At Agemy Financial Strategies, we’re here to help you retire – AND STAY RETIRED.

Turning 60 is a milestone that prompts reflection—not just on life, but on money. If you have $2 million in a Roth IRA and a projected $2,000 monthly Social Security benefit, it’s natural to wonder: Does this mean I’m ready to retire?

The short answer: maybe—but it depends on more than your account balances. True retirement readiness goes beyond dollars and cents; it’s about aligning your lifestyle goals, risk tolerance, healthcare needs, taxes, and longevity expectations with your assets.

In this guide, we’ll explore how to evaluate whether your financial foundation is sufficient to retire comfortably, and the steps you can take to make that decision with confidence.

Understanding Your Starting Point

At age 60, many financial experts suggest a sustainable withdrawal rate in the 3.5%–4.7% range from a diversified portfolio. For a $2 million Roth IRA, that translates to roughly $70,000–$94,000 in annual withdrawals.

Add in your $2,000 monthly Social Security, which provides $24,000 per year of guaranteed, inflation-adjusted income, and your potential total annual income could range from $100,000 to $118,000. That’s a solid foundation—but readiness isn’t just a number; it’s whether this income can realistically support your lifestyle over the next 30+ years.

Why the Roth IRA Matters

Your Roth IRA offers a unique advantage:

- Tax-free withdrawals after age 59½ and five years of account ownership.

- No required minimum distributions (RMDs) during your lifetime.

- Flexibility to time withdrawals to meet income needs or tax planning goals.

This makes your Roth IRA both a spending vehicle and a long-term strategic tool. But having money isn’t the same as being ready; you need a plan for using it effectively.

Assessing Your Retirement Lifestyle Needs

Money alone doesn’t define retirement readiness. Lifestyle is equally important. To determine whether you’re ready, ask yourself:

- How much do I spend now, and how might that change in retirement?

- What lifestyle do I envision—travel, hobbies, supporting family, or philanthropy?

- What level of financial security will give me peace of mind?

Sustainable Withdrawal Estimates

Research suggests retirees with a balanced portfolio (roughly 30–50% equities) may target 3.9% initial withdrawals as a conservative baseline. On $2 million, this is about $78,000 in year one. More flexible planning could allow $90,000–$94,000, depending on market conditions and risk tolerance.

Adding Social Security income of $24,000, your first-year retirement income could reach $100,000–$118,000, providing a solid foundation for a comfortable lifestyle.

Social Security: Timing Is Everything

Your $2,000 monthly Social Security benefit is a guaranteed income source, but the timing of claiming can make a significant difference:

- Early claim at 62: reduces benefits permanently by ~25–30%.

- Full Retirement Age (66–67): receive the full benefit of $2,000.

- Delayed claim to 70: boosts your benefit by up to 32% through delayed retirement credits.

Many retirees use their Roth IRA or other savings to fund early retirement years while allowing Social Security to grow. This strategy can create a higher guaranteed income floor in your later 70s and 80s, helping to protect against longevity risk.

Building a Strategic Roth IRA Withdrawal Plan

Even with a tax-free Roth, a thoughtful withdrawal strategy matters:

Step 1: Confirm Your Roth Rules

- You’re past age 59½, but ensure the five-year rule is satisfied.

- Confirm how much of your withdrawals will be tax-free, particularly if you opened multiple Roth accounts at different times.

Step 2: Asset Allocation for Retirement

- Equities for growth: help protect against inflation and extend portfolio longevity.

- High-quality bonds/fixed income: reduce volatility and provide predictable income.

- Cash reserve: cover 1–3 years of spending to avoid selling during market downturns.

The goal is to balance growth and security, helping ensure your portfolio supports decades of spending while preserving upside potential.

Step 3: Roth + Social Security Coordination

- Use Roth withdrawals to fund early retirement years if delaying Social Security.

- Tax-free Roth withdrawals minimize taxable income, reducing Medicare and Social Security taxation.

A well-designed strategy blends guaranteed and flexible income to help maximize lifetime financial security.

Evaluating Risk in Retirement

Even with strong assets, retirement readiness also involves mitigating key risks:

Sequence of Returns Risk

Early withdrawals during market downturns can erode retirement assets.

Mitigation strategies may include:

- Maintaining a cash or short-term bond buffer for several years of expenses.

- Adopting flexible withdrawal strategies: reduce spending after negative market years and increase after positive years.

Research indicates retirees willing to adjust spending may safely withdraw more initially than those with rigid inflation-adjusted budgets.

Inflation and Longevity

Over a 30–35-year retirement, inflation can erode purchasing power:

- Maintaining some equity exposure is typically necessary.

- Stress-testing to age 90–95 ensures your portfolio can support extended lifespans.

Your Roth IRA growth acts as a hedge against rising costs and market volatility.

Healthcare and Long-Term Care

Healthcare is often the largest expense in retirement:

- Plan for Medicare premiums, supplemental insurance, and out-of-pocket costs.

- Consider long-term care insurance, hybrid life/LTC policies, or self-funding a portion of expenses.

Retirement readiness isn’t just financial; it’s practical planning for real-life contingencies.

Tax Planning Considerations

Even tax-free Roth withdrawals can interact with other income sources:

- Social Security may be partially taxable, depending on other income.

- Withdrawals from taxable or traditional accounts can push you into higher tax brackets.

- Roth IRAs give flexibility, but planning helps ensure that income sequencing and potential Roth conversions maximize tax efficiency.

Key takeaway: A tax-efficient strategy helps preserve wealth and reduces surprises in retirement.

Estate, Legacy, and Philanthropy Planning

Part of retirement readiness is ensuring your wealth works for you and your loved ones:

- Estate planning: review wills, powers of attorney, healthcare directives, and IRA beneficiary designations.

- Legacy planning: Roth IRAs can be passed tax-free to heirs, maximizing long-term family wealth.

- Charitable goals: consider Qualified Charitable Distributions (QCDs) from IRAs after 70½ to reduce taxable income.

A comprehensive approach integrates income, legacy, and philanthropy, helping ensure your assets fulfill your long-term vision.

Lifestyle and Location Considerations

Agemy Financial Strategies serves clients in both Colorado and Connecticut, and location can impact readiness:

- Colorado: Mountain or urban living may involve higher housing, property taxes, and lifestyle costs. Outdoor hobbies, vacation homes, and winter recreation can affect budgets.

- Connecticut: High cost-of-living areas, especially near Hartford or Fairfield County, may require a higher income to maintain the same lifestyle. Property taxes and healthcare costs can also be significant.

Your retirement income needs should match your desired lifestyle in your specific location. A $2 million Roth IRA and Social Security may be more than sufficient in one area, yet barely cover expenses in another.

Checking Your Retirement Readiness

Here’s a practical checklist to assess if you’re truly ready:

- Lifestyle alignment: your income supports your ideal retirement lifestyle.

- Withdrawal strategy: Roth IRA and Social Security withdrawals are coordinated.

- Risk management: sequence-of-returns, inflation, longevity, and healthcare are addressed.

- Tax efficiency: your plan minimizes lifetime taxes.

- Estate planning: wills, powers of attorney, and beneficiaries up to date.

- Location considerations: income supports your preferred lifestyle in Colorado or Connecticut.

If these boxes are checked, you’re likely ready. If not, you may need adjustments or phased retirement strategies.

Practical Steps for Those Considering Retirement

Step 1: Build a Written Plan

- Map income sources and withdrawal strategies.

- Stress-test under different market scenarios and life expectancy assumptions.

- Update as circumstances change; retirement isn’t static.

Step 2: Model Social Security Options

- Compare claiming at 62, FRA, and 70.

- Identify how portfolio withdrawals can bridge the gap to delayed benefits.

Step 3: Coordinate Taxes and Investments

- Sequence withdrawals for tax efficiency.

- Consider Roth conversions where appropriate.

- Maintain asset allocation aligned with income needs and risk tolerance.

Step 4: Address Risk Management

- Review healthcare and long-term care strategies.

- Maintain sufficient cash or bonds for emergencies.

- Confirm insurance and estate planning align with retirement goals.

Does This Mean You’re Ready for Retirement?

Having $2 million in a Roth IRA and $2,000/month Social Security is a strong foundation, but readiness isn’t automatic. It depends on:

- Whether your income supports your desired lifestyle for 30+ years.

- How well you’ve planned for key risks like market downturns, inflation, and healthcare.

- Whether Social Security timing and Roth withdrawals are coordinated for efficiency.

- Whether you have a written plan integrating taxes, lifestyle, and legacy goals.

If yes, you’re likely ready.

If not, you may need planning tweaks, phased retirement strategies, or adjustments to lifestyle expectations to ensure comfort and security.

How Agemy Financial Strategies Can Help

Agemy Financial Strategies is highly experienced in retirement income planning, guiding clients from accumulation to sustainable income strategies. Our approach includes:

- Detailed cash-flow projections for 30+ year horizons.

- Social Security modeling to help maximize guaranteed lifetime income.

- Coordinated withdrawal strategies across Roth, traditional, and taxable accounts.

- Stress-testing for longevity, inflation, and market volatility.

- Location-specific planning for Colorado and Connecticut clients, helping ensure retirement readiness in high-cost or mountain-area markets.

With offices in Colorado and Connecticut, Agemy helps clients turn impressive balances into confidence, allowing you to enjoy retirement without uncertainty.

Bottom line: Having $2 million in a Roth IRA and $2,000/month Social Security is impressive – but retirement readiness is about strategy, flexibility, and confidence. With the right plan, you can retire comfortably, with peace of mind, and fully enjoy the lifestyle you’ve worked for.

Retire and stay retired with Agemy Financial Strategies. Schedule a consultation here today.

Investment advisory services are offered through Agemy Wealth Advisors, LLC, a Registered Investment Advisor and fiduciary to its clients. Agemy Financial Strategies, Inc. is a franchisee of Retirement Income Source®, LLC. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC are associated entities. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC entities are not associated with Retirement Income Source®, LLC. This content is for informational and educational purposes only and should not be construed as individualized investment, tax, or legal advice. Any review, reliance or distribution by others or forwarding without the express permission of the sender is strictly prohibited. To the extent permitted by law, Agemy Financial Strategies, Inc and Agemy Wealth Advisors, LLC, and Retirement Income Source, LLC do not accept any liability arising from the use or retransmission of the information in this article.

slowdown:

slowdown: 3. Tax Planning in an Evolving Landscape

3. Tax Planning in an Evolving Landscape foresight. That’s where

foresight. That’s where

2. Have a Sound Retirement Income Strategy

2. Have a Sound Retirement Income Strategy

A Fiduciary’s Perspective on Long-Term Wealth Growth

A Fiduciary’s Perspective on Long-Term Wealth Growth

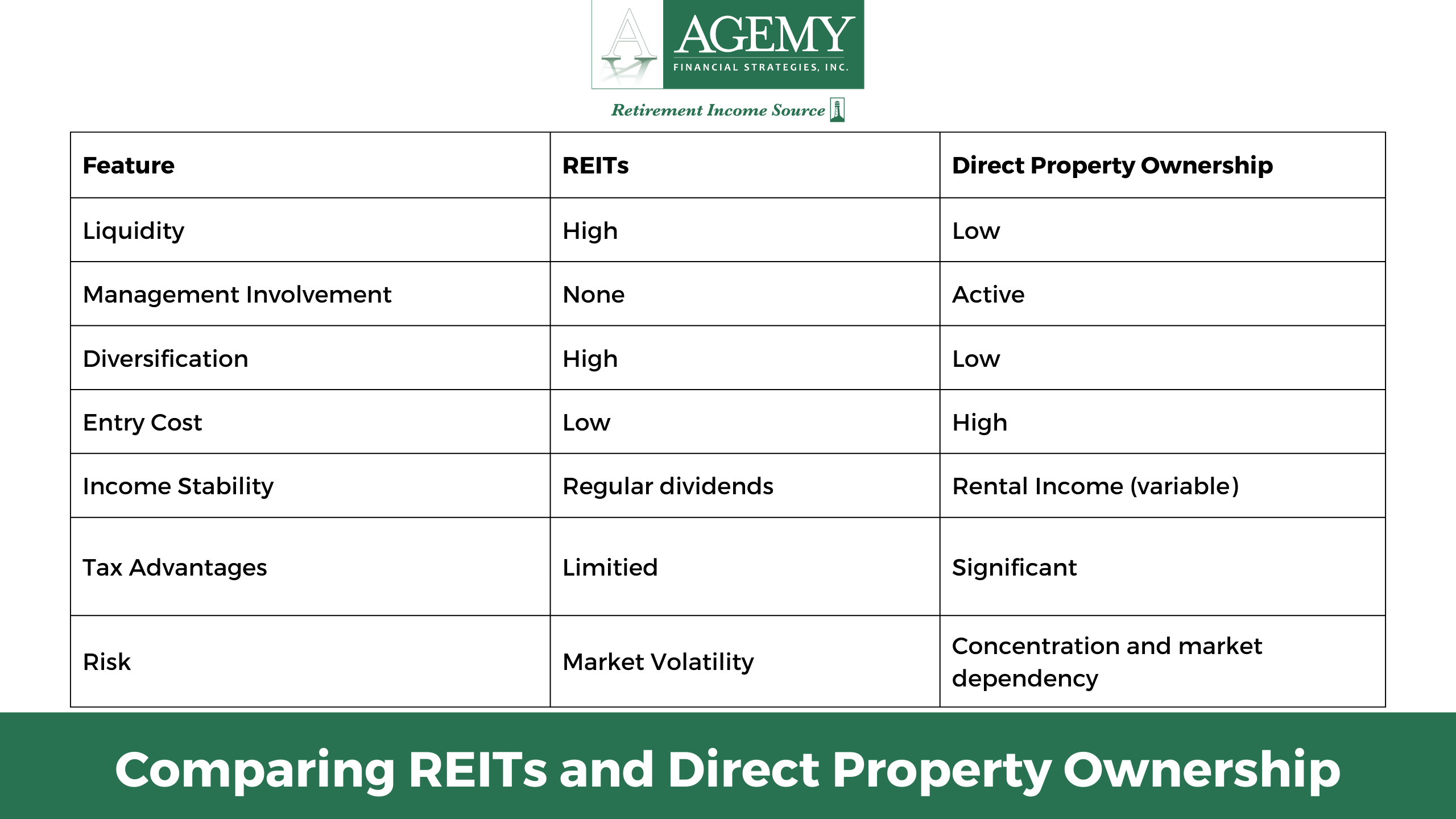

Cons of REITs

Cons of REITs

Cons of Direct Property Ownership

Cons of Direct Property Ownership

Savings and Investments: Adapting to a New Landscape

Savings and Investments: Adapting to a New Landscape

The Importance of Fiduciary Guidance

The Importance of Fiduciary Guidance