When you hear the word “growth” in relation to your retirement portfolio, what comes to mind?

It’s a simple question, but the answer is almost embarrassingly complex because the financial industry and everyday retirees speak two entirely different languages. Much like how ancient Greek had four different words to describe the nuances of “love,” the modern financial world desperately needs different words to describe “growth.”

For decades, you’ve been trained to chase one specific type of growth. But as you transition from your working years into retirement, chasing that same definition can be one of the most dangerous risks to your financial security.

It is time to unlearn the habits of your accumulation years and discover the income secret that retirees seldom learn: the profound difference between Known Growth and Unknown Growth.

The Great Misunderstanding: Defining “Growth”

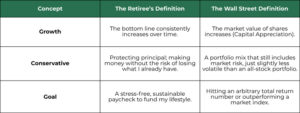

When most retirees say they want “growth,” they mean something very straightforward: they want to see their bottom line go up consistently, and they don’t want to lose their principal. They are looking for conservative, steady progression.

However, when a traditional wealth manager or financial advisor hears the word “growth,” they hear something else entirely: capital appreciation. They hear, “I want my share prices to go up.”

Here is the problem: in order for share prices to go up, they must also have the capacity to go down.

The Disconnect

When your definition of growth doesn’t match your portfolio’s reality, you expose yourself to sudden, unexpected drawdowns.

A 40% drop on a $40,000 account when you are 30 years old is an inconvenience. A 40% drop on a $1,000,000 account when you are retiring next month—reducing your life savings to $600,000—is a life-altering disaster.

It can mean canceling vacations, changing your lifestyle, or even un-retiring and going back to work.

Two Paths to the Top: The Elevator vs. The Escalator

To understand the difference between Unknown Growth and Known Growth, imagine you are standing in the lobby of a high-rise building, trying to get to the penthouse. You have two choices:

1. The Elevator (Unknown Growth)

You step into the elevator, hit the button for the penthouse, and the doors close. Suddenly, the elevator shoots up 25 floors, drops down 15 floors, and plummets into the basement.

Your stomach drops. You panic. Why is this happening?

You quickly realize that you are not the one pushing the buttons. The Federal Reserve is pushing the buttons. Quant funds are pushing the buttons. Global economic events, investor sentiment, and hedge fund managers are pushing the buttons. You are locked in a metal box with flashing lights, entirely out of control, hoping you eventually reach the top. If the doors open on the wrong floor right when you need your money, you lose.

This is the reality of relying solely on the stock market for capital appreciation. It can be stressful, unpredictable, and relies entirely on hope.

2. The Escalator (Known Growth)

Now, imagine you choose the escalator.

It moves a bit slower, but the progression is methodical and consistent. You step on, and it simply goes up. You don’t get that gut-wrenching drop in your stomach. There is no stop-and-go traffic, no slamming on the brakes. Furthermore, you can look around, enjoy the view, and actually relax.

If you want to move faster, you can walk up the steps. But you don’t have to. You can just chill out and let the escalator do the work.

This is Known Growth. It is built on steady, reliable, and predictable income strategies rather than the erratic whims of the stock market.

The Formula for Real Growth: G = I + CA

To shift your mindset from the elevator to the escalator, you need to understand the true equation for growing your money in retirement:

G = I + CA

(Growth = Income + Capital Appreciation)

There are two primary ways to grow an account, but the financial industry largely focuses on just one.

The Trap of Capital Appreciation (CA)

Capital appreciation means your asset’s value increases over time. But here is the harsh reality: equity is not money. If you own a stock that skyrockets by 300%, you haven’t actually made a single dime of growth until you sell that stock.

If you don’t sell, and the market crashes the next day, that “growth” vanishes into thin air. Relying on capital appreciation means you have to have perfect timing. If the “market gods” do not cooperate with you the year you decide to retire, your portfolio could be wrecked.

The Power of Income (I)

Income represents dividends, interest, and cash flow generated by your assets. Unlike stock prices, which fluctuate wildly based on market sentiment, income is often contractual.

Imagine you have $100 invested, and it pays a $3 dividend. Regardless of what the stock market does that day—whether it crashes or sets a record high—you still received your $3. Your account grew to $103 organically.

When you prioritize Income (I) over Capital Appreciation (CA), you flip the Wall Street model upside down. Instead of hoping for 7% to 8% in stock market growth and settling for a meager 1% to 2% in dividends, an income-focused strategy aims to generate a robust 6% to 7% in steady cash flow, with any capital appreciation acting as the cherry on top.

On a $1,000,000 portfolio, that is the difference between hoping to sell shares at the right time versus knowing you have $60,000 to $70,000 in cash coming into your account every single year.

The Danger of the “401(k) Brain” and Sequence of Returns Risk

Why is it so difficult for people to grasp this concept? Because for 30 or 40 years, we have been conditioned to have a “401(k) brain.”

Forty years ago, everyday workers didn’t have to worry about stock market volatility because they had pensions. When they retired, they received a guaranteed check every month. Today, the burden of retirement has shifted to the individual via 401(k)s and savings accounts, forcing everyday people to become amateur portfolio managers.

This “401(k) brain” teaches us to build a massive pile of money and then slowly withdraw from it using rules of thumb, like taking out 4% a year. But this can expose retirees to one of the most devastating financial dangers: Sequence of Returns Risk.

When you retire and start withdrawing money matters deeply:

- Retiring in 2010: If you retired in 2010 and took out $40,000 a year, you experienced a massive, historic bull market. Your portfolio likely grew despite your withdrawals.

- Retiring in 2007: If you retired in 2007, took out $40,000, and then the market crashed by 50%, you were suddenly withdrawing money from a severely depleted account. You had to sell shares at rock-bottom prices just to survive, locking in those losses permanently. Many people in this scenario simply ran out of money.

When you shift to an income model, Sequence of Returns Risk practically disappears. If your portfolio generates enough organic income through dividends and interest to fund your lifestyle, you never have to sell your underlying principal. It doesn’t matter what the stock market is doing on any given Tuesday, because you aren’t forced to sell your assets to pay your bills.

Roosters vs. Chickens: How Do You Want to Eat in Retirement?

When you are in retirement, you still have to eat. You can approach your portfolio in one of two ways:

- Investing in Roosters (Capital Appreciation): If your portfolio is built on pure growth, you own a flock of roosters. To eat, you have to kill a rooster. If you kill too many roosters during a bad season (a market downturn), eventually, you will look out at your yard and realize you’ve run out of roosters. You are out of money.

- Investing in Chickens (Income and Dividends):

If your portfolio is built on income, you own chickens. You don’t eat the chickens; you eat the eggs. You have a renewable, stress-free resource. If your chickens produce more eggs than you need to eat that year, you can take the surplus, buy more chickens, and increase your egg production for the following year.

This is the ultimate secret to a stress-free retirement. Do not kill your roosters. Buy chickens, eat the eggs, and enjoy the peace of mind that comes with knowing your resources are renewable.

From Hope to Knowing

Retirement is a massive life transition. Your schedule changes, your social circles change, and the paycheck you relied on for 40 years stops coming. There is an emotional weight—even grief—that comes with the end of your working life.

You do not need to add the stress of the stock market to that transition.

You deserve a strategy, not just a plan. A plan is throwing a football down the field and hoping someone is there to catch it. A strategy is built on known factors: knowing exactly how much income your portfolio will generate, knowing you don’t have to constantly check the financial news, and knowing your money will last.

If you want your retirement to be stress-free, invest for the “I” (Income) rather than the “G” (Unknown Growth). Step off the terrifying elevator, get on the escalator, and finally enjoy the view.

How Agemy Financial Strategies Can Help You Make the Shift

Transitioning from a lifetime of accumulation (unknown growth) to a sustainable income mindset (known growth) is one of the hardest mental shifts to make, but you don’t have to navigate it alone.

For over 30 years, Andrew and Daniel Agemy have helped individuals aged 50 and over build custom plans designed to keep them retired and stress-free. As fiduciaries, their obligation is legally and ethically bound to your best interest, not just what is “suitable.”

Here is how the team at Agemy Financial Strategies can help you step off the elevator and onto the escalator:

- The Portfolio Stress Test (Your Financial MRI): Do you know exactly what would happen to your life savings if we experienced another 2008-level financial crisis, or conversely, a 2013-style market run-up? Agemy Financial offers a free, no-obligation stress test to look backward and forward at your current portfolio, so you can make informed, smart decisions rather than relying on hope.

- The Retirement Readiness Report (RR): Stop relying on generic online calculators and rules of thumb. The RR is a personalized analysis designed to answer the exact questions keeping you up at night: Can I retire? When can I retire? How much do I actually need?

- Custom Retirement Income Planning: The goal isn’t just to hit an arbitrary total return number; it is to build a steady, reliable “retirement paycheck” using dividends, interest, and contractual income that pays you regardless of what the stock market is doing today.

Ready to find your Known Growth? Reach out to us at agemy.com.