfolio: $67,000/year → 6.7% initial withdrawal rate

Outcome: A 6.7% withdrawal rate is aggressive and likely unsustainable over a multi-decade retirement without other income sources. This retiree will likely exhaust the $1M or face significant lifestyle cuts unless they reduce spending, delay retirement, or generate supplemental income.

Scenario C — High Medical / Long-Term Care Risk

- Portfolio: $1,000,000

- Social Security: $22,000/year

- Desired living expenses: $60,000/year

- Unexpected long-term care: nursing facility costs or extended home health ($7,000–$12,000+/month depending on level and location)

Outcome: One year of high-level long-term care can easily consume $100k+, quickly eroding the nest egg. For retirees with a family history of chronic illness or cognitive decline risk, $1M alone may be insufficient unless long-term care insurance, hybrid life/long-term care products, or safety-net planning is arranged.

Practical Strategies to Make $1M Go Further in Colorado

If $1M is your starting point, you don’t have to accept doom or blind faith; there are practical levers:

- Secure a guaranteed income first: Maximize reliable income sources. Consider delaying Social Security if feasible (benefits grow for each year you delay up to age 70), understand pensions, and consider partial annuitization for a portion of savings to cover essential living expenses. Locking in income for basics reduces sequence-of-returns risk.

- Control housing costs: Housing is the single biggest expense for many Colorado retirees. Options:

- Pay off the mortgage before retiring to lower recurring expenses.

- Downsize to a smaller home or move to an area with lower property taxes.

- Consider a reverse mortgage only if you understand the tradeoffs.

- Rent in a desirable area to avoid high property taxes and maintenance (depends on the market).

- Tax-efficient withdrawal sequencing: Blend withdrawals from taxable accounts, tax-deferred IRAs, and Roth accounts strategically. Roth withdrawals can be tax-free; doing Roth conversions in lower-income years can help reduce future required minimum distributions and state tax exposure.

- Healthcare coverage and long-term care planning: Budget for Medicare premiums, supplemental insurance, and out-of-pocket costs. Evaluate long-term care insurance or hybrid life/LTC policies long before care is needed; premiums are lower and underwriting is easier at earlier ages.

- Adjust the withdrawal rate dynamically: Instead of a fixed 4% rule, use a dynamic withdrawal strategy that may help reduce spending after poor market returns and increase it after good performance. This adaptive approach improves portfolio longevity.

- Consider part-time work or phased retirement: Working part-time in retirement can help reduce withdrawals, delay Social Security, and preserve lifestyle.

- Estate and legacy planning: If leaving a legacy is important, structuring accounts, gifting strategies, and life insurance can help preserve some capital for heirs while still funding a comfortable retirement.

When $1M Is Likely Enough (And When It Isn’t)

$1M is potentially enough if:

- You own your home free and clear or have low housing costs.

- You expect a modest lifestyle (annual spending in the mid-$30k to low-$60k range).

- You have a guaranteed income (Social Security, pension) that covers a healthy portion of essential needs.

- You have relatively good health and low expected long-term care needs.

$1M is less likely to be enough if:

- You still carry a mortgage or high rent.

- You plan expensive travel or maintain multiple properties.

- You face high local property taxes or expensive private healthcare needs.

- You have family patterns that suggest a high probability of long-term care.

A Quick Sensitivity Example: How Taxes and COLA Affect the Number

Start with a $40,000 withdrawal (4% rule) on $1M. Subtract Colorado + federal tax (amount depends on filing status and deductions), even a modest combined effective tax rate of 15% reduces $40,000 to $34,000 net.

Then account for a Colorado cost-of-living premium of ~13% on your target spending bucket, that same lifestyle now needs roughly $45,000 in gross spending rather than $40,000.

That gap shows why $1M at 4% may not be enough once taxes and higher local costs are built into the plan.

How Agemy Financial Strategies Approaches the Question

At Agemy Financial Strategies, we don’t answer the “is $1M enough?” question with a single number. We help build personalized retirement blueprints that examine:

- Your current portfolio composition and tax status.

- Realistic spending needs and discretionary priorities.

- Housing and healthcare exposure, including the likelihood of long-term care.

- Social Security claiming strategies, pension options, and possible annuitization.

- A stress-tested withdrawal plan across market scenarios, including lower and higher volatility outcomes.

We model multiple scenarios (best case, base case, stress case) and present clear tradeoffs: retire now and reduce travel, delay retirement X years to improve odds, buy LTC insurance, do a partial annuitization, or adopt a dynamic spending plan.

Final Thoughts

$1,000,000 is a significant milestone and can absolutely fund a comfortable Colorado retirement for many people, especially if combined with Social Security, paid-off housing, good health, and disciplined withdrawals. But Colorado’s higher cost of living, property taxes, and the unpredictable cost of long-term care mean that $1M will not guarantee the same lifestyle everywhere in the state.

If you want certainty about your situation, the right next step is not to compare to a generic “enough” metric; it’s to run a plan using your actual numbers: your expected Social Security payout, your mortgage status, your desired annual spending, your health profile, and your tolerance for market risk.

Want to Know if $1M Is Enough for You?

At Agemy Financial Strategies, we’re highly experienced in retirement-income planning, “helping you make it down the mountain.” We’ll build a realistic, tax-aware plan, model how long your money will last under different scenarios, and create a practical path to the retirement lifestyle you want while protecting legacy goals.

Contact us today for a complimentary retirement readiness review and a custom scenario that answers the question specifically for your situation.

Visit agemy.com or call our office to schedule your consultation.

Investment advisory services are offered through Agemy Wealth Advisors, LLC, a Registered Investment Advisor and fiduciary to its clients. Agemy Financial Strategies, Inc. is a franchisee of Retirement Income Source®, LLC. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC are associated entities. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC entities are not associated with Retirement Income Source®, LLC. This content is for informational and educational purposes only and should not be construed as individualized investment, tax, or legal advice. Any review, reliance or distribution by others or forwarding without the express permission of the sender is strictly prohibited. To the extent permitted by law, Agemy Financial Strategies, Inc and Agemy Wealth Advisors, LLC, and Retirement Income Source, LLC do not accept any liability arising from the use or retransmission of the information in this article.