As we approach 2026, economic shifts, evolving tax policies, and financial market fluctuations make it more important than ever to reassess and refine your retirement goals.

At Agemy Financial Strategies, we understand that each client’s financial landscape is unique, and we help craft strategies that optimize wealth preservation, legacy planning, and lifestyle objectives.

In this guide, we will explore how HNWIs can approach setting meaningful retirement goals for 2026, incorporating actionable strategies to help safeguard wealth, maximize opportunities, and achieve a fulfilling retirement.

Understanding the Landscape: Why 2026 Is a Crucial Year

The financial environment heading into 2026 presents both challenges and opportunities. While historically low interest rates have affected traditional investment yields, the markets continue to offer avenues for growth. For HNWIs, the interplay between taxation, estate planning, and investment performance has become increasingly significant:

- Interest Rate Adjustments: The Federal Reserve has signaled potential rate changes in the coming years, influencing bond yields, mortgage rates, and broader investment strategies.

- Tax Policy Evolution: Anticipated adjustments to capital gains, estate taxes, and retirement account rules could significantly impact post-retirement income.

- Market Volatility: Global economic factors, including geopolitical tensions and inflation trends, underscore the importance of a diversified and resilient investment portfolio.

Setting retirement goals in 2026 requires not only a snapshot of your current finances but also an understanding of how these macroeconomic shifts may influence your wealth trajectory.

Defining Retirement Goals: More Than a Number

For many high-net-worth individuals, retirement planning is not merely about accumulating wealth; it’s about crafting a vision for the lifestyle you want to lead post-career. Defining clear retirement goals is essential for shaping your financial strategy. Consider these elements:

- Lifestyle Objectives: Do you envision traveling extensively, maintaining multiple residences, or pursuing philanthropic projects? Lifestyle expectations will dictate how much liquidity you need in retirement.

- Legacy Planning: High-net-worth individuals often prioritize passing wealth to heirs, funding charitable foundations, or establishing trusts. Clearly articulating your legacy goals can shape investment and tax strategies.

- Health and Longevity Planning: Ensuring your retirement funds account for potentially longer lifespans is critical.

- Flexibility vs. Security: Determine the balance between maintaining a secure income stream and preserving flexibility to seize new opportunities, such as private investments or emerging markets.

A precise understanding of your retirement vision can help enable more accurate financial modeling and goal-setting.

Conducting a Comprehensive Financial Audit

Before setting concrete retirement targets, it’s vital to assess your current financial position in detail. For HNWIs, this audit should go beyond simple account balances:

- Net Worth Analysis: Evaluate assets, including real estate, private equity holdings, business interests, art, and other tangible assets. Consider liquidity and market value.

- Income Streams: Identify active and passive income sources. Review dividend-yielding investments, rental properties, royalties, and business profits.

- Debt Management: Analyze leverage, including mortgages, lines of credit, and business loans, and plan for repayment schedules that align with retirement goals.

- Retirement Accounts and Tax-Deferred Investments: Consider contribution limits, potential Required Minimum Distributions (RMDs), and tax optimization strategies for 401(k)s, IRAs, and other accounts.

This audit allows you to determine the gap between your current resources and your retirement vision, helping to shape realistic and achievable goals for 2026.

Setting Financial Benchmarks for 2026

Once your audit is complete, it’s time to set specific financial benchmarks. HNWIs often have more complex portfolios, and benchmarks should reflect both wealth preservation and growth objectives:

- Target Retirement Income: Calculate the annual income you will need to sustain your lifestyle. This includes discretionary spending, healthcare, travel, and philanthropy. For HNWIs, you may need to factor in multiple residences, luxury expenditures, and tax obligations.

- Savings Goals: Determine how much additional savings or investment growth is required to bridge the gap between current assets and target retirement income.

- Investment Allocation Targets: Review your portfolio’s asset allocation to help ensure it aligns with your risk tolerance and retirement timeline. Consider a balance between liquid assets, growth equities, fixed income, and alternative investments.

- Estate and Tax Planning Milestones: Set goals for minimizing estate taxes, optimizing trust structures, and leveraging charitable giving strategies. This can help ensure wealth preservation across generations.

Benchmarking provides a roadmap for actionable steps and offers a framework for tracking progress throughout the year.

Leveraging Tax-Efficient Strategies

Taxes can significantly impact retirement wealth, particularly for HNWIs with complex portfolios. A forward-looking tax strategy is essential:

- Roth Conversions: Consider converting traditional IRA or 401(k) funds into Roth accounts in years when income is lower, potentially reducing long-term tax liabilities.

- Charitable Contributions: Utilize donor-advised funds or charitable remainder trusts to achieve philanthropic objectives while reducing taxable income.

- Capital Gains Optimization: Strategically manage the timing of asset sales to minimize capital gains taxes.

- Estate Planning Tools: Implement trusts, family limited partnerships, and gifting strategies to transfer wealth efficiently while minimizing tax exposure.

By integrating tax strategies into retirement goal-setting, HNWIs can preserve more wealth and help ensure their retirement lifestyle remains financially sustainable.

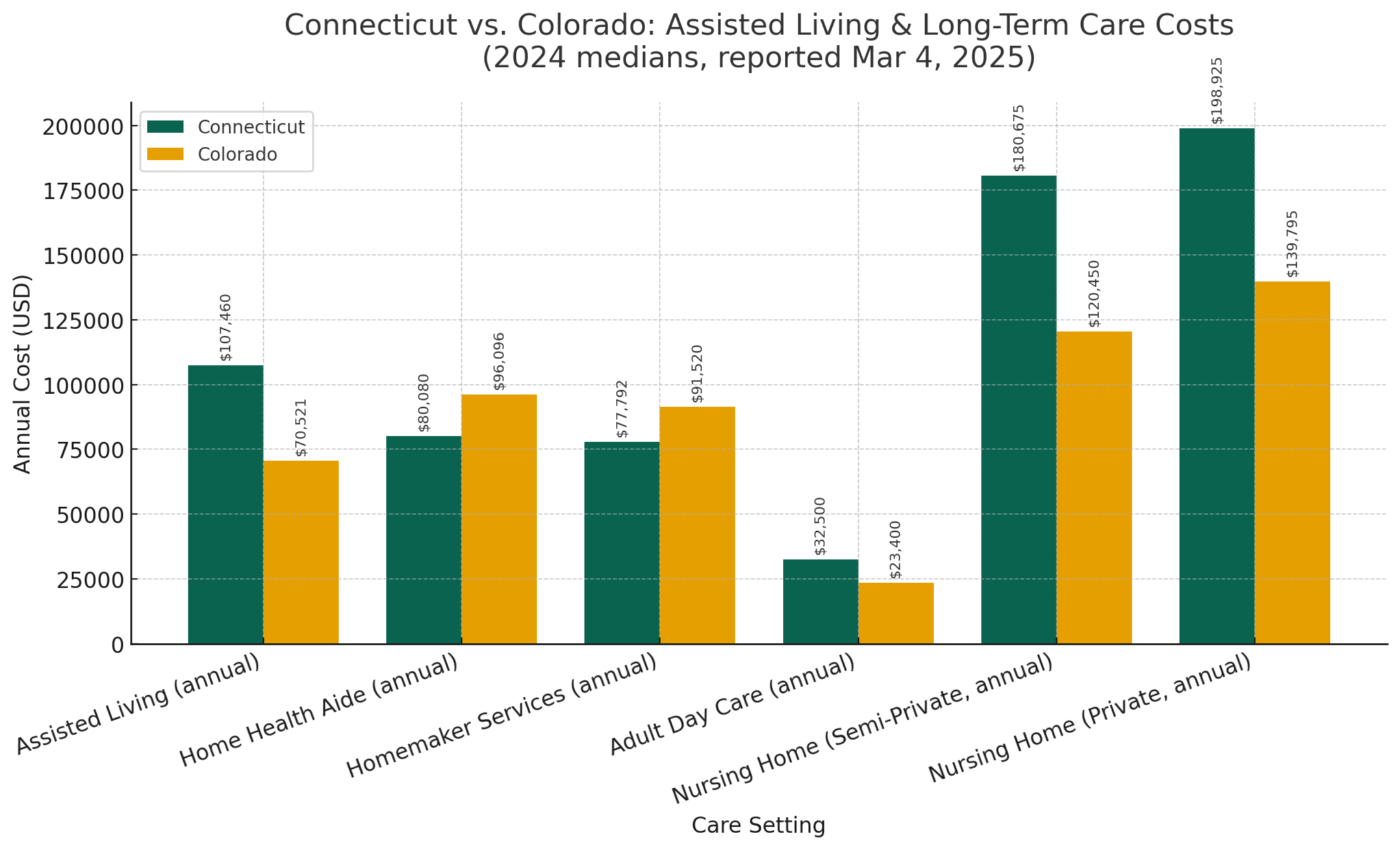

Accounting for Healthcare and Long-Term Care

Healthcare expenses are a critical, often underestimated component of retirement planning. HNWIs should proactively address these costs:

- Medicare and Private Insurance Planning: Evaluate coverage gaps and consider supplemental policies to address high-cost medical needs.

- Long-Term Care Planning: Explore options such as long-term care insurance, hybrid life insurance policies, and self-funding strategies.

- Wellness and Preventive Programs: Investing in preventive health measures can help reduce long-term medical expenses and improve quality of life in retirement.

Ensuring that healthcare and long-term care expenses are integrated into your 2026 retirement goals prevents unexpected financial strain and helps safeguard your wealth.

Diversification and Risk Management

A core principle for HNWIs is protecting and growing wealth through diversification and risk management. In 2026, this may include:

- Portfolio Diversification: Maintain exposure across equities, fixed income, real estate, private equity, and alternative assets. Diversification can help reduce vulnerability to market volatility.

- Geographic Allocation: Consider international investments to help hedge against regional economic fluctuations.

- Insurance and Asset Protection: Review life insurance, umbrella policies, and liability coverage to protect wealth.

- Scenario Planning: Stress-test your portfolio against potential economic shocks, market downturns, or unexpected personal events.

A disciplined approach to risk management helps ensure that your retirement goals are resilient under various market conditions.

Planning for Lifestyle and Legacy

For HNWIs, retirement planning extends beyond finances; it encompasses lifestyle aspirations and legacy goals:

- Lifestyle Planning: Define how you wish to spend your retirement years. Consider travel, hobbies, volunteerism, and ongoing professional involvement. Lifestyle planning influences cash flow requirements and investment strategies.

- Legacy Goals: Identify the financial legacy you wish to leave for heirs or philanthropic causes. Structured estate planning, trusts, and strategic gifting can help achieve these goals efficiently.

- Philanthropy and Impact Investing: Align investments with personal values, supporting causes that matter to you while potentially providing tax benefits.

Clear articulation of lifestyle and legacy objectives helps ensure your retirement is not only financially secure but also personally meaningful.

Monitoring, Adjusting, and Staying Informed

Retirement goal-setting is not a one-time exercise. It requires ongoing monitoring and adjustment:

- Regular Portfolio Reviews: Assess performance, rebalance assets, and make adjustments based on market conditions and personal circumstances.

- Policy and Tax Updates: Stay informed about changes to tax law, estate planning regulations, and retirement account rules that may impact your strategy.

- Professional Guidance: Collaborate with financial advisors, estate planners, tax professionals, and investment managers to help ensure your retirement plan remains aligned with your goals.

By maintaining flexibility and responsiveness, HNWIs can stay on track toward their 2026 and long-term retirement objectives.

Working With Agemy Financial Strategies

At Agemy Financial Strategies, we’re experienced in guiding high-net-worth individuals through the complex landscape of retirement planning. Our approach includes:

- Personalized Financial Planning: Tailored strategies that reflect your unique lifestyle, risk tolerance, and wealth profile.

- Advanced Tax and Estate Planning: Knowledgeable guidance to help optimize tax efficiency and ensure the smooth transfer of wealth.

- Comprehensive Investment Strategies: Diversified portfolios designed to preserve capital, maximize growth, and mitigate risk.

- Ongoing Support and Review: Continuous monitoring and adjustments to keep your retirement plan on course.

Partnering with Agemy Financial Strategies helps ensure that your 2026 retirement goals are not only realistic but also strategically designed for long-term success.

Final Thoughts

Setting retirement goals for 2026 is a multifaceted endeavor for high-net-worth individuals. It requires a blend of financial acumen, strategic foresight, and personalized planning. By defining clear objectives, conducting thorough audits, leveraging tax-efficient strategies, and planning for healthcare, lifestyle, and legacy, you can confidently navigate the path toward a fulfilling and secure retirement.

At Agemy Financial Strategies, we understand the complexities faced by HNWIs and provide the expertise needed to translate your retirement vision into actionable strategies. As 2026 approaches, now is the ideal time to refine your goals, safeguard your wealth, and help ensure your retirement years reflect the lifestyle and legacy you desire.

Take the first step today. Contact Agemy Financial Strategies to start crafting your 2026 retirement plan and secure a future that aligns with your vision, values, and aspirations.

Frequently Asked Questions (FAQs)

FAQ 1: What makes retirement planning different for high-net-worth individuals?

High-net-worth individuals have more complex financial portfolios, including multiple income streams, real estate, private equity, and business interests. Their retirement planning often involves advanced tax strategies, estate planning, philanthropy, and legacy considerations that go beyond traditional retirement savings plans.

FAQ 2: How should I set realistic retirement income goals for 2026?

Start by assessing your desired lifestyle, projected expenses, and potential sources of income. Consider discretionary spending, healthcare, travel, and legacy goals. Conducting a comprehensive financial audit with a trusted advisor can help determine the gap between your current assets and your target retirement income.

FAQ 3: How can tax planning impact my retirement strategy?

Effective tax planning can help preserve wealth and increase retirement income. Strategies may include Roth conversions, charitable giving, optimizing capital gains, and leveraging trusts or estate planning tools. Staying proactive with tax strategies helps ensure your assets work efficiently to support your retirement goals.

FAQ 4: Should I account for healthcare and long-term care in my retirement plan?

Yes. Healthcare and long-term care can significantly impact retirement expenses, especially for high-net-worth individuals who may require private coverage or specialized care. Planning for medical costs, insurance, and wellness programs can help ensure your retirement funds are sufficient for a comfortable lifestyle.

FAQ 5: How often should I review and adjust my retirement goals?

Retirement planning is dynamic. You should review your portfolio, tax strategy, and lifestyle goals at least annually or more frequently if there are major life changes or market shifts. Regular adjustments help ensure your plan remains aligned with your vision and adapts to evolving economic conditions.