“Is $1 million enough to retire comfortably in Connecticut?” It’s one of the most asked questions in retirement planning, and the honest answer is: it depends.

The short version: for some people in Connecticut, $1 million can fund a comfortable retirement if they plan carefully and have low housing or health-care burdens; for others, especially those facing high mortgage payments, expensive long-term care needs, or a desire for an active, travel-heavy lifestyle, it may fall short.

This blog walks through the numbers, the Connecticut-specific factors that change the calculus, realistic scenarios, and practical strategies to help you (or your clients) decide whether $1M will get you down the mountain, and how Agemy Financial Strategies can help plan the descent.

The Basic Math: What $1M Looks Like in Retirement

Disclaimer: This material is for educational purposes only and does not constitute individualized financial, legal, or tax advice. Consult your professional fiduciary advisors about your specific situation and state-specific rules.

A common rule of thumb is the 4% safe withdrawal rate (SWR): withdraw 4% of your portfolio in year one, then adjust that dollar amount for inflation each subsequent year. On a $1,000,000 portfolio, 4% = $40,000 per year before taxes. That’s a helpful starting point, but it’s only a guideline, not a guarantee. Market returns, longevity, inflation, and sequence-of-returns risk can make a big difference in whether that $40,000 lasts 30+ years.

If you target a more conservative 3.5% withdrawal, that’s $35,000 per year. If you’re aggressive and accept more risk, a 5% withdrawal yields $50,000 initially, but with a higher chance of depleting the portfolio over a long retirement. Those small percentage differences matter a lot when you multiply them by decades. (1,000,000 × 0.04 = 40,000; 1,000,000 × 0.035 = 35,000; 1,000,000 × 0.05 = 50,000.)

Which number is “enough” hinges on your annual spending needs after factoring in guaranteed income (Social Security, pensions), taxes, and major expected costs like housing and healthcare.

Connecticut Matters: Cost of Living, Housing, Taxes, and Long-Term Care

Cost of Living

Connecticut’s overall cost of living index is well above the national average. Multiple cost-of-living trackers place Connecticut roughly 12–13% higher than the U.S. average, driven largely by housing and utilities. That means a retiree who needs $50,000 a year to live comfortably in a mid-cost state may need closer to $56,000–$57,000 in Connecticut for the same lifestyle.

Housing/Home Prices

Median home prices in Connecticut vary widely by county and town (coastal Fairfield County towns are far pricier than inland Litchfield or Windham County), but statewide median sale prices recently have been in the mid-$400k range according to current market trackers. If you still have a mortgage in retirement, a higher home price translates into higher recurring housing costs and pressure on your nest egg. If you own your home outright, property taxes and maintenance remain important considerations: Connecticut has among the highest effective property-tax rates relative to home value in the nation.

State Taxes on Retirement Income

Connecticut’s tax rules can affect how far $1M will go. Connecticut taxes many types of retirement income; Social Security benefits may be exempt for lower-income seniors, but pension and IRA distributions are generally taxable at the state level (with some exemptions and phase-outs for certain incomes or ages). That means withdrawals from a traditional IRA or taxable account may face both federal and Connecticut income tax, reducing your net spendable income. Tax treatment varies by individual circumstance, so state taxation is an essential piece of planning for Connecticut retirees.

Healthcare and Long-Term Care Costs

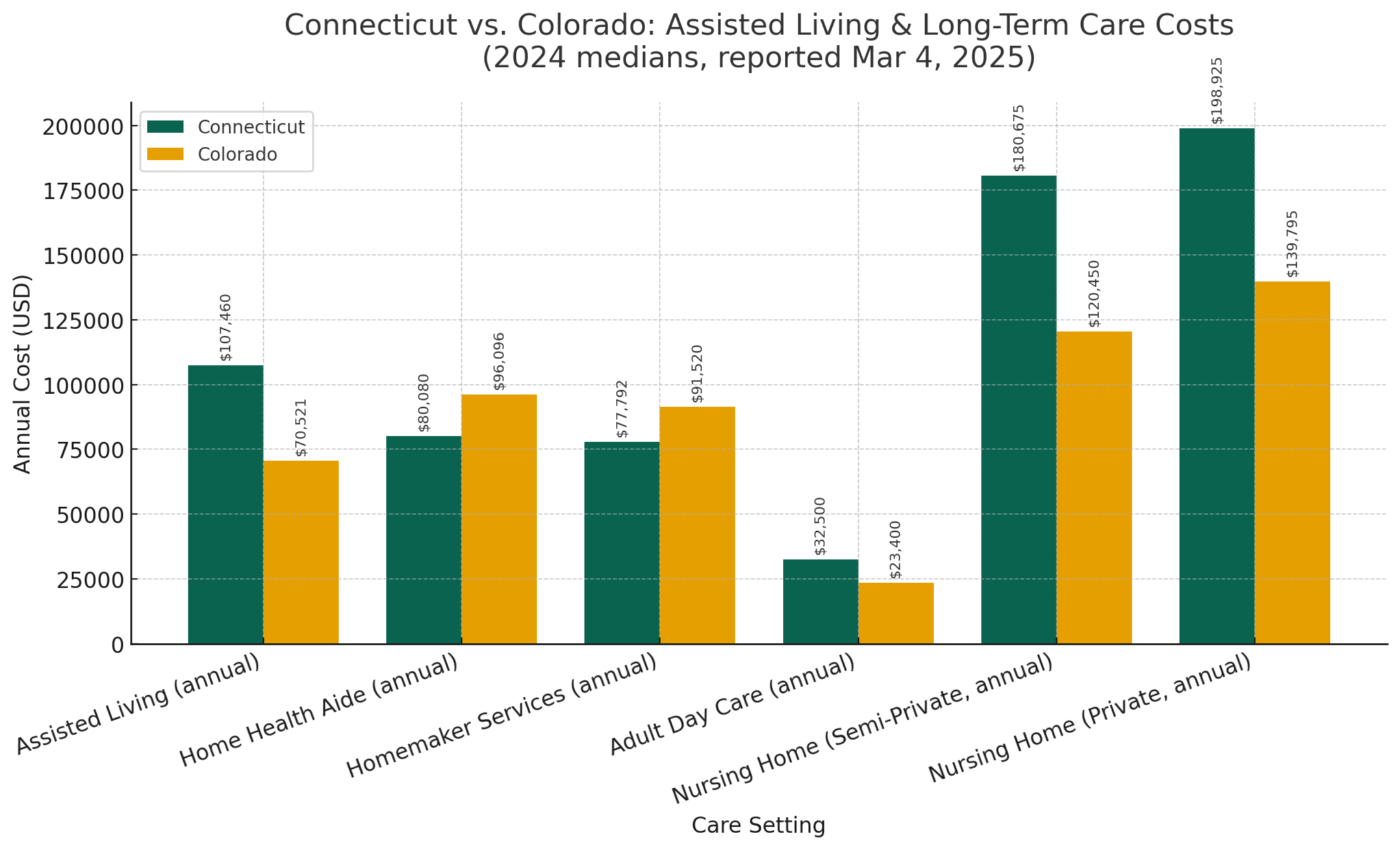

Healthcare is often the single largest variable in retirement budgets. Medicare covers many medical costs beginning at age 65, but premiums, supplemental plans (Medigap), prescription drugs, dental, hearing, and vision care add expenses. Long-term care (home health aides, assisted living, nursing homes) can be extremely expensive and is priced locally. Connecticut’s state data and reports show a wide range of private-pay rates for home health and nursing care by town and agency; many retirees underestimate this cost. If long-term care is needed, a large portion of a $1M nest egg can be consumed quickly.

What Typical Retirees Actually Spend

National analyses show wide variation in retiree spending. Some households live on under $25,000 a year in retirement; others spend $60,000+, depending on lifestyle and location. Retirement researchers estimate average retiree household spending in the $40k–$60k range, depending on age group and region. Connecticut’s higher cost of living pushes the local average toward the upper end of that range. Which group you fall into determines whether $1M is likely to be sufficient.

Scenario Analysis: Real Examples for Connecticut Retirees

Below are simplified scenarios; real retirements are messier, but these illustrate the tradeoffs.

Scenario A — Modest Lifestyle, Mortgage-Free, Owns Car, Average Health

- Portfolio: $1,000,000 (taxable/Roth/IRA mix)

- Guaranteed income: Social Security $20,000/year

- Desired spending: $55,000/year gross

- Gap to fund from portfolio = $35,000/year

- Withdrawal rate required = 3.5% (1,000,000 × 0.035 = 35,000)

Outcome: At a conservative 3.0–3.5% sustainable withdrawal, and if healthcare costs remain typical and taxes are managed, this retiree likely can sustain a comfortable, moderate Connecticut retirement. This scenario benefits from being mortgage-free and having Social Security. Taxes on withdrawals and state income tax still reduce spendable income, so careful tax-aware withdrawal sequencing (Roth conversions, taxable vs. tax-deferred withdrawals) helps.

Scenario B — Active Lifestyle, Travel, Second Home, Some Healthcare Costs

- Portfolio: $1,000,000

- Social Security: $18,000/year

- Desired spending: $85,000/year

- Gap to fund from portfolio = $67,000/year → 6.7% initial withdrawal rate

Outcome: A 6.7% withdrawal rate is aggressive and likely unsustainable over a multi-decade retirement without other income sources. This retiree will likely exhaust the $1M or face significant lifestyle cuts unless they reduce spending, delay retirement, or generate supplemental income.

Scenario C — High Medical / Long-Term Care Risk

- Portfolio: $1,000,000

- Social Security: $22,000/year

- Desired living expenses: $60,000/year

- Unexpected long-term care: nursing facility costs or extended home health ($7,000–$12,000+/month depending on level and location)

Outcome: One year of high-level long-term care can easily consume $100k+, quickly eroding the nest egg. For retirees with a family history of chronic illness or cognitive decline risk, $1M alone may be insufficient unless long-term care insurance, hybrid life/long-term care products, or safety-net planning is arranged.

Practical Strategies to Make $1M Go Further in Connecticut

If $1M is your starting point, you don’t have to accept doom or blind faith; there are practical levers:

1. Secure a guaranteed income first

Maximize reliable income sources. Consider delaying Social Security if feasible (benefits grow for each year you delay up to age 70), understand pensions, and consider partial annuitization for a portion of savings to cover essential living expenses. Locking in income for basics reduces sequence-of-returns risk.

2. Control housing costs

Housing is the single biggest expense for many Connecticut retirees. Options:

- Pay off the mortgage before retiring to lower recurring expenses.

- Downsize to a smaller home or move to an area with lower property taxes.

- Consider a reverse mortgage only if you understand the tradeoffs.

- Rent in a desirable area to avoid high property taxes and maintenance (depends on the market).

3. Tax-efficient withdrawal sequencing

Blend withdrawals from taxable accounts, tax-deferred IRAs, and Roth accounts strategically. Roth withdrawals can be tax-free; doing Roth conversions in lower-income years can help reduce future required minimum distributions and state tax exposure.

4. Healthcare coverage and long-term care planning

Budget for Medicare premiums, supplemental insurance, and out-of-pocket costs. Evaluate long-term care insurance or hybrid life/LTC policies long before care is needed; premiums are lower and underwriting is easier at earlier ages.

5. Adjust the withdrawal rate dynamically

Instead of a fixed 4% rule, use a dynamic withdrawal strategy that reduces spending after poor market returns and increases it after good performance. This adaptive approach improves portfolio longevity.

6. Consider part-time work or phased retirement

Working part-time in retirement can help reduce withdrawals, delay Social Security, and preserve lifestyle.

7. Estate and legacy planning

If leaving a legacy is important (as many Connecticut families expect to pass wealth to children or charities), structuring accounts, gifting strategies, and life insurance can help preserve some capital for heirs while still funding a comfortable retirement.

Rules of Thumb: When $1M Is Likely Enough (And When It Isn’t)

$1M is potentially enough if:

- You own your home free and clear or have low housing costs.

- You expect a modest lifestyle (annual spending in the mid-$30k to low-$60k range).

- You have a guaranteed income (Social Security, pension) that covers a healthy portion of essential needs.

- You have relatively good health and low expected long-term care needs.

$1M is less likely to be enough if:

- You still carry a mortgage or high rent.

- You plan expensive travel or maintain multiple properties.

- You face high local property taxes or expensive private healthcare needs.

- You have family patterns that suggest a high probability of long-term care.

A Quick Sensitivity Example: How Taxes and COLA Affect the Number

Start with $40,000 withdrawal (4% rule) on $1M. Subtract Connecticut + federal tax (amount depends on filing status and deductions), even a modest combined effective tax rate of 15% reduces $40,000 to $34,000 net.

Then account for a Connecticut cost-of-living premium of ~12% on your target spending bucket, that same lifestyle now needs roughly $44,800 in gross spending rather than $40,000.

That gap shows why $1M at 4% may not be enough once taxes and higher local costs are built into the plan. (Numbers above are illustrative; exact taxes depend on individual income sources and deductions.)

How Agemy Financial Strategies Approaches the Question

At Agemy Financial Strategies, we don’t answer the “is $1M enough?” question with a single number. We build personalized retirement blueprints that examine:

- Your current portfolio composition and tax status.

- Realistic spending needs and discretionary priorities.

- Housing and healthcare exposure, including the likelihood of long-term care.

- Social Security claiming strategies, pension options, and possible annuitization.

- A stress-tested withdrawal plan across market scenarios, including lower and higher volatility outcomes.

We model multiple scenarios (best case, base case, stress case) and present clear tradeoffs: retire now and reduce travel, delay retirement X years to improve odds, buy LTC insurance, do a partial annuitization, or adopt a dynamic spending plan.

Final Thoughts

$1,000,000 is a significant milestone and can absolutely fund a comfortable Connecticut retirement for many people, especially if combined with Social Security, paid-off housing, good health, and disciplined withdrawals. But Connecticut’s higher cost of living, property taxes, and the unpredictable cost of long-term care mean that $1M will not guarantee the same lifestyle everywhere in the state.

If you want certainty about your situation, the right next step is not to compare to a generic “enough” metric; it’s to run a plan using your actual numbers: your expected Social Security payout, your mortgage status, your desired annual spending, your health profile, and your tolerance for market risk.

Want to Know if $1M Is Enough for You?

At Agemy Financial Strategies, we’re highly experienced in retirement-income planning, “helping you make it down the mountain.” We’ll build a realistic, tax-aware plan, model how long your money will last under different scenarios, and create a practical path to the retirement lifestyle you want while protecting legacy goals.

Contact us today for a complimentary retirement readiness review and a custom scenario that answers the question specifically for your situation.

Visit agemy.com or call our office to schedule your consultation.

Investment advisory services are offered through Agemy Wealth Advisors, LLC, a Registered Investment Advisor and fiduciary to its clients. Agemy Financial Strategies, Inc. is a franchisee of Retirement Income Source®, LLC. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC are associated entities. Agemy Financial Strategies, Inc. and Agemy Wealth Advisors, LLC entities are not associated with Retirement Income Source®, LLC

The information contained in this e-mail is intended for the exclusive use of the addressee(s) and may contain confidential or privileged information. Any review, reliance or distribution by others or forwarding without the express permission of the sender is strictly prohibited. If you are not the intended recipient, please contact the sender and delete all copies. To the extent permitted by law, Agemy Financial Strategies, Inc and Agemy Wealth Advisors, LLC, and Retirement Income Source, LLC do not accept any liability arising from the use or retransmission of the information in this e-mail.