When most people think about retirement, they imagine freedom, travel, family time, and enjoying the fruits of a lifetime of hard work. But beneath those dreams often lies a lingering fear: “Will I run out of money?”

The truth is, many retirees are making the same critical mistake—they’re chasing growth in the stock market rather than securing reliable income. And that mistake can cost them not just peace of mind, but their entire retirement lifestyle.

Here’s what the smartest retirees know—and what most financial advisors don’t tell you: The key to a stress-free retirement isn’t about how much money you’ve saved, it’s about how much income your portfolio can generate.

Welcome to the retiree’s best-kept secret.

Why Income, Not Growth, Is the Foundation of a Secure Retirement

Most financial professionals build retirement plans around the idea of accumulating a large nest egg, usually invested heavily in growth stocks or mutual funds. The assumption is: “If the market keeps growing, your portfolio will too.”

But here’s the flaw: The market doesn’t grow in a straight line.

There are up years and down years. And if you’re withdrawing money from your portfolio during a down year, you’re not just losing value—you’re locking in losses and reducing your future income potential.

Instead, retirees should be thinking like landlords. Just as landlords collect rent month after month, regardless of the housing market’s value, retirees can—and should—collect steady income from investments designed to pay them regularly.

What Does Income-Based Retirement Look Like?

An income-first retirement strategy focuses on building a portfolio of assets that generates reliable, predictable cash flow. These include:

- Dividend-paying stocks

- Corporate and municipal bonds

- Preferred stocks

- Real estate investment trusts (REITs)

- Alternative fixed-income vehicles

This approach means your lifestyle isn’t dependent on whether the S&P 500 is up or down. You’ll know what’s coming in, month after month, year after year.

It’s not about growth—it’s about certainty.

How Is This Different from Traditional Retirement Planning?

Let’s look at a typical growth-based portfolio. If your $1.5 million nest egg is invested in stocks yielding 2%, you’ll get just $30,000/year in income. The rest depends on market gains, which can be unpredictable.

With an income-focused approach? That same $1.5 million could potentially generate $90,000/year in contractual or dividend income, and possibly more if actively managed for value.

And thanks to compounding and strategic trading, that “extra” 1–2% return each year could translate into over $300,000 in additional earnings over a decade.

Why Haven’t You Heard About This?

Because it doesn’t benefit Wall Street.

Wall Street firms make money whether you gain or lose, as long as your money stays invested. Their priority is assets under management, not the outcome of your retirement.

And frankly, many advisors simply don’t know how to build income-generating portfolios. The skill set required is different, more hands-on, and requires deep expertise in bonds, credit markets, and alternative income vehicles.

This is where Agemy Financial Strategies comes in.

How Agemy Financial Strategies Can Help

At Agemy Financial Strategies, we’ve been helping retirees enjoy stress-free retirements for over 30 years. We believe that everyone deserves a retirement defined by confidence, not anxiety.

Here’s how we do it:

✔ Income-First Planning: We prioritize building portfolios that generate contractual, predictable income, not just paper gains.

✔ Tactical Investment Management: Our team actively manages your portfolio to buy low, sell high, and capture additional yield—often gaining an extra 1–2% per year through professional trading strategies.

✔ True Diversification: We go beyond ETFs and mutual funds. Our clients enjoy portfolios that are resilient to market chaos and tailored to withstand volatility.

✔ Fiduciary Responsibility: As fiduciaries, we are legally and ethically obligated to put your interests first, not Wall Street’s.

✔ Personalized Retirement Income Plans: You’ll receive a custom roadmap with income projections, retirement milestones, and peace-of-mind calculations—so you know exactly how your money will support your goals.

We call this approach “More Life Than Money”—and we’d love to help you experience it firsthand.

Final Thoughts: Take the “Hope” Out of Retirement

A good retirement plan doesn’t rely on hope.

Hope that the market does well.

Hope that you don’t live too long.

Hope that you won’t outspend your savings.

Retirement should be lived with certainty, not speculation.

The retiree’s best-kept secret is simple: Invest for income, not just growth. And with the right strategy, you can enjoy more than enough income to live the way you want for the rest of your life, without fear of running out.

Frequently Asked Questions (FAQs)

- What is the biggest mistake retirees make with their money?

They stay invested in a growth-oriented portfolio and withdraw funds during market downturns—locking in losses. Shifting to an income-focused strategy helps provide more stability and predictability. - Is income investing safe?

Income investing can be very safe when diversified and managed properly. It focuses on assets with contractual payouts and less market volatility, potentially offering more consistent returns than growth-only strategies. - Can I still get growth in an income-focused portfolio?

Yes. While the primary goal is income, your portfolio can still grow. Active management can help provide strategic gains on top of the steady income stream—think of growth as the “icing on the cake.” - What’s the ideal time to switch from growth to income investing?

Typically, 5–10 years before retirement is the best time to start rebalancing toward income. But it’s never too late to make the shift—even if you’re already retired. - How do I get started with Agemy Financial Strategies?

Call us at 800-725-7616 or visit www.agemy.com. We’ll set up a free consultation to review your goals and explore how to help you maximize your retirement income.

Ready to make your income work for you?

Call Agemy Financial Strategies at 800-725-7616 for your free copy of the white paper “TR = I + G: The Formula for a More Successful Retirement” and begin your journey toward peace, purpose, and plenty in retirement.

Disclaimer: This content is for educational purposes only and should not be considered financial or investment advice. Please consult with the fiduciary advisors at Agemy Financial Strategies before making any investment decisions.

slowdown:

slowdown: 3. Tax Planning in an Evolving Landscape

3. Tax Planning in an Evolving Landscape foresight. That’s where

foresight. That’s where

2. Have a Sound Retirement Income Strategy

2. Have a Sound Retirement Income Strategy

4. Plan for Estate and Gift Taxes to Preserve Generational Wealth

4. Plan for Estate and Gift Taxes to Preserve Generational Wealth

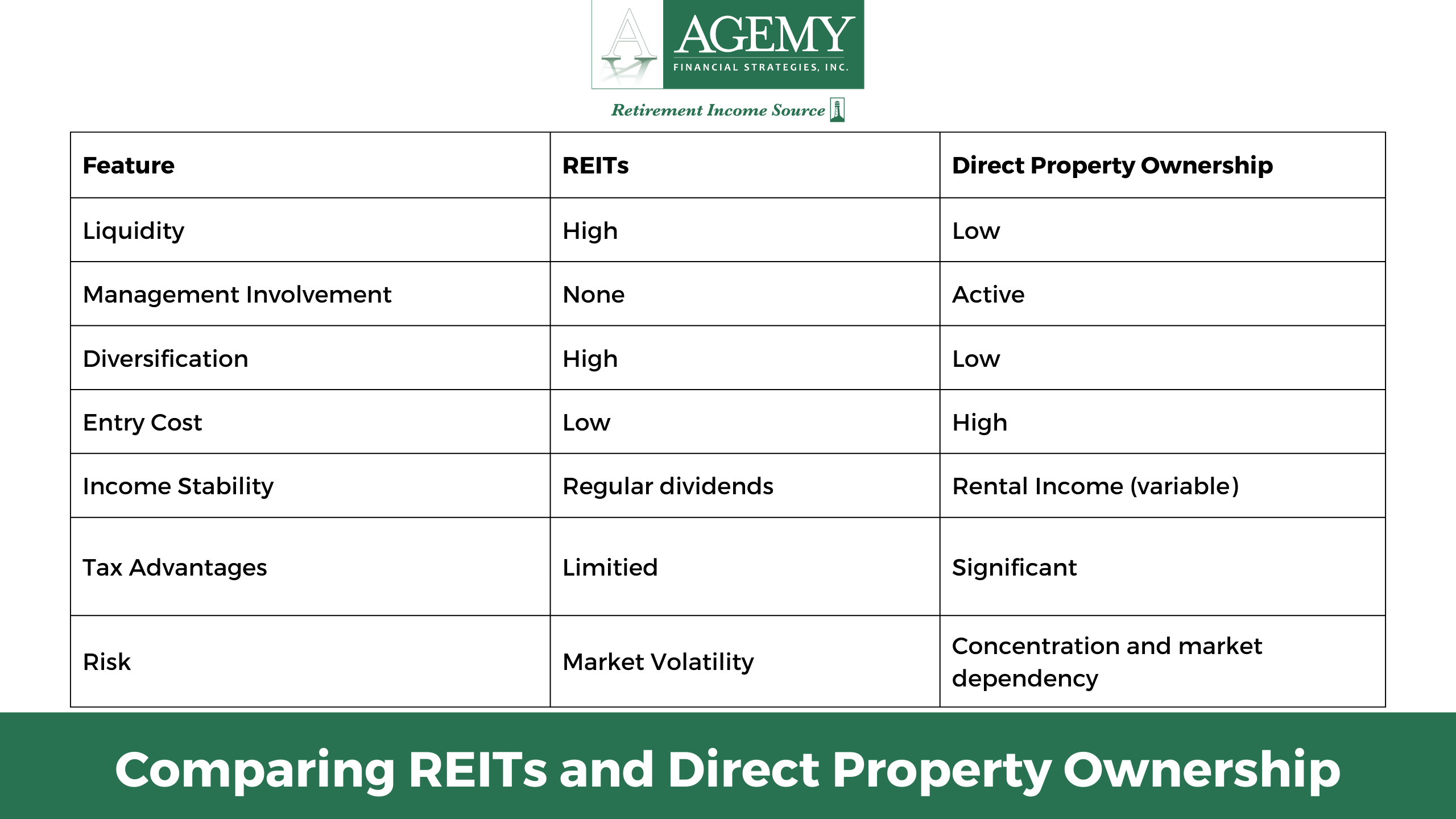

Cons of REITs

Cons of REITs

Cons of Direct Property Ownership

Cons of Direct Property Ownership

The Importance of Early Estate Planning

The Importance of Early Estate Planning Selecting Trustees and Beneficiaries

Selecting Trustees and Beneficiaries Regularly Review and Update Your Plan

Regularly Review and Update Your Plan

Cash Flow in Real Estate

Cash Flow in Real Estate

1. Real Estate Investments

1. Real Estate Investments

Having a Tax-Efficient Strategy

Having a Tax-Efficient Strategy

Lower Borrowing Costs

Lower Borrowing Costs

Alternative Real Estate Investment Strategies

Alternative Real Estate Investment Strategies